by Alexandre Laurin

- Canada increasingly uses the tax system to deliver income-tested benefits, making filing essential for access. Budget 2025’s “automatic federal benefits” initiative aims to expand participation but largely targets individuals already known to the Canada Revenue Agency and participating in the tax system. This limits its reach when it comes to truly hard-to-engage non-filers. About 3.6 percent of potential filers, roughly 1.2 million people in 2023, are unlikely to file, though not all are eligible for benefits.

- Non-filing is a relatively narrow but complex problem driven largely by behavioural barriers like distrust, administrative challenges, and concerns about informal income rather than filing costs alone. Existing automation tools such as SimpleFile have seen persistently low uptake (3-11 percent), suggesting limited success in reaching hard-to-engage populations.

- The scope for automatic tax filing in Canada is constrained by system complexity. Many deductions, credits, and income-tested benefits require taxpayer-reported information, including key details such as expenses and family circumstances that the CRA does not hold, meaning only a minority of returns (roughly one-third) can be fully automated. International experience, particularly from the UK, shows that automation works best in simpler systems and still requires ongoing taxpayer input.

- While targeted automation may reduce compliance costs for some low-income filers, it is unlikely to significantly improve benefit uptake among non-filers. More meaningful progress will likely require broader reforms, including simplifying the tax system and reconsidering the link between tax filing and benefit delivery.

Introduction

Canada increasingly uses the personal income tax system to deliver income-tested benefits to households. As a result, filing a tax return has become a prerequisite for receiving many forms of financial support, including the Canada Child Benefit, the GST credit (now the Canada Groceries and Essentials Benefit), and the Canada Workers Benefit. This has driven growing interest in policies aiming to expand tax participation by simplifying compliance and reducing barriers to filing, particularly for low-income individuals. In some countries,11 Laurin and Dahir (2022) review international tax filing systems and find that employees in countries such as Argentina, Costa Rica, Chile, Germany, Ireland, Peru, and the United Kingdom are generally not required to file a return when employment income is their sole source of income. such as the United Kingdom, most people do not file an annual tax return, which has led some to ask whether Canada could move in a similar direction.

Recent federal budgets have proposed expanding the use of automatic, or Canada Revenue Agency (CRA)-prepared, tax returns to help vulnerable individuals access benefits more easily. Budget 2025 goes further with its “automatic federal benefits” initiative, which aims to simplify filing for targeted individuals with no tax liability in straightforward situations. By easing compliance for selected filers, and potentially filing on behalf of a still-to-be-defined subset, the government seeks to increase tax participation and, in turn, extend benefits to more eligible Canadians who currently remain outside the tax system.

This paper first reviews how Canada’s tax-filing system operates and compares it with the United Kingdom’s experience. It then examines the extent of non-filing, estimating that the rate – about 3.6 percent of potential filers, or roughly 1.2 million individuals in 2023 – is lower than commonly reported, largely due to late filing and related factors. This does not diminish the issue, however. The characteristics and behavioural barriers among non-filers point to a relatively narrow policy challenge, one that is unlikely to be meaningfully addressed by broad-based automation initiatives that primarily target individuals already participating in the tax system.

Recent data show very modest uptake of the CRA’s existing automation initiatives, File My Return and SimpleFile, highlighting the limits of this approach. Participation in SimpleFile remains far below the roughly one million returns completed annually through volunteer tax clinics. This suggests that CRA phone and digital tools alone are unlikely to be effective in reaching hard-to-engage, disadvantaged populations, some of whom may lack trust in the Agency.

Regardless of their impact on tax participation, CRA automation tools have broad support for their perceived potential to reduce compliance costs. This paper argues, drawing on the UK experience, that successful automation is closely linked to tax simplicity. Canada’s complex federal-provincial system, with its many tax and benefit provisions requiring direct taxpayer input, makes automatic filing difficult for most individuals. While AI-driven innovations may ease compliance in the short term, meaningful progress will require substantial simplification of the tax system by both federal and provincial governments.

