by Thorsten V. Koeppl

- Data from the past 25 years show that natural disasters are happening more frequently in Canada, increasing overall losses from such events. Insurance markets face two main challenges when insuring against natural disasters: first, repeated large losses can strain underwriting capacity, driving up prices and reducing insurance availability; and second, extreme “peak perils” (such as major earthquakes) can threaten the solvency of the entire property and casualty (P&C) industry.

- Canada currently lacks a federal backstop for P&C insurers that could address these market failures. Such a backstop should be designed around three sound economic principles. First, it should leverage the government’s ability to smooth losses over time. Second, it should minimize costs to taxpayers by passing expected losses and costs to insurance customers. Third, it should rely on market mechanisms to allocate the costs of insurance to the source of the risk.

- A fully priced, mandated reinsurance scheme that transfers tail risk to the government satisfies these principles. The scheme uses two layers: a Disaster Risk Layer to smooth cyclical shocks and a Catastrophe Risk Layer to cover extreme events that threaten industry solvency. It also strengthens insurance coverage by making comprehensive coverage against disaster risk the default for consumers.

- Estimates suggest that this approach can expand broad coverage against natural disasters at a reasonable cost for the average policyholder.

Introduction

Canada faces the possibility of large seismic events, both in the Cascadia region off the West Coast and in the Charlevoix seismic zone in Western Quebec. At the same time, other natural hazards like wildfires, storms, and flooding are on the rise in Canada. Over the last 25 years, they have increased in frequency and, thus, total losses have mounted. Single extreme events – often considered tail risk – such as the Fort McMurray wildfire, the Calgary hailstorm, or the recent widespread flooding in Quebec, have caused significant losses for the insurance industry.

This development raises two distinct but related concerns. First, there is systemic risk.11 See the earlier contribution of Le Pan (2016). The occurrence of a peak peril event, such as a major earthquake, could wipe out the entire capital of the Canadian property and casualty (P&C) insurance sector. Second, there is the risk of severe disasters leading to insurance cycles. A string of tail events, i.e. rare, extreme events, with large losses can temporarily strain the capacity to underwrite insurance for the industry, leading to higher prices, tighter limits on coverage, and even possible withdrawal from certain perils. What complicates matters further is that insurance demand often does not internalize the full risk exposure. As a result, the insurance premiums people are willing to pay do not necessarily reflect the underlying risk.

Currently, Canada has no formal policy arrangements in place to address these concerns. Many other countries, however, provide a backstop or a government-provided reinsurance scheme to safeguard against these events. One approach is to cover only specific perils such as earthquakes (like Japan or New Zealand). Another approach is to cover perils more broadly (like France or Spain, or the recent discussion of having a public EU-wide catastrophe reinsurance layer). What these approaches have in common is that they are based on a private-public partnership where the government assumes only the tail risk, but the private sector continues to provide insurance.

This Commentary takes a look at the economics of insuring against natural disasters and argues that the federal government is uniquely positioned to improve on market outcomes by transferring both systemic and severe cyclical risk to its balance sheet. This is due to three advantages. First, governments can spread natural disaster risk over time through their softer budget constraint, that is, borrowing when necessary and building up reserves in other periods. The federal government can thus put up contingent capital upfront at a much lower level than private insurers, who have to worry about solvency. Second, when spreading risk over time, the government has an opportunity cost that tends to be lower than the return on equity (ROE) required by private insurers, which includes both risk and insolvency premiums. Third, the federal government can pool tail risk across Canada and across all hazards, achieving a large degree of diversification.

A well-designed risk transfer to the federal government must be based on sound economic principles. The core requirement is a fiscally responsible design that protects taxpayers. In particular, the costs of providing public funds to backstop risk must be recovered upfront and over time, and be passed through to insurance customers, preferably through a market-based mechanism.

Along these guidelines, this Commentary develops a concrete proposal with two pillars. The first strengthens demand for insurance as much as possible. This may involve mandatory coverage or default coverage for consumers with an opt-out option, at the cost of losing government assistance. The second pillar is an explicit reinsurance arrangement for P&C insurers. Under two layers – a lower Disaster Risk Layer (DRL) for sufficiently severe losses and an upper Catastrophe Risk Layer (CATL) for extreme losses – the government assumes industry-wide losses above certain thresholds in exchange for a premium that reflects the cost of backstopping the risk.

The reinsurance scheme builds up reserves over time by charging premiums to insurers that are in proportion to their underwriting. Insurers then pass these costs on to customers as they compete in the private market.22 Some of these insights are not new. Lewis and Murdock (1996) advocate for a federal catastrophe backstop along similar lines in the United States, while Cummins et al. (1999) develop a detailed methodology on how to implement it through an excess-of-loss contract that is sold via auctions. This Commentary follows some of these ideas, but deviates in key dimensions, for example, by promoting a backstop accumulating reserves and by insurers directly buying contracts from the backstop. Payouts are triggered by event-specific, industry-wide losses above the scheme’s thresholds. These thresholds need to be carefully calibrated so that risks the market can handle remain with private insurers and reinsurers.

By design, the scheme charges customers for transferring tail risk to the government. It avoids cross-subsidization between high- and low-risk areas. It also protects taxpayers by pricing premiums to cover expected losses over time, as well as the costs of providing contingent funds upfront. At the same time, it expands coverage to include all disaster risks, which is currently often restricted to specific hazards.

Finally, the Commentary estimates the premiums for the proposed transfer using illustrative thresholds of $2 billion and $10 billion per event for the two layers. These thresholds are not calibrated based on historic data on losses and fluctuations in insurance premiums but align with existing schemes in other countries. The results show significant savings for consumers in the DRL relative to purely private insurance. For the CATL, a simple calculation confirms that such risk is effectively uninsurable by private insurers due to the high cost of capital. A public reinsurance scheme, however, can provide this coverage at a reasonable price.

Natural Disaster Risk and the Canadian P&C Insurance Sector – Some Stylized Facts

An overview of the Canadian P&C market provides useful context for the analysis that follows. Regulation is split between the federal and provincial governments: the former oversees solvency, and the latter governs market conduct and rate setting by insurers. The industry has established a not-for-profit backstop – the Property & Casualty Insurance Compensation Corporation (PACICC) – which partially covers losses from the insolvency of individual insurers.33 There have been no failures of P&C insurers in Canada since 2003, with PACICC insuring the last two failures prior to 2003 (see Kelly et al. 2024). Its compensation fund is around $60 million, with the possibility to access up to $1.27 billion annually from its members, representing about 95 percent of the Canadian P&C market. The federal government does not provide a backstop for insurers. Instead, it provides disaster relief to provinces for large, geographically concentrated events. Importantly, this assistance does not include a replacement guarantee for insured losses.

This approach differs from many other advanced economies. Countries like Japan, Taiwan, and New Zealand mandate earthquake insurance with government-backed reinsurance covering both tail risk and peak perils. France, Spain, and Switzerland mandate coverage for all natural disasters with direct government involvement. Still other countries rely on industry-sponsored reinsurance pools for specific hazards – like Flood Re in the UK – with government guarantees only if those pools are exhausted.44 A detailed comparison is beyond the scope of this Commentary. For a recent detailed overview of such schemes, see Kelly et al. (2025) and IBC (2015a).

The Canadian P&C market is somewhat concentrated. The top five insurers account for about 45 percent of the market, with the next five holding an additional 20 percent. This is partially the result of some consolidation within the industry over the last two decades, including exits and acquisitions. Most large insurers operate nationwide and maintain significant market shares across provinces and territories, while some regional players remain active, particularly in the Prairies and Quebec. Expanded distribution channels through brokers, agents, and direct online offerings have also increased competition.55 Campbell (2024) presents a detailed industry overview. He also calculates a Herfindahl-Hirschmann index (HHI) that indicates a highly competitive environment.

