The Bank of Canada targets 2 percent annual increases in the Consumer Price Index (CPI). However, some of the CPI’s components are volatile, making it difficult to determine inflation’s underlying trend – critical in the proper setting of monetary policy.

The Bank has created a series of core inflation measures as a result. One of them is CPI-common, which attempts to capture common price changes across the different categories of the CPI basket by omitting price movements that are specific to a particular component.

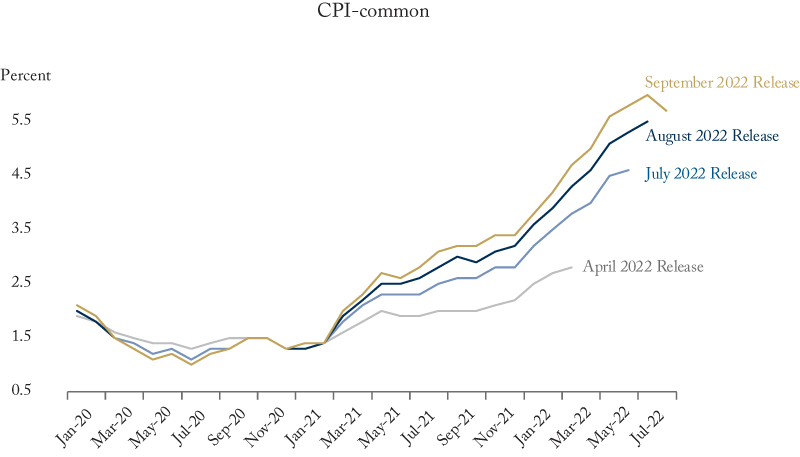

Trying to capture the underlying trend is crucial to getting monetary policy right. But, as the economics team at National Bank of Canada has pointed out, the model underlying CPI-common is not well suited to the job. The Bank’s re-estimates of CPI-common in recent months, as inflation has surged, have produced major upward revisions to its prior readings.

The Bank was relying on CPI-common as an indicator of trend inflation during this period, which means monetary policy likely stayed easy longer than it would have if the Bank had relied on something more dependable. The opposite problem is a possibility going forward: if CPI-common starts overestimating the underlying trend, the Bank could tighten monetary policy more than necessary.

This tightening cycle is going to be hard enough. No sense making it harder using an indicator that is wise only after the fact. The Bank should retire CPI-common.