The policy discussion concludes by examining alternative approaches the government could use to improve the delivery of income-tested benefits to vulnerable non-filers. Enhancing access may require decoupling benefit eligibility and administration from the requirement to file a tax return. A dedicated body, operating at arm’s length from the CRA and focused on administering benefits, could more effectively reach and engage hard-to-reach populations.

A Portrait of Canada’s Tax-Filing System

The CRA – with Revenu Québec operating a parallel system – provides multiple ways for individuals to file personal income tax returns, depending on eligibility and preferences. Taxpayers may file on their own, electronically or on paper, or authorize a representative – such as an accountant, tax preparation firm, or trained volunteer – to file on their behalf.

Electronic Filing by Individuals and Representatives

Canada operates a self-assessment tax system, with electronic filing now dominant (93 percent of returns).22 CRA filing statistics for the 2025 filing season, all returns, as of March 2026. The CRA supports two electronic filing channels: NETFILE for individuals and EFILE for authorized preparers. Both rely on CRA-certified commercial tax software.

EFILE remains the primary filing method (60 percent), reflecting the widespread use of professional tax preparation services, while NETFILE has grown with improved software and online access (33 percent).

Auto-fill My Return (Pre-Population of Tax Returns)

The CRA offers Auto-fill My Return, an optional service through certified software that pre-populates parts of a return using third-party data, including benefit payments and registered savings contributions, and amounts from T4, T3, and T5 slips (e.g., employment, pension, and investment income, and withdrawals from registered savings).

To use Auto-fill, individuals must register for the CRA’s secure online portal, My Account, while representatives access the same functionality through the Represent a Client portal. Filers can accept or modify pre-filled data. Although the CRA has expanded the range of pre-populated information, the system stops short of generating a completed return.

More than 19.3 million individuals used Auto-fill to complete their 2024 return (about 61 percent of filers),33 Number of Auto-fill users (19.3 million) retrieved from a May 8, 2025, CRA media release, “The tax-filing deadline has passed, but you can still file your 2024 income tax and benefit return.” Number of 2024 tax returns processed (31.9 million) obtained from CRA filing statistics as of March 2026. illustrating significant uptake. However, because the CRA does not publish annual Auto-fill usage statistics in its regularly updated filing statistics, obtaining a consistent and more detailed annual picture of usage is difficult.

Assistance for Low-Income Filers

Low-income filers have some resources they can use to help them file their tax returns in simple situations.

SimpleFile (formerly File My Return)

The CRA offers a fully automated filing option for selected individuals with low or fixed incomes, typically those with very simple situations and little or no tax liability. Formerly known as File My Return (FMR), the service has since been rebranded as SimpleFile (SFS). The rebranding to SimpleFile (SFS) is part of a broader CRA effort to frame the program as a step toward automatic tax filing, but participation has remained limited and, up to the 2025 tax season, invitation-based. Eligible individuals are invited by the CRA to file for free, typically by phone or more recently through a simplified digital process, without completing a conventional tax return. Since 2026, individuals can complete an online questionnaire to verify their eligibility without first receiving an invitation. A key requirement is having income below $12,747 ($23,045 for those eligible for the disability tax credit) for Ontario residents under 65, from specified sources.44 Employment on T4 slips, OAS, GIS, C/QPP, EI, interest on T5 slips, social assistance, and workers’ compensation benefits.