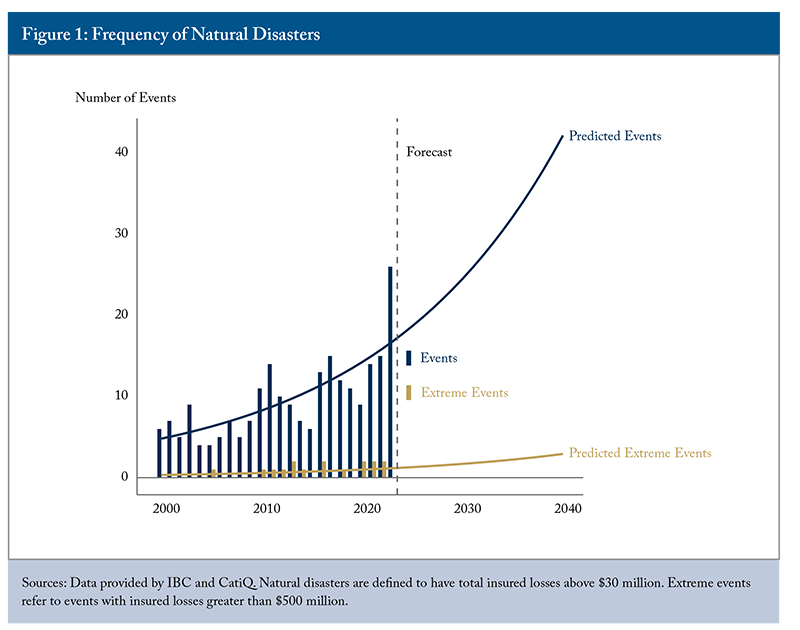

Catastrophe losses due to natural disasters have received a lot of attention recently. Figure 1 plots the total number of natural disaster events, as well as the number of extreme events with losses exceeding $500 million. A straightforward estimation (see online Appendix I) reveals an exponential increase in the frequency of such events, but the evidence suggests that large losses above the threshold of $500 million have become less frequent, relative to other natural disasters that have lower losses.

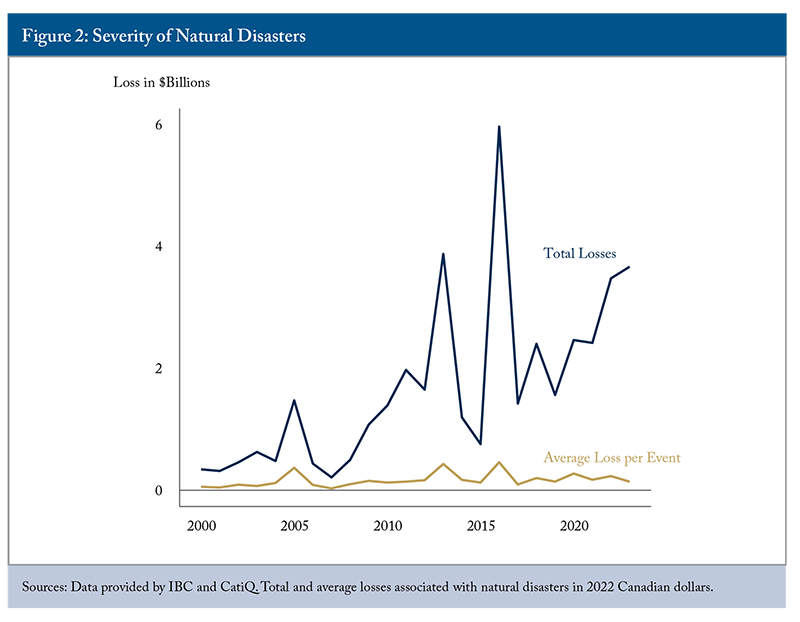

Figure 2 plots total insured annual losses from severe events in 2022 Canadian dollars.66 To arrive at a better estimate of future loss estimates in current dollars, one would have to add an estimate of replacement costs, which have outpaced general inflation over the time period (see McGillivray 2024). There is no clear trend in the average loss per event since 2000. Hence, total losses increased primarily because events occurred more frequently. The so-called uninsured loss or protection gap is currently estimated at roughly 37 percent77 Swiss Re offers an interactive tool that estimates this gap. See https://www.swissre.com/risk-knowledge/mitigating-climate-risk/natcat-protection-gap-infographic.html#/. According to this source, Canada has a lower gap than countries like the United States or Germany, but a higher one than the UK or Switzerland. for the Canadian market, meaning about two-thirds of disaster risk is currently covered by insurance.

More than 60 earthquakes of magnitude (M) larger than 6.5 on the Richter scale – capable of causing major damage – have been recorded in Canada since 1660.88 See Cassidy et al. (2010). There are no data available to estimate the frequency or severity of the associated losses. Hence, most analyses of earthquakes are based on scenarios. Table 1 presents two commonly used stylized scenarios: one off the coast in British Columbia and another in the Charlevoix region of Quebec, northeast of Ottawa. The estimated damages include only private property and exclude losses to infrastructure and further economic losses. These scenarios are so severe that they would lead to a collapse of the Canadian P&C sector.99 See Kelly et al. (2024). The threshold considered for a systemic event where the entire industry collapses is pinned at roughly $35 billion. One would expect, however, that the entire industry would come under severe stress already at a much lower level.

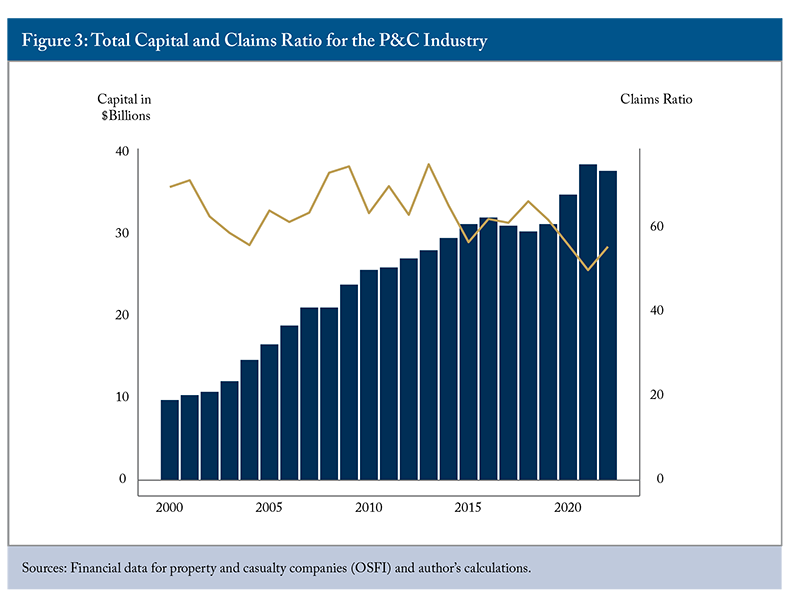

The industry-wide claims ratio for P&C insurers – the ratio of claims to premiums written – has been fairly steady over time (see Figure 3). Regionally, however, claims ratios have spiked following natural disasters that disproportionately affected particular regions, which emphasizes the benefits of geographical diversification for Canadian insurers.1010 For example, the claim ratio hit 400 percent in the wake of Hurricane Fiona in PEI for 2022. Figure 3 also shows that the total capital in Canada’s P&C sector has increased by about 400 percent since 2000 and remains around $40 billion.1111 These figures also include capital of mortgage insurers. The adjustment was necessary to generate a consistent time series, given changes in OSFI’s reporting. Over this time horizon, the industry consistently met its main solvency metric – the Marginal Capital Test (MCT) ratio – maintaining capital at about 2.5 times or more the minimum capital required by the Office of the Superintendent of Financial Institutions (OSFI).

