Source: CFIB December 2019 Research Snapshot.

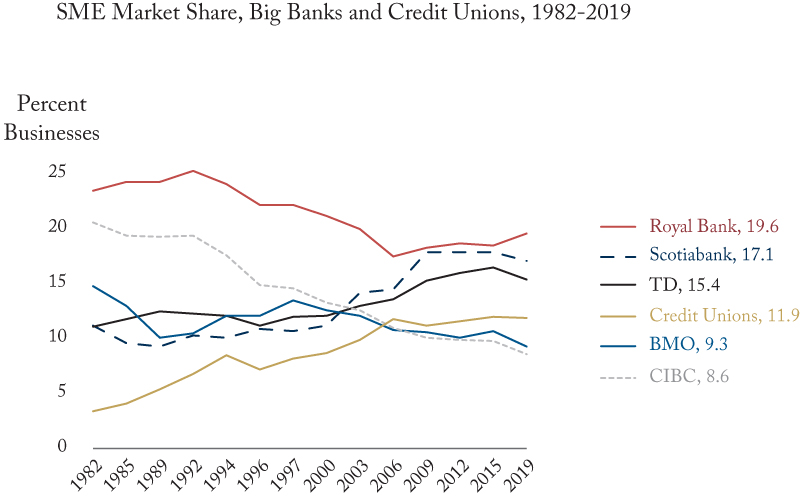

Credit unions in Canada play an important role in promoting financial services competitiveness. At the end of 2019, just before COVID-19, total credit union market share (assets/total financial institution assets) was 7.3 percent. While small relative to the big banks, credit unions punch above their weight in providing banking services to Canadian SMEs – who employ the vast majority of our private labour force. In 2019, despite a market share of just over 7 percent, nearly 12 percent of SMEs listed credit unions as their primary financial institution.

Credit unions began as retail-facing entities, meant to encourage thrift (savings) and offer small-dollar loans and home mortgages to under-served parts of the market. As they matured, and as the banks shifted to operating more retail-facing businesses of their own in the 1960s and 1970s, credit unions began to explore commercial real estate. After a rocky start in the late 1970s and 1980s, they found their footing in the 1990s, leveraging their governance model and its proximity to communities to expand their share of the SME segment – something that continued through the financial crisis.

Our recent paper offers a more detailed look at the sector and recommendations for its future.