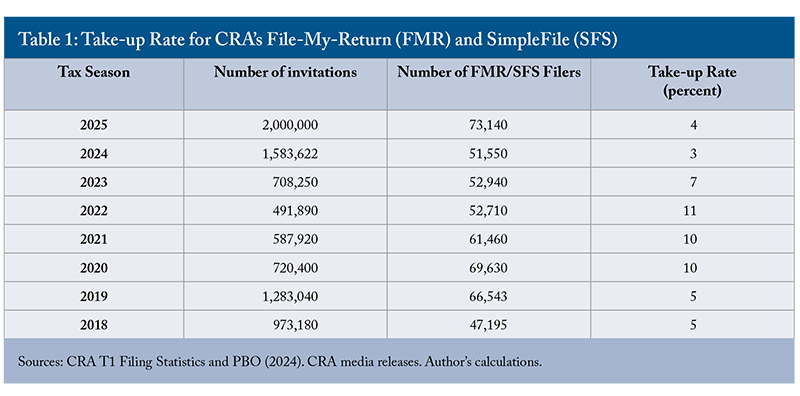

Despite its automation, take-up has historically been very low relative to the number of invitations sent. The CRA’s regular tax-filing statistics provide the number of tax returns completed via FMR/SFS, while invitation data come from the Parliamentary Budget Officer (PBO) (PBO 2024). About 2 million invitations to use SFS were sent for the 2025 tax season, yet only 73,140 filers participated for a meagre 4 percent take-up rate. Results for prior years are not more encouraging, with 51,550 filers participating in 2024 despite 1.5 million invitations (Table 1).55 Starting with the 2023 tax year, Revenu Québec introduced a similar simplified tax filing program. In the 2024 filing season, only about 4,000 individuals used the program (Revenu Québec 2025), indicating similarly low uptake. However, the Quebec program is still relatively new. The take-up rate has oscillated between 3 and 11 percent, with little relationship between the number of invitations and participation.

A CRA-commissioned study helps explain low participation in the simplified filing system (CRA 2022). Many participants are repeat filers who return to SFS year after year, reflecting persistent filing habits. Some already rely on free alternatives such as community volunteer tax clinics (see below) or have a family member or friend prepare their return, reducing the perceived benefit of switching to a CRA-prepared option. Others prefer to file jointly with a spouse and use a tax preparer, especially when the spouse is ineligible for SFS or has a more complex return (CRA 2022). The PBO reports that for the 2023 filing season, about half of SFS invitees used a tax preparation service, while about a fifth used community volunteers (PBO 2024).

The invitation process is partly responsible for the low take-up. To receive an invitation, a tax filer must have a recent history with the CRA because the agency must establish a pattern of filing simple tax returns from year to year. Thus, presumably almost all are already filers. It is unclear whether any SFS filers did so for the first time as a result of the invitation, but certainly it appears clear from the data that most would have filed anyway, although they found the simplified method more practical.

For the 2024 tax season, only 3 percent of the SFS invitees filed a tax return using SFS, while about 90 percent filed through other methods, and roughly 7 percent did not file.66 The Ombudsperson reports that 93 percent of the invitees had filed (Canada 2025). This non-filing rate is broadly similar to that of the overall population (Table 2 below), leaving doubts on the efficacy of the SFS invitations to increase tax filing participation.

Community Volunteer (Free) Tax Clinics

Individuals with modest incomes and simple tax situations may also file through community volunteer tax clinics, where trained volunteers prepare returns free of charge using commercial tax-preparation software provided to participating organizations. The program is funded by the CRA. Prior to the COVID-19 pandemic, these clinics prepared more than 800,000 returns annually. Although in-person volunteer activity was disrupted during the pandemic, services gradually resumed in subsequent years. By 2025, community volunteers prepared over one million tax returns. These clinics remain the primary source of filing assistance for low-income individuals, despite the CRA issuing about 2 million invitations to low-income taxpayers to use its own automated SimpleFile services.

Paper Filing

Paper filing is still available but now accounts for a small share of returns – 7 percent in 2025, down from 16 percent in 2016. It is used primarily by individuals who still prefer non-digital methods, with limited digital access, or are required to file paper returns due to specific circumstances. Because most commercial tax software allows users to print completed returns for mailing, paper filing no longer implies manual completion. As a result, it is reasonable to infer that only a very small number of returns are now filled out by hand using mailed paper forms.

A Look at the United Kingdom

International experience shows that countries with widely used automatic or return-free filing tend to have a simpler personal income tax system than Canada in terms of the number of credits and deductions, and other provisions, that are generally claimed by most employees.