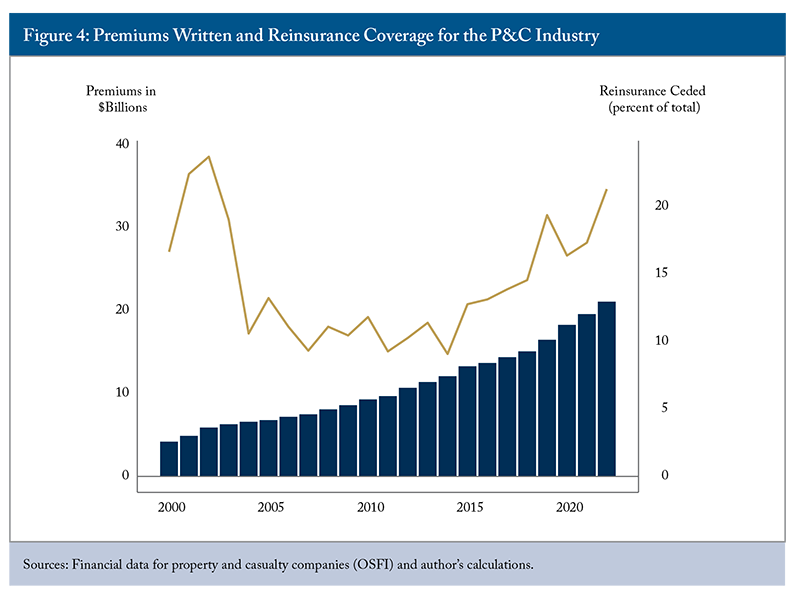

The Canadian P&C sector strengthens its capital base through reinsurance. The global reinsurance market operates with capital of about US$400 billion, excluding Berkshire Hathaway’s reinsurance operations that tend to focus on specialized risks.1212 For more information on the market, see Gallagher Re (2025). Demand for reinsurance has increased over the last few years to about 20 percent of premiums, bringing the total closer to the early 2000s when reinsurance demand increased in the wake of insurer insolvencies (see Figure 4).

Reinsurance capital fluctuates with losses from natural disasters. For example, industry-wide capital declined by 5 percent in 2018 and 17 percent in 2022. These declines were followed by higher reinsurance prices, making risk transfers more expensive for P&C insurers but also supported capital rebuilding through higher profitability.1313 See for example CBO (2024) and AON (2025).

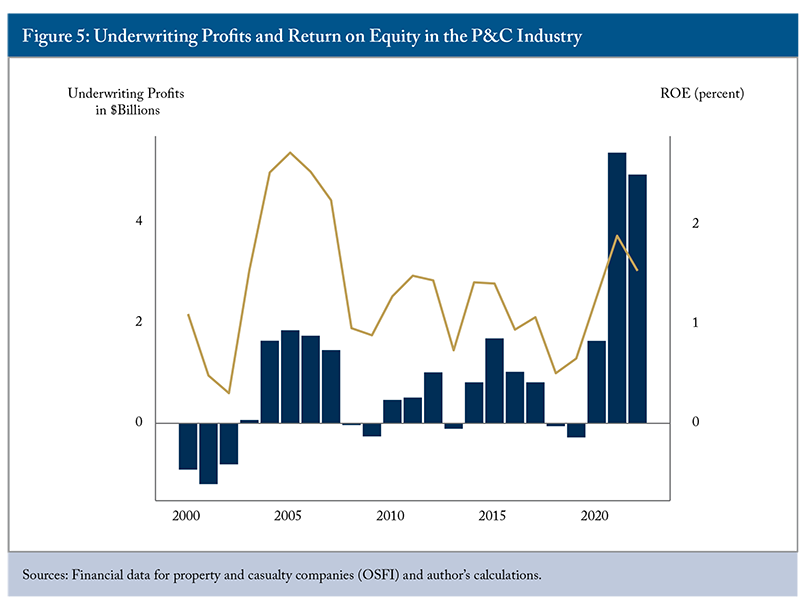

Despite this risk transfer, the ROE in the sector has fluctuated widely across time (see Figure 5), primarily due to large swings in underwriting profits for Canadian insurers. This variability reflects so-called “insurance cycles,” discussed in the next section. Soft markets with lower rates, more lenient underwriting, and higher capacity result in low profits. These are followed by hard markets with higher rates, stringent underwriting, and restricted capacity, resulting in higher profit margins.

The analysis in this section can be summarized in five stylized facts:

- The Canadian P&C market is fairly competitive, with leading companies operating nationwide.

- Insured losses from natural disasters have increased considerably and are likely to keep increasing.

- Reinsurance has become more important, but reinsurance capital and costs fluctuate considerably over time.

- Insurance cycles are evident, with underwriting profits and ROE varying over time.

- There is a meaningful risk of a major natural disaster in Canada – likely seismic in nature – which could lead to a significant fall in capital of P&C insurers, as well as insolvencies of some insurers or the entire industry.

Are There Market Failures in Insuring Natural Disaster Risk?

Insurance pools risk across a large population, exposing insurers to average losses rather than individual outcomes. This makes losses more predictable and reduces the need for costly capital to cover insolvency risk. In a well-diversified pool, premiums can be “fair” in a competitive environment. Customers pay premiums that reflect their expected loss, plus some adjustment for expenses and the cost of capital that insurers incur. Importantly, “fairness” here has nothing to do with “affordability.” Insurers just charge their expected cost to risk-averse consumers for the transfer of risk.

There are reasons, however, why competitive markets for insuring against natural hazards do not work well.1414 The most prominent market failures in insurance are moral hazard and adverse selection, where people’s actions or their innate, but unobservable characteristics, adversely affect losses. When looking at natural hazards in P&C markets, however, such failures tend to play a minor role. Differences in risk among the insured are often common knowledge and, hence, can be priced into premiums. Similarly, such risks either tend to be exogenous to people’s actions or incentives can be given to mitigate losses. The key issues lie on both the demand and supply sides, resulting in relatively low coverage.

The Demand Side

Several, mostly behavioural, factors can suppress demand, even at fair prices. First, households and businesses are often not fully aware of the risk exposure they face. The Canadian Council of Insurance Regulators (CCIR) discusses several gaps in consumer awareness.1515 See CCIR (2023). First, people tend to underestimate the frequency and severity of rare events and often do not understand their coverage or available options for natural hazards.

Survey evidence confirms these gaps, with regional differences. For example, when it comes to earthquakes, awareness is relatively high in British Columbia but very low in Quebec, where many people mistakenly believe that they have insurance coverage in their policies.1616 See IBC (2015). For other hazards, such as flooding, insurance take-up has increased, mainly for low- and medium-risk areas.1717 See for example CatIQ (2022). The increase is due to both more demand and better risk measurement through improved flood mapping.

Second, households and businesses may wrongly believe that the federal and provincial governments stand ready to provide full financial assistance to cover losses in case of a major natural disaster. Under a new framework announced in 2025, the federal government provides assistance in the form of cost-sharing agreements for emergency response, rebuilding critical infrastructure, and losses suffered by households and small businesses where insurance is not available.1818 On the provincial level, disaster relief varies both in coverage and deductibles with most of the relief being provided by the federal government in the event of large natural disasters. In practice, governments may provide additional support after large events, creating incentives for consumers to “free ride,” especially when perceived risks are very low.

Finally, consumers may anticipate insurer insolvency following a natural disaster. Customers thus face both the underlying risk and the risk of insurer default. This can lead risk-averse consumers to reduce coverage or opt out entirely, since they may not receive a full insurance payout in bad times.1919 For a detailed review of the demand for insurance, including this argument, see Schlesinger (2013).

The Supply Side

On the supply side, there are two reasons why the market for insuring against large natural disasters does not work well. First, peak perils such as a major earthquake can cause exceedingly large losses while occurring infrequently. These events can threaten the solvency of the entire P&C industry, requiring insurers to hold substantial capital upfront. Such risk is therefore considered to be “uninsurable” due to the high cost of capital.2020 For a more technical, but still accessible analysis of “insurability,” see Cummins (2006). Where coverage is available, it is typically limited in quality, with high deductibles, exclusions for certain hazards, and restrictions on payouts to a single occurrence.

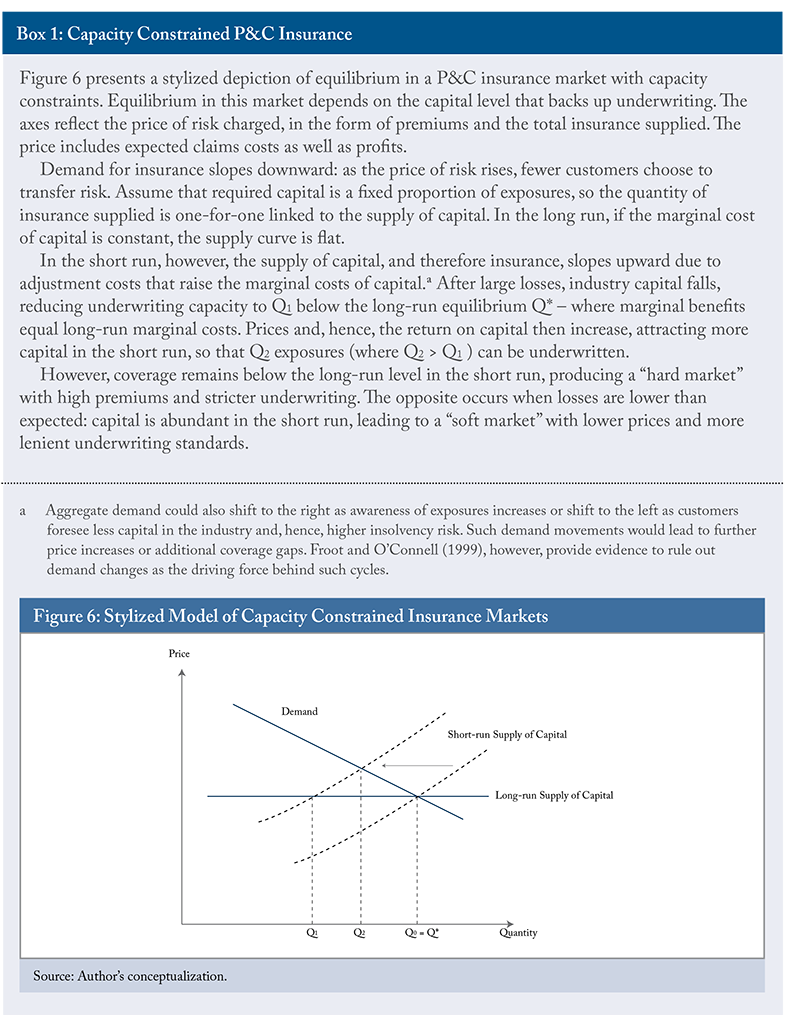

A second issue is that P&C insurance markets tend to react adversely to shocks in the form of extreme losses caused by a string of natural disasters. The literature on insurance shows that capital is costly to rebuild and slow to adjust, giving rise to the phenomenon of significant insurance cycles.2121 Harrington et al. (2013) provide a detailed review of the literature on insurance cycles with a focus on adjustment costs of capital. Other prominent explanations for such cycles are variations in investment returns and regulatory restrictions for premium adjustments that lead to reduced coverage. Froot and Stein (1998) provide a solid theoretical foundation for shocks to insurers’ capital driving pricing in the presence of costly external capital, investment uncertainty, and hedging possibilities. After a sequence of larger-than-expected losses, insurers’ capital declines, increasing insolvency risk. In response, insurers raise premiums and tighten coverage. The additional revenue can be used to rebuild capital internally so that, over time, capital levels return to normal levels with premiums falling and coverage reaching old levels.2222 When insurance demand is very sensitive to higher premiums or when premiums are capped by regulation, insurers may not be able to raise premiums sufficiently to rebuild capital. In such a scenario, they are even forced to leave the market. Even when solvency is not at risk, these cycles reduce the availability of insurance in the short run, as premiums, deductibles, and underwriting standards all increase.

As capital is costly, P&C insurers often try to transfer their tail risk to reinsurers or capital markets. Reinsurers operate globally and can achieve at least some geographic diversification, which lowers their cost of capital. Similarly, capital markets have an incentive to offer insurance-linked securities (ILS) such as catastrophe bonds, since catastrophe losses tend to be uncorrelated with financial market returns. In principle, these channels could ease supply-side constraints in insurance markets.

The evidence, however, does not support this view. For example, Froot (2001) points out that the market power of reinsurers and their own capacity constraints are responsible for premiums that far exceed expected losses from catastrophe events. Hence, reinsurance is still very costly, especially for peak perils. Reinsurance markets also exhibit cycles tied to the availability of global reinsurance capital. As pointed out, this is reflected in the relatively high premiums that reinsurers have charged over the last few years in the wake of an increase in catastrophe losses.

Overall, the amount of capital available through reinsurance is limited and expensive for Canadian P&C insurers when covering large natural disaster losses. This points to persistent capacity constraints in the industry, not only for peak perils such as earthquakes, but also as a consequence for losses arising from a series of large natural disasters.

Designing a Backstop as an Additional Publicly Provided Reinsurance Layer

Why Introduce a Government Backstop in the First Place?

Private capital works well for covering lower levels of natural disaster risk. As noted, global reinsurers and capital markets benefit from geographic diversification and can spread risk over time. But if “the ability of a reinsurer to diversify catastrophic risk is limited by the reinsurer’s access to capital and the costs associated with the risk of insolvency ... [then] the actuarially fair premium ... is meaningless if the ... disaster ... bankrupts the re-insurer” (Cummins et al. 1999). Above a certain threshold, the government therefore has a clear advantage over private capital in backing up insurance.

The government is less constrained by solvency and can spread aggregate risk better over time. Rather than putting up capital upfront, it can pledge contingent capital and recover the losses from underwriting disaster risk over time. The costs of doing so are related to the costs associated with government borrowing, which tend to be below the typical required ROE in the insurance industry that includes premiums for risk and insolvency. A public backstop can both make broadly available high-quality insurance against peak perils and improve market outcomes in the face of capacity constraints.

Any government backstop, however, needs to be based on sound economic principles. First, it should leverage the government’s ability to spread risk over time. Second, it needs to minimize the costs for taxpayers by passing on its expected losses and costs to insurance customers. Third, it should rely as much as possible on market-based mechanisms that address the market failures at their root.2323 For this last point, see also Kunreuther and Kerjan (2013).

These principles are best embodied by an explicit transfer of tail risk from P&C insurers to a government backstop in the form of a reinsurance arrangement that is properly priced. Such an arrangement would charge both premiums and the costs of public funds related to possible government borrowing from the start, ensuring that the contingent liability of the government is managed prudently.

The design requires two broad-stroke measures to deal with the market failures identified earlier. The first is to strengthen the demand for catastrophe insurance. The second is the transfer of tail risk at a “fair” premium – protecting taxpayers – which relies on a competitive P&C insurance market to pass costs through to those bearing the risk, namely households and businesses.2424 As a byproduct, a reinsurance scheme would also shift costs away from disaster relief where the government may be inclined to bail out consumers after large disasters. Reinsurance levies the costs ex-ante on insurance customers and not, like disaster relief, ex-post on taxpayers. This is important as costs for disaster relief may increase despite a revised federal program (see PBO 2025).