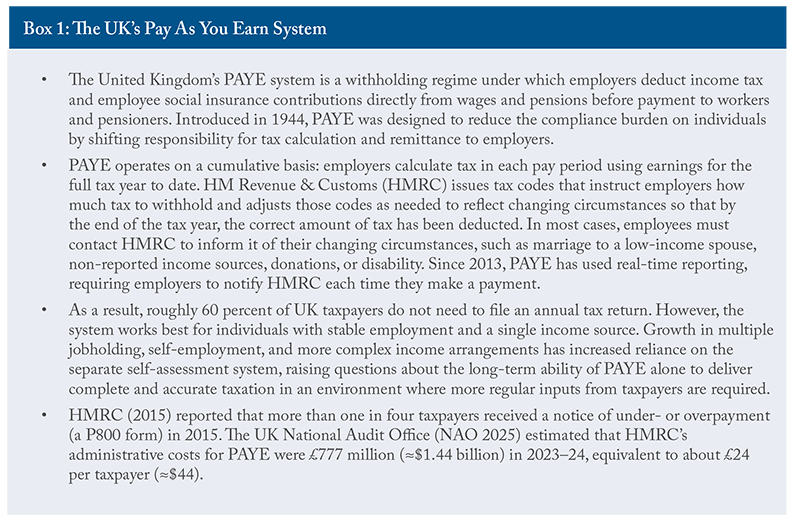

The United Kingdom is a particularly instructive case. For most employees and pensioners with no other major sources of revenue, income tax is assessed entirely through the Pay As You Earn (PAYE) withholding system (see Box 1), eliminating the need to file an annual return. This system works in part because the UK relies less on deductions or taxpayer-reported credit amounts.

Self-employed individuals, high-income individuals, landlords, and others for whom employment or a pension is not a major source of income generally have to file an annual tax return. For PAYE taxpayers, however, their input is required only to claim a small set of reliefs, such as the marriage allowance, blind person’s allowance, charitable donations, and certain employment expenses.

Another source of simplification is that most people can earn some taxable interest and dividends up to an allowance without having to report and pay tax on this income. For higher levels of taxable investment income but below a £10,000 threshold, taxpayers may contact the tax administrator to have the tax garnished from their wages through the PAYE system. Individuals with income from savings and investments over £10,000 (about $18,500) must file a return. The capital gains tax is administered separately and requires the taxpayer to file with the tax administrator.

Childcare supports and other income-tested transfers in the UK are administered largely outside the personal income tax system. The main means-tested benefit for families, Universal Credit, is administered by the Department for Work and Pensions, not the tax authority, and must be claimed through a separate application process.

Comparable benefits in Canada include the Canada Child Benefit, the GST Credit (recently renamed the Canada Groceries and Essentials Benefit), and the Canada Workers Benefit, all of which require the filing of a tax return in order to establish eligibility and calculate entitlements.

In the UK, parents who are not eligible for free childcare may receive financial support through “Tax-Free Childcare.” Despite its name, this program is also administered separately from income tax assessment. Parents apply to open a dedicated online account, from which approved childcare providers are paid. For every £8 deposited by parents, the government contributes £2, up to an annual maximum.

In contrast, in Canada, tax relief for childcare is provided primarily through a deduction for eligible childcare expenses. In addition, Quebec and Ontario offer refundable tax credits. All of these supports are delivered through the income tax system and therefore require the filing of a tax return.

Canada: From Automatic Tax Filing to Automatic Federal Benefits

The September 2020 Speech from the Throne committed the federal government to “work to introduce free, automatic tax filing for simple returns to ensure citizens receive the benefits they need.” Subsequent budgets from 2023 to 2025 and the 2024 Fall Economic Statement have refined this commitment.

Since 2023, the CRA’s automatic tax filing efforts have focused on its SimpleFile service. It has also run pilot projects inviting individuals who had never filed a tax return or had a significant gap in filing to submit their returns over the phone, digitally, or on paper.

These efforts culminated in Budget 2025, which reframed the commitment from “automatic tax filing” to “automatic federal benefits.” The new approach introduces two streams: pre-filled income tax returns for known filers and deemed filing for selected candidates identified by the CRA (Canada 2026).

Under the first stream, the CRA will prepare pre-filled tax returns in its My Account online portal for about 1 million lower-income individuals with simple tax situations starting in the 2026 tax year, expanding to roughly 5.5 million individuals by 2028. These are tax filers already known to the CRA, presumably with a history of non-taxable returns (returns for which no income tax is owed).77 In the 2023 tax year, almost 9 million individuals had non-taxable returns.

Under the second stream, Ottawa proposes amending the Income Tax Act to allow the CRA to file tax returns on behalf of certain eligible lower-income individuals with simple tax situations who do not owe tax and have not filed. Budget 2025 suggests that individuals selected for the deemed filing stream will be drawn from the pool of pre-filled returns in the first stream (Canada 2026, p. 162).

Eligible individuals would generally:

- have taxable income for the year below the basic personal amount (plus any applicable age or disability amounts);

- receive all of their income from sources for which information slips have been filed with the CRA, such as employment, social assistance, or public pensions;

- have failed to file a return in at least one of the three preceding taxation years;

- have not otherwise filed a return for the year before, or within 90 days after, the filing deadline.

Under the proposal, eligible individuals would have 90 days to review and amend the information provided by the CRA. Since they would receive notification through authenticated CRA portals and must verify their identity before accessing the proposed return, they are presumably already registered with My Account (Canada 2026). If they do not respond, the CRA could file a return on their behalf, issue a notice of assessment, and determine their credit and benefit entitlements.

But it is unclear how many individuals would qualify, since accurate benefit payments often require confirmation of marital status and spousal information. Without such confirmation, it is unclear how the CRA could reliably file a return. Significant screening of past tax returns will be required, since candidates for deemed filing will be considered complex tax situations by the CRA (Canada 2026).

How Large Is the Non-Filer Population and Will the Policy Reach Them?

To receive cash benefits such as the Canada Child Benefit (CCB), the GST credit, the Canada Workers Benefit, or the Guaranteed Income Supplement, individuals must file a tax return. Those who do not file receive no benefits for those years, although they may receive retroactive payments if they file later – up to 10 years for the CCB and generally up to 11 months for the GIS.

The policy problem is that some Canadians in need fail to participate in the tax system and therefore miss benefits they may be entitled to. This issue is particularly concerning for vulnerable individuals, whose missed benefits could make a sizable difference to their living standards.