Before going into further detail, it is important to stress that the reasoning here is based entirely on correcting market failures, not on making insurance more affordable. Backstop solutions for disaster risk can also take the form of implicit taxpayer-financed subsidies for households and businesses living in high-risk areas. For example, a government guarantee in the event of large catastrophe losses may act as a covert subsidy for P&C insurers: insurers collect premiums in good times, while losses are partly absorbed by the government (and ultimately taxpayers) in bad times.

Strengthening the Demand Side

On the demand side, the guiding principle for a backstop is to increase the risk pool as much as possible. This would spread risk across more people and regions, bringing the pool closer to reflecting the average risk. In a similar vein, the backstop should be comprehensive, providing coverage against tail risk for all natural hazards.

Insurance still must be priced fairly, reflecting expected losses. This implies that people exposed to extreme events, such as earthquakes, or living in higher-risk areas, such as flood or earthquake zones, will pay more for insurance. Expanding insurance against natural disasters will therefore place most costs on those facing these risks. It is essential, then, to ensure these individuals purchase insurance at prices that reflect their exposure.

The proposed solution is to require insurers to offer comprehensive insurance against all natural hazards by default. This would raise consumer awareness and make insurance pricing more transparent, reflecting the likelihood of any hazard materializing. Customers could still have the option to opt out by declining coverage.

To limit free riding by high-risk individuals who expect government support after a disaster, insurance contracts should specify that those who opt out receive only immediate disaster relief, with no further compensation from governments or insurers. This is in line with the new design of federal disaster relief but hinges on the government credibly committing to such a policy.

If this approach does not sufficiently expand the pool, a stronger measure may be needed that would make property insurance mandatory for private and commercial property owners, possibly with a maximum deductible. This would be an extreme option. But many homeowners and businesses are already required to have coverage, for example as a condition of a mortgage.2525 For private properties, a rough calculation based on information from OSFI and Statistics Canada indicates that between 75-80 percent of all properties – roughly 12 million out of about 16 million properties – are insured (author’s calculation).

Strengthening the Supply Side Through a Transfer of Tail Risk

On the supply side, transferring tail risk to the government can address both the lack of high-quality insurance against peak perils and also the possible fluctuations in underwriting capacity. But this transfer must follow the principles outlined above. To minimize costs for taxpayers, it should take the form of a fully priced reinsurance arrangement that leverages the government’s ability to spread aggregate risk over time. Other solutions, like ex post bailouts, repayable loans, or recapitalizations, do not follow prudent rules for fiscal management that spread the costs of public funds across time. In a nutshell, the best form of backstop formalizes the federal government’s role as the “insurer-of-last-resort” through an explicit reinsurance scheme.

The costs of providing such reinsurance need to be passed on to the industry. In a largely competitive industry, P&C insurers would then pass on the premiums to consumers, akin to other reinsurance arrangements already in place. Private reinsurers can still compete for lower layers of exposure. This would preserve market competition while addressing market failures and ensuring costs flow through to final customers.

A comparison with mortgage insurance is instructive. The federal government provides a backstop to the industry, which consists of private insurers and a Crown corporation, the Canadian Mortgage and Housing Corporation (CMHC). The idea is that the federal government recapitalizes the sector in the event of a major housing crisis when insurer capital is insufficient to cover all losses.

But here the analogy ends. The backstop for mortgage insurance is currently not priced. Once losses materialize, taxpayers face an effective increase in their tax burden when funds used in the bailout are not fully recovered. Similarly, the costs of public funds associated with the contingent liability are not passed on to the industry upfront either. As with natural disaster risk, a fully priced reinsurance scheme against tail risk in the housing sector is the preferred solution.2626 For more details, see Koeppl and MacGee (2015). CMHC also provides insurance directly to Canadian households, which questions the idea of a level playing field in the market.

Main Design Features

Reinsurance Scheme

The reinsurance scheme should use two layers, reflecting the two different market imperfections on the supply side outlined earlier. The first layer – the Disaster Risk Layer (DRL) – addresses the tendency for insurance markets to tighten after a series of large, but not extreme, losses due to natural disasters. Excluding earthquakes, natural disasters have a basic element of diversification across time. This allows coverage through a quasi-revolving tranche in which premiums break even with losses over a medium-term horizon. In essence, this layer transfers cyclical disaster risk to the federal government.

Extreme tail risk, like a major earthquake, requires a second layer – the CATL. Because peak perils occur infrequently, this layer allows reserves to build over a long horizon. It transfers the risk of a systemic crisis in the insurance sector to the federal government and substitutes private capital provided upfront by contingent public capital.

Thresholds for these layers need to be carefully calibrated to reflect when cyclical or systemic disruptions are likely, without crowding out private reinsurance in lower layers. For illustration, consider excess-of-loss (XOL) contracts that cover all events within a given period – for example, one year – within a specified loss range.2727 For details on such contracts, see Appendix. The DLR could cover losses between $2 billion and $10 billion per event, while the CATL would apply above $10 billion up to a ceiling. The upper threshold would remain below the estimated $35 billion level associated with systemic collapse of the Canadian P&C sector (see Kelly et al. 2024), recognizing that severe stress would likely occur well before that point.

Under this design, the CATL would not have been triggered by any event since 2000, whereas the DRL2828 This would be similar, at $2 billon, to other government-operated reinsurance schemes like Taiwan or Japan. would have paid out only once. Lowering the threshold to $1 billion would have resulted in four payouts, whereas lowering it to $500 million would have included 16 events.

As a result, the government backstop would separate risk into three layers. The lowest one can be diversified and will be covered by traditional reinsurance, putting private capital at risk. The middle layer covers cyclical risk that can be diversified over time, while the highest layer reflects systemic risk that cannot be diversified. The last two layers would be backed by public capital through a reinsurance scheme.

An important element of the reinsurance scheme is an event-specific, industry-wide trigger: each qualifying event within a year can trigger payouts. The backstop does not depend on the capital position or losses of individual insurers. Instead, it covers industry-wide losses from extreme events, complementing the role of PACICC, which is focused on the insolvency of individual insurers.2929 Le Pan (2016) argues for a larger role of PACICC, covering also systemic risk. This design also limits moral hazard or adverse selection by reducing incentives for insurers to concentrate risk.

Pricing

The DRL and CATL can be priced from an actuarial perspective (see Appendix). The pricing will reflect three components: the expected losses from writing the reinsurance, underwriting costs, and the costs for the government to put up capital for which further detail is provided next.

First, the scheme is designed to break even over time. Because losses fluctuate, the scheme must hold reserves to protect taxpayers. Initially, the government could merely put up contingent capital through a priced credit line. Over time, the reinsurance scheme will then acquire reserves in good times, which it can invest, while in bad times it taps into the credit line and borrows. Such a setup avoids precisely the problem of cyclical fluctuations of insurance capital while spreading the cost of public funds over time.

Second, the scheme must recover the net cost of contingent capital through premiums. If the scheme builds up reserves, it can pay out an interest rate from its investments that lowers current premiums. If the scheme has accumulated contingent debt, it needs to repay the debt plus accumulated interest through higher current and future premiums. With the fluctuations in reserves cancelling out over time, the government thus insulates taxpayers from assuming the costs of providing reinsurance to the market. The required rate of return can be set to the long-term marginal costs of public funds associated with government borrowing, which are estimated to be currently around 7-8 percent (see online Appendix II). This is well below the 10-14 percent ROE typically targeted by private reinsurers over the insurance cycle.

P&C insurers would be required to purchase tail-risk coverage periodically, say once a year, to cover their exposures for the upcoming year. With the strengthening of the demand side, insurers would then pass these costs on to consumers. In a competitive insurance market, premiums will then reflect each policyholder’s underlying exposure to natural disaster risk.