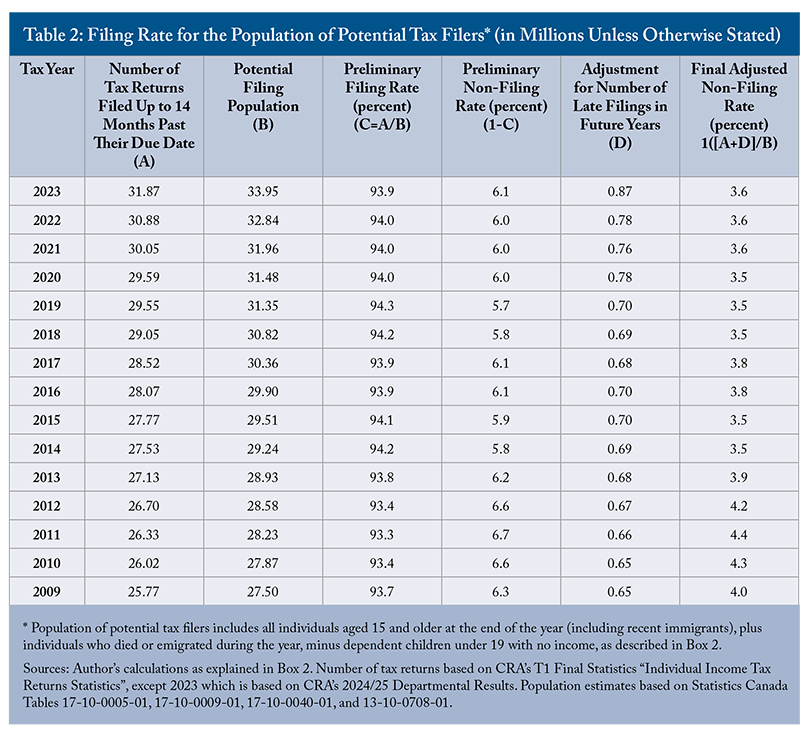

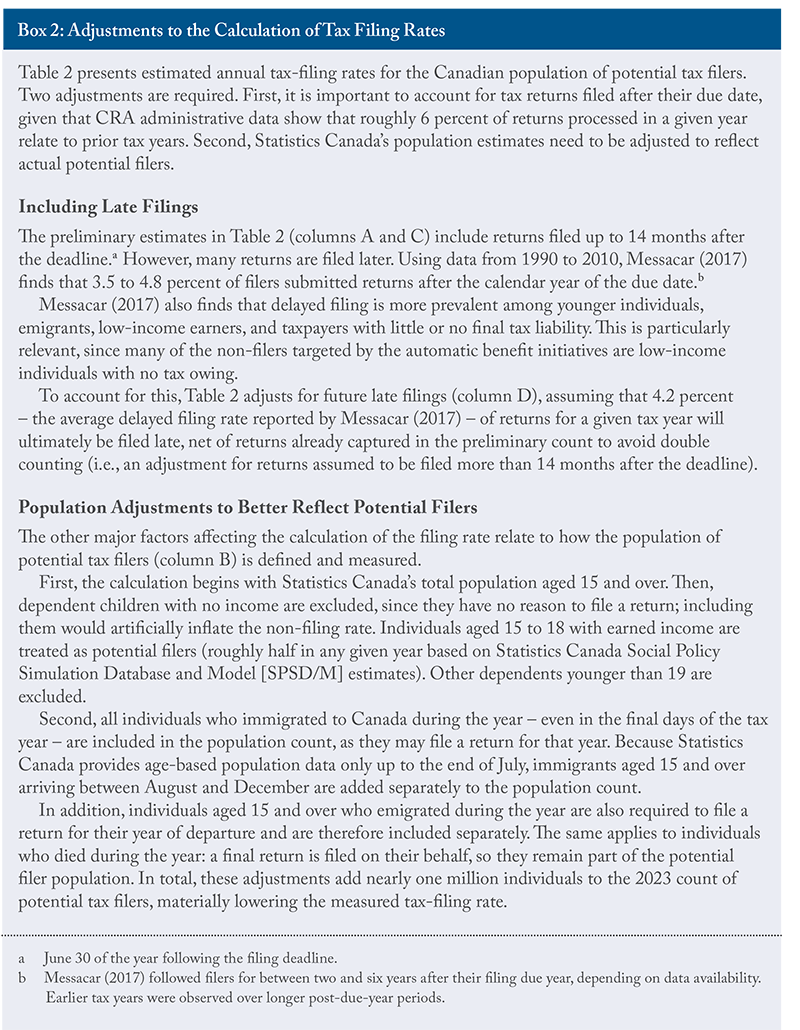

Calculating tax-filing rates for the Canadian population is not straightforward. It is complicated by the possibility of late filing, by the presence of dependent children for whom filing a return is not required, and by population groups such as emigrants, recent immigrants, and recently deceased individuals that affect the population of potential tax filers. Please see Box 2 for details on how these factors are accounted for in Table 2.

The estimates in Table 2 present non-filing rates for 2009 to 2023. Without adjusting for very late filing, approximately 94 percent of potential filers submit a return within 14 months after the filing deadline. This rate has remained stable over time. When estimated late returns filed more than 14 months past the deadline are also taken into account, the effective filing rate rises to 96.4 percent. This implies that roughly 3.6 percent of potential filers – about 1.2 million individuals in 2023 – did not (or are unlikely to) file a return.

Not all non-filers would be entitled to cash benefits. For example, some employees with sufficient tax withheld at source may overlook filing a tax return, but they may not qualify for income-tested benefits. In 2023, about 425,000 potential filers were recent emigrants or deceased and thus not eligible for cash benefits. A further 2.3 million were temporary residents (excluding protected persons), many of whom were ineligible for benefits such as the CCB.