Practical Considerations when Implementing the Reinsurance Scheme

The reinsurance scheme would charge separate premiums for the two layers to insurers, assessed on individual insurers’ underwriting and reflecting geographic and other factors that affect the frequency and severity of losses. For practical reasons, pricing would occur at fixed intervals using insurers’ underwriting at that moment in time. As a rule of thumb, reinsurance can be sold on a yearly basis using insurance in force at a particular date for pricing.3030 An additional possibility is that insurers have the option to replace coverage under the reinsurance scheme with private reinsurance. This aspect, however, may introduce moral hazard if the solvency risk of the private reinsurer is high.

As with typical insurance, payouts from the scheme would be pro-rated according to the actual losses suffered in an event. Insurers with greater losses would receive a larger proportion of the payouts. For example, an insurer bearing 40 percent of total losses would receive 40 percent of the payouts, irrespective of the premiums paid. Insurers would thus avoid so-called basis risk where the protection is not perfectly aligned with an insurer’s underwriting.

The reinsurance scheme would also need to assess insurers’ exposure to natural disaster hazards. This requires a formal, geographic risk assessment based on flood mapping, wildfire risk, seismic regions, and so forth.3130 L’empanellement consiste à rattacher chaque patient à un médecin de famille ou à une équipe de soins, créant ainsi un groupe de patients défini afin d’assurer la responsabilisation, la continuité des soins et une gestion proactive. Such comprehensive risk mapping does not exist currently and would need to be developed, preferably in a joint effort between the industry and the federal government.

A final consideration is how the reinsurance scheme decides when the trigger for an event has been met. Claims following a disaster must be assessed and verified within a relatively short timeframe (e.g., 12 months) to provide planning certainty. Trigger thresholds should also be updated periodically to reflect inflation, growth in exposures, and potential changes in loss severity and replacement costs.

Putting the Reinsurance Scheme into Action

To get an idea of the costs for consumers, it is useful to carry out a back-of-the-envelope estimate of the premiums that need to be charged under the scheme. Several simplifying assumptions apply. First, all results are expressed in 2022 Canadian dollars. Second, the analysis is based on insured losses only, not total loss data.3232 Using the loss gap mentioned earlier to scale the data may introduce bias as it is based on more recent data, and historical data are not available. Also, if take-up is not 100 percent, one needs to make an assumption as to what part of the loss will be covered by the backstop. Third, it assumes no time trend in the severity of tail losses, consistent with the available data. Fourth, long-term borrowing costs for the federal government are set at 4 percent, so that the cost of capital for the government is around 8 percent. Fifth, the analysis abstracts from the expense ratio and any investment returns on accumulated reserves. These factors work in opposite directions and are hard to predict, so they are assumed to offset each other. Overall, these assumptions allow the scheme to be illustrated and provide a rough estimate of the costs.

Premiums and Reserves for the DRL

For the DRL, data related to natural disasters in Canada from 2000 to 2023 are used to estimate the frequency and severity of natural disasters (see Appendix).3333 Data were taken from IBC (2023) or were directly provided by CatIQ. For expositional purposes only, the XOL contract thresholds are set at $2 billion and $10 billion.

The pure premium equals the expected number of events per year multiplied by the expected payout from the scheme per event. In the estimation, the expected number of events increases over time as the frequency of natural disasters shows a positive time trend. By contrast, the expected payout per event is held constant, as the data show no trend in severity (see Figure 1).

The premium is then adjusted for the cost of capital. The main advantage of the reinsurance scheme is that it can tap into contingent capital and therefore smooth out losses across time. Consequently, capital at risk can be set equal to the total expected payout under the XOL contract, which, conveniently, is equal to the pure premium charged by the reinsurance scheme.

Since surpluses and deficits accumulate over time, capital at risk must be adjusted for accumulated reserves. These reserves will be negative if the backstop has accumulated debt over time. This leads to the following pricing formula:

Premium(t) = Pure Premium(t) + ROE × [Capital at Risk(t) − Reserves(t)]

All variables depend on time t. The return on equity (ROE) is set to 0.08 (or 8 percent), reflecting a conservative estimate of the costs of public funds.

The backstop charges for the opportunity cost initially, and then whenever its reserves are below the capital at risk. At the same time, the premiums are lowered when reserves are sufficient to cover the expected yearly payouts and all accumulated debt. As a result, pricing depends on the history of losses and equals the pure premium plus some adjustment cost for contingent capital, which may be positive or negative depending on the scheme’s net debt position.

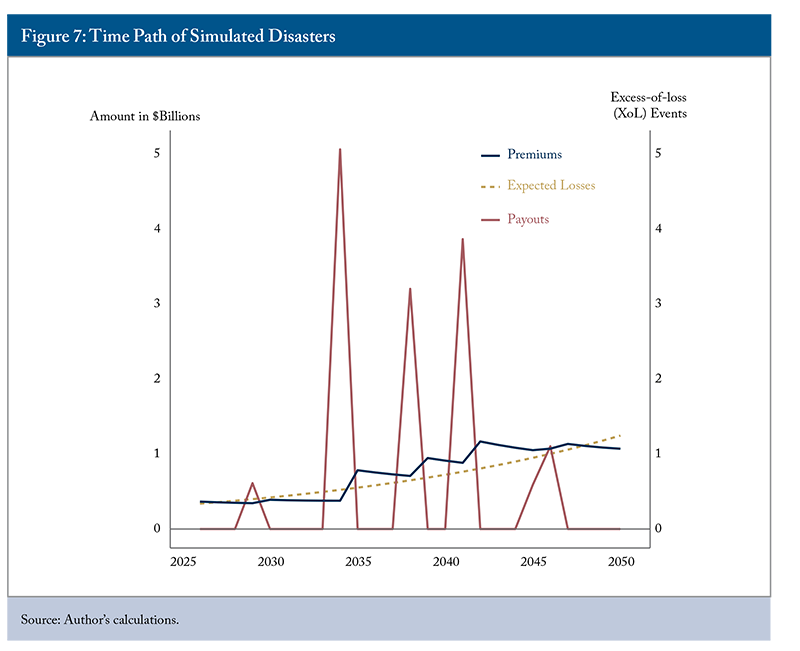

Figure 7 shows a simulated path for the number of events that trigger the XOL contract and the associated total losses for the scheme. Payouts are infrequent but can be large since the DLR covers a relatively high layer of risks.3434 The value at risk (VaR) for the layer is roughly at the 95 percentile. The dashed gold line refers to the expected losses (the pure premium), while the blue line shows actual annual premiums charged by the reinsurance scheme. The growth in premiums reflects the trend in the frequency of large natural disasters. Any upward (or downward) deviation of premiums from expected losses reflects the cost of capital or the benefit of accumulated reserves.

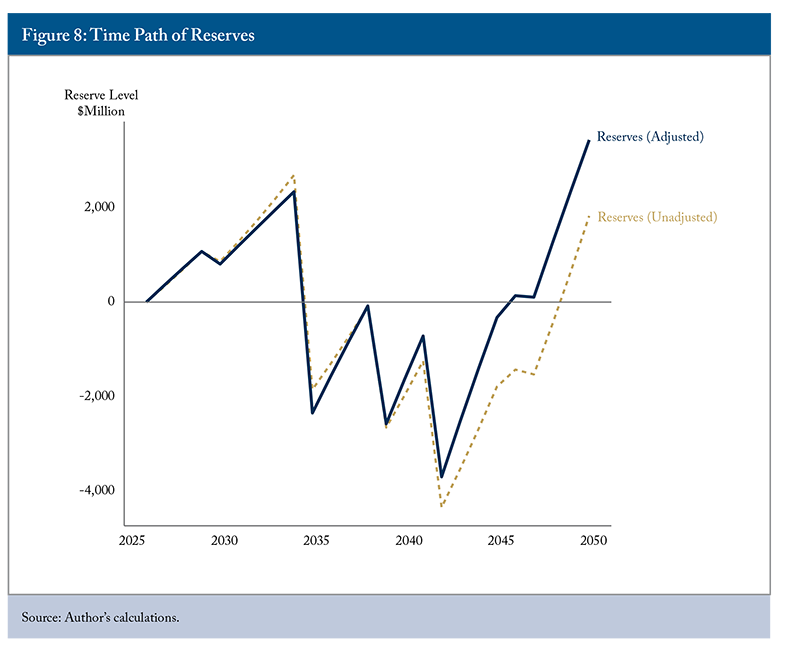

Figure 8 shows the development of reserves for this sample path. Initially, the backstop has no reserves as it relies on contingent capital provided by the government. In the early years, losses are relatively small, so the scheme runs a surplus and builds reserves, aside from a small premium discount reflecting the fact that reserves exceed capital at risk. After some time, the reinsurance scheme needs to borrow to cover losses that exceed its reserves. Premiums then reflect the cost of public borrowing. In the simulation, however, the scheme roughly breaks even over the 25 years, ending with a surplus over the last few years. More generally, averaging across many such simulations would show that the expected cost of the backstop is essentially zero.

It is also useful to estimate the average cost per insurance policy. There are about 12 million property insurance policies in place in Canada. This translates into an average cost per policy of about $31 in the first year and increases to roughly $89 after 25 years in the simulation (in 2022 dollars). These premiums will not increase the cost of insurance one-for-one. Current premiums may already contain charges for disaster risk in the range of the DRL, which are now substituted for by the charges from the reinsurance scheme.

For comparison, consider a counterfactual in which private insurance fully covers DRL-level disaster risk. Private insurance would be subject to OSFI’s capital rules, which require that a tail value at risk at 99 percent of the exposure – equivalently, the expected loss in the top 1 percent of losses – is covered by a combination of capital and reinsurance.

The estimation puts this value at roughly $10.5 billion. Assuming a 12 percent ROE, insurers would need to charge roughly $1.26 billion in premiums, or about $105 per policy (in 2022 dollars). Private insurance against natural disasters will therefore be more expensive.

This basic calculation is likely to overestimate the benefits of a public reinsurance scheme for consumers for three reasons. First, some existing insurance contracts already include partial disaster coverage. Second, the scheme would add administrative costs that must be passed on to consumers. Third, private insurers already hold capital and reinsurance – albeit at a lower level – for lower risk layers. Notwithstanding, transferring risk in the layer of $2-10 billion to the reinsurance scheme could offer significant savings for consumers.

Total premiums must be allocated across consumers based on exposure to natural hazards. As a result, price changes will vary across consumers. With mandatory coverage, people without coverage will see their prices increase. Also, people in high-risk areas will face higher charges than people in low-risk areas. As a consequence, some people may see their premiums increase, while others may see theirs decline, but pricing would better reflect underlying risk, with the average policyholder likely benefiting from more complete coverage.

Premiums and Reserves for the CATL

For the CATL, there are no historical data to estimate the frequency and the severity of an event. Instead, the analysis uses earthquake scenarios outlined earlier. Pricing aims to build sufficient reserves over time to cover a certain portion of future losses. The expected losses from the two scenarios over the next 50 years are $17.7 billion and $6.9 billion. The analysis assumes the contingent capital that the reinsurance scheme is expected to put at risk is equal to the total of these two amounts. Applying an 8 percent cost of capital is thus equal to 0.08 x ($17.7 billion+$6.9 billion), or $1.968 billion. This serves as a basis to calculate the overall required premiums for Canada.

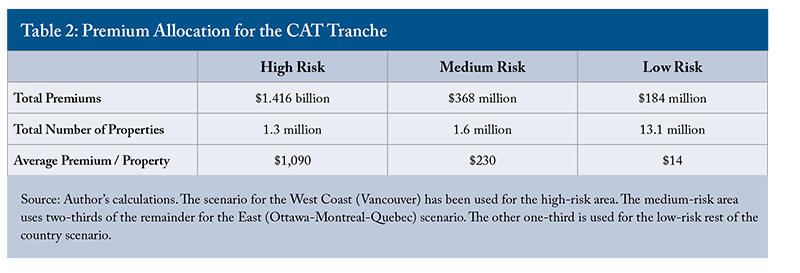

To illustrate how costs pass through to consumers, the calculations divide Canada into three risk regions: a high-risk area (e.g., Vancouver), a medium-risk area (Ottawa-Montreal-Quebec), and a low-risk area, which is the rest of the country. Table 2 shows the amount of the total premiums per year that need to be recovered from the three areas. Note that the aggregate total premiums equal the estimated expected loss per year.

These premiums would apply on top of existing coverage for customers without earthquake insurance and assume no deductible. Clearly, the allocation of premiums ensures that people in the high-risk area pay more. Note that all customers pay a premium for the CATL, even though earthquake risk is negligible for some customers. The reason is that losses above $10 billion automatically bounce from the DRL into the CATL. In such an event, premiums in this layer would also need to be adjusted to recover such losses.3535 Note that natural disasters with losses above $10 billion are estimated to be very rare, accounting for only about 0.3 percent of all natural disaster events.

It is again instructive to compare these costs for customers with a high-quality private alternative. Capital regulation, such as OSFI’s B-9 guidelines, requires insurers to put aside enough capital or purchase reinsurance to cover a one-in-500 event according to a probability-of-maximum loss (PML) calculation. This would lead to massive premiums as the required capital would be astronomically high. For example, assuming a 12 percent ROE and $59 billion in exposure covered by private capital, the average premium charged would need to be more than $5,000 for the high-risk region, or more than five times higher than under the public reinsurance scheme. This simply shows that such risk is uninsurable without a public backstop.

Conclusion

A federal backstop for natural disaster risk is a sound economic idea and should be an essential feature of Canada’s P&C insurance market. An efficient design would feature a reinsurance scheme backed by the government’s soft budget constraint. Its capacity to borrow and spread losses over time makes it a much cheaper solution than putting up private capital to cover extreme risks associated with natural hazards. More affordable premiums may follow as a result.

From this starting point, implementation falls to the federal government. The Department of Finance needs to develop a framework for mandatory insurance and build the infrastructure to price the reinsurance arrangement. Several core functions are required. First, it needs to (in cooperation with the industry) carry out a comprehensive mapping of hazards across Canada. Second, it needs to build up expertise in rate making to ensure that the pricing of reinsurance properly trickles through to consumers. Third, it needs to set up the expertise to manage its borrowing capacity and reserve funds.

Even with these elements in place, there remain some additional issues to tackle in ensuring a well-functioning backstop. The most important issue is its legal structure. A separate Crown corporation to operate the scheme seems best.3636 The alternative is to have an existing independent Crown corporation in charge of its management. Possibilities could be the CPPIB, the Bank of Canada or CMHC, all managing large portfolios of investments already. In an earlier contribution, Le Pan (2016) argues for an industry driven scheme where PACICC takes on the role to cover systemic risk for the Canadian P&C insurance industry. Another issue is setting up a credit line arrangement with the federal government. Here, a special-purpose vehicle that borrows from capital markets seems the optimal solution, with the federal government guaranteeing the debt issuance. Finally, an audit regime is necessary, which ideally reports back to Parliament. Prominent areas would include cost oversight, actuarial soundness, and investment performance.