A CRA (2024) study, conducted with Statistics Canada and Employment and Social Development Canada (ESDC), compares filing rates across population groups to identify those eligible for benefits but who are harder to reach.88 The tax filing rates of interest were calculated for the population aged 18 years and over because, for the same reason, an adjustment is made in Table 2, including 15- to 17-year-olds – many of whom are not required to file – would bias the results. Because the study excludes returns filed more than eight months after the deadline, its general population filing rate of 92 percent is consistent with the 94 percent preliminary rate reported in Table 2.99 Excluding the more than half a million returns filed during the additional six months included in the preliminary rate calculation in Table 2 reduces the filing rate in Table 2 from 94 percent to 92 percent.

Interestingly, seniors exhibit a very high filing rate, with 97 percent filing within the due year (the rate would be even higher if all late filers were included). Newcomers to Canada, who might be expected to have lower participation, file at rates similar to those of the general population (CRA 2024).

So, who is less likely to file? The CRA (2024) results are not surprising in light of the existing academic literature on the characteristics of non-filers (Robson and Schwartz 2020). Indigenous Peoples are about 7 percent less likely to file than the general population, while adults under 30 and housing-insecure individuals are each about 6 percent less likely to file (CRA 2024). These categories are not mutually exclusive: the same individual may belong to more than one group, and the data do not allow us to determine which characteristic, if any, has the dominant effect. It is safe to conclude, therefore, that individuals who combine these characteristics – for example, a young, housing-insecure Indigenous adult – are substantially less likely to file.

Low income is also associated with lower filing rates, as noted by both the CRA (2024) and Robson and Schwartz (2020). However, individuals with the characteristics discussed above are also more likely to have low incomes. Importantly, Robson and Schwartz (2020) find that, once other individual characteristics are taken into account, low income on its own does not significantly increase the likelihood that working-age adults fail to file.

In light of the non-filing statistics, the policy problem of individuals missing cash benefits because of non-filing is both complex and relatively narrow in scope, and therefore calls for targeted solutions. While the Budget 2025 “automatic federal benefits” initiative is more focused than universal automatic filing, it still casts a wide net. It does not appear aimed at hard-to-reach individuals: the 5.5 million people targeted for pre-filled returns are already known filers, and the initiative will face many of the same implementation challenges as universal automatic filing.

Implementation Challenges

Automatic tax filing could improve benefit delivery and reduce filing barriers, but its implementation in Canada faces two major constraints: the complexity of the tax system and non-financial factors such as behavioural resistance and capacity issues.

Tax Complexity

The primary implementation challenge is the complexity of Canada’s personal income tax system. Fortin (2023), after examining European experiences (in particular those of the UK and Finland), finds that a large part of the feasibility of tax automation depends on the simplicity of the tax system. Finland, which operates a highly automatic tax filing system, has one of the simplest tax systems in the world. Significant tax simplification reforms accompanied its evolution towards greater automation (Fortin 2023).

Truly automatic tax filing can work reliably only when the tax authority already holds the information needed to calculate taxes and benefits accurately. In practice, this condition is rarely satisfied, at least for taxable filers. Although third-party reporting provides the CRA with information on major income sources such as employment earnings, pensions, government transfers, and most investment income, important categories remain outside the reporting system, including self-employment income, rental income, many capital gains, certain foreign income, and spousal support receipts (Laurin and Dahir 2022).

Deductions and credits add further complexity. Claims for childcare expenses, moving costs, employment expenses, work-from-home expenses, investment carrying charges, or business activities require information that the CRA does not have. Likewise, numerous credits depend on personal expenditures or circumstances that must be actively reported, including medical expenses, disability eligibility, charitable donations, some tuition payments, caregiving responsibilities, and various sector-specific incentives. Provincial credits add an additional layer of information requirements.

When these elements are considered together, Laurin and Dahir (2022) estimate that only about one-third of potential Canadian filers would have a truly “basic” return that the CRA could complete using available information (provided essential information on marital status and housing characteristics is confirmed). More recent research based on administrative data reaches a similar conclusion, suggesting the CRA could automatically file returns for roughly 29 percent of families (Genest-Grégoire et al. 2024).

The scope for automation also declines as income rises. Laurin and Dahir (2022) find that nearly half of filers in lower-income families (under $50,000) have a basic tax return. Using detailed income groupings, Genest-Grégoire et al. (2024) show that more than half of families in the bottom 20 percent of the income distribution have no source of tax complexity and could likely be assessed automatically, compared with 20 percent or less among the top 50 percent of families by income.

For determining eligibility for cash benefits, most of which depend on net family income, Laurin and Dahir (2022) find that the CRA would have enough third-party financial information to calculate income-tested cash benefit entitlements for nearly 70 percent of individuals in families earning under $50,000. Genest-Grégoire et al. (2024) similarly find that about three-quarters of families relying on social assistance have no source of tax complexity.

These estimates have limitations. They reflect a single year, while individuals’ circumstances change over time, reducing the share of consistently “simple” filers. The CRA also requires basic, up-to-date information on filers – such as contact details, address, household composition, marital status, and the names of spouses and children. For non-filers and hard-to-reach individuals, the CRA cannot be certain that any information it holds is current. This makes it difficult to bring these individuals into the filing system.

Taken together, these findings show that in a system where federal and provincial governments rely extensively on targeted deductions, credits and income-tested provisions tied to specific expenses, sources of income, and personal circumstances, meaningful progress toward automatic filing would require substantial tax simplification. Automation does not eliminate the need for taxpayer input.

On the other hand, technological changes like advances in artificial intelligence (AI) may ease some of these constraints. As record-keeping becomes more digital, compliance may become easier to manage. As Young (2024) notes, “The near future may be uncertain, but transformational change in the tax world, driven by technology, seems certain to arrive in time.” Electronic invoicing and other private-sector innovations may also expand third-party reporting, simplifying compliance for individuals and businesses (Hawara 2024).

AI could further improve the filing experience by building on increasingly digital transactions and economic activity. Tax software providers and preparers will most likely contribute to this change. It remains unclear, however, whether the most significant advances will come from industry or from governments, particularly if the latter seek to build large, centralized data and tax-optimization systems capable of handling increasingly complex economic lives and tax rules.

Behavioural Resistance and Capacity-Related Factors

While automatic tax filing is often presented as a technical or administrative reform, behavioural factors remain a central challenge, particularly for vulnerable populations. As Laurin and Dahir (2022) explain, multiple non-financial barriers affect filing behaviour. These include a lack of trust in government, physical or mental health problems, potential unpaid taxes that individuals wish to avoid, limited self-confidence or administrative capacity, and cultural or language barriers.

Many CRA online and telephone services require identity verification based on information from prior tax returns or official records. This can be difficult for vulnerable individuals who may not recall specific line items from a previous return, may have moved frequently and be unsure of the last address on file, or may face language barriers (Canada 2020).

Stapleton (2018, p. 6), drawing on extensive personal experience, consultations, and focus groups with low-income populations, compiled a “…list of the concerns, both founded and groundless, that make many low-income people skeptical of government and averse to tax filing.” Some stem from misinformation, such as the belief that benefits will be clawed back from social assistance or confusion about how refunds work. Other concerns are rooted in fear that filing might prompt scrutiny of past income sources and expose them to enforcement actions. As Stapleton (2018, p. 7) observes, “Uncertainty is an outsized problem for low income people.”

Informal or casual work adds to this uncertainty. “In our focus groups…everyone on a low income we spoke with…had worked in the informal economy for small amounts of money in service jobs such as home repairs, cleaning, or child care for cash” (Stapleton 2018, p. 7). While these amounts are typically modest, concerns about reporting them may deter filing. At the same time, the potential tax revenue from stricter enforcement in this segment is likely small relative to the administrative cost (Stapleton 2018). Of course, this does not include non-filers who willfully avoid taxes by participating in the underground economy or illicit activities.

These behavioural considerations complicate the promise of automatic filing. Even if returns were prepared automatically, mistrust, fear of enforcement, uncertainty about informal income, and identity-verification barriers could still deter engagement. The very low take-up rate of SimpleFile, fluctuating between