There are also challenges. First, provincial jurisdiction over insurance markets needs attention. The backstop deals with solvency issues where OSFI already has primary oversight. But costs need to be passed through to consumers, a matter that falls under the mandate of provincial regulation. Also, expected costs per insured dollar will vary across provinces, which can be hard to sell in negotiations with the provinces. Here, a broad backstop covering all natural disasters may be a selling point. Finally, the idea of mandatory coverage, even with an opt-out clause, may be a hard political sell to the electorate.

Natural hazards, be they moderate or major, have become a serious concern for Canadians, with no expected relief in the foreseeable future. Let us make sure we address these concerns in the best possible way. A federally backed reinsurance scheme, together with mandated insurance coverage, would not only provide a better product for the average consumer at a lower price point but also be a prudent and efficient risk management choice for Canada.

The author extends gratitude to Mawakina Bafale, Mary Kelly, Anne Kleffner, Jeremy Kronick, Peter MacKenzie, Mark Zelmer, and several anonymous referees for valuable comments and suggestions. The Insurance Bureau of Canada and CatIQ kindly provided some of the data used in the empirical section of this Commentary. The author retains responsibility for any errors and the views expressed.

Appendix

Excess-of-Loss Contracts

An excess-of-loss contract (XOL) is a standard reinsurance product. It cedes losses from the purchaser to the reinsurer whenever the loss L exceeds a certain threshold T, commonly called the trigger. Exposures to the loss are often capped at a level C for the reinsurer. Mathematically, the payout P from the XOL contract is then given by

P = max(0, min(L – T, C – T).

There is a deductible for the insurer in the amount of L. If losses are below T, there is no payout. If losses are above T, the excess L – T is paid out up to a maximum of C – T. One can rewrite the above equation as

P = max(0, L – T) – max (0, L – C).

The contract thus mirrors the payoff of two call options at maturity, buying one with strike price T and selling one with strike price C, which is commonly referred to as a bull call spread.

For the reinsurance scheme, a key difference to a regular XOL contract is that the loss events – and hence the trigger – are not insurer-specific, but industry-specific. Furthermore, the pricing of reinsurance will take into account that the pricing of the XOL contract is on a yearly basis, but for an unlimited number of events within that horizon. Hence, premiums will also reflect the expected number of yearly events that fall in the range of the contract.

Pricing of the Contracts

The pricing of such contracts has three components.1 First, a pure premium is calculated that takes into account the frequency and severity of tail events. Next, this premium is adjusted for an expense ratio and a return on investment of the premiums, reflecting operating costs and returns on investing premiums. Finally, one needs to take into account the capital the backstop puts at risk, which needs to be compensated with a return.

The mathematical details for the pricing are given by

where L is the expected loss per event, T is the trigger, e is the expense factor, and rf is a discount rate over the length of the contract, which is one year. The last expression includes the capital at risk adjustment, where rc is a required return on capital (ROE).

The first part of the formula is standard and expresses the net present value of the expected payouts, taking into account the expenses from underwriting. The advantages of having the government provide the backstop enter through the second term and reflect the ability to spread risk over time with less solvency concerns.

1 An alternative would be to use option pricing given the structure of the contract.

REFERENCES

Aon. 2025. “Reinsurance Market Dynamics – Midyear 2025 Renewal.” Report.

Campbell, Alistair. 2024. The High Price of Prudence – Benchmarking Canada’s Property and Casualty Industry. Commentary 671. Toronto: C.D. Howe Institute.

Canada Council of Insurance Regulators. 2023. “Climate Change, Natural Catastrophes and Consumer Awareness.” Position Paper.

Cassidy, J., C. Rogers, M. Lamontagne, S. Halchuk, and J. Adams. 2010. “Canada’s Earthquakes: ‘The Good, the Bad and the Ugly.’” Geoscience Canada 37(1): 1-16.

CatIQ. 2022. “Flood Insurance Take-up in Canada, 2021.”.

Congressional Budget Office. 2024. “Climate Change, Disaster Risk and Homeowner’s Insurance.” Report.

Cummins, David J. 2006. “Should the Government Provide Insurance for Catastrophes?” Federal Reserve Bank of St. Louis Review 88(4): 337-379.

Cummins, David J., Christopher M. Lewis, and Richard D. Phillips. 1999. “Pricing of Excess-of-Loss Reinsurance Contracts.” In K. Froot (ed.),

The Financing of Catastrophe Risk. University of Chicago Press.

Dahlby, Bev. 2008. The Marginal Costs of Public Funds. MIT Press.

Dionne, Georges (ed.). 2013. Handbook of Insurance. 2nd edition. Springer.

Froot, Kenneth A. (ed.). 1997. The Financing of Catastrophe Risk. The University of Chicago Press.

Froot, Kenneth A. 2001. “The Market for Catastrophe Risk: A Clinical Examination.” Journal of Financial Economics 60: 529-571.

Froot, Kenneth A., and Jeremy C. Stein. 1998. “Risk Management, Capital Budgeting, and Capital Structure Policy for Financial Institutions: An Integrated Approach.” Journal of Financial Economics 47(1): 55-82.

Gallagher Re. 2025. Reinsurance Market Report 2024.

Government of Canada. N.d. “Canada’s National Earthquake Catalogue.”

Hanson, Samuel, David Scharfstein, and Adi Sunderam. 2019. “Social Risk, Fiscal Risk and the Portfolio of Government Programs.” Review of Financial Studies 32(6): 2341-2382.

Harrington, Scott E., Greg Niehaus, and Tong Yu. 2013. “Insurance Price Volatility and Underwriting Cycles.” In G. Dionne (ed.), Handbook of Insurance, 2nd edition. Springer.

Insurance Bureau of Canada. 2013. “Study of Impact and the Insurance and Economic Cost of a Major Earthquake in British Columbia and Ontario/Quebec.” Report.

________________. 2015a. “A Primer on Financial Risk from Natural Disasters: The Case for Public-Private Collaboration.” Report.

________________. 2015b. “Preparing Canada for an Earthquake – A National Conversation.” Report.

________________. 2023. “Facts of the Property and Casualty Insurance Industry in Canada.”

Kelly, Grant, Zhe Peng, and Ian Campbell. 2024. “When it Rains it Pours …” PACICC report.

Kelly, Mary, Anne Kleffner and Grant Kelly. 2020. “An examination of catastrophes, insurance guaranty funds and contagion risk.” The Geneva Papers on Risk and Insurance – Issues and Practice (45): 256-280.

Kelly, Mary, Anne Kleffner, and Lori Medders. 2025. “An examination of catastrophe insurance programs: elements that support program resilience.” The Geneva Papers on Risk and Insurance – Issues and Practice.

Koeppl, Thorsten V., and James C. MacGee. 2015. Mortgage Insurance as a Macroprudential Tool: Dealing with the Risk of a Housing Market Crash in Canada. Commentary 430. Toronto: C.D. Howe Institute.

Le Pan, Nicolas. 2016. Fault Lines: Earthquakes, Insurance, and Systemic Financial Risk. Commentary 454. Toronto: C.D. Howe Institute.

Lewis, Christopher M., and Kevin C. Murdock. 1996. “The Role of Government Contract in Discretionary Reinsurance Market for Natural Disasters.” Journal of Risk and Insurance 63(4): 567-597.

McGillivray, Marissa. 2024. “Insights into the impact of extreme weather trends in Canada on homeowners insurance profitability and consumers.” Analysis in Brief. Statistics Canada.

Parliamentary Budget Office. 2025. “Projecting the Cost of the Disaster Financial Assistance Arrangements Program.” Report.

Schlesinger, Harris. 2013. “The Theory of Insurance Demand.” In: G. Dionne (ed.), Handbook of Insurance, 2nd edition. Springer.

Swiss Re. 2024. “Natural catastrophes in 2023.” Sigma 01/2024.

_______. 2025. “ILS Market Insights.” February 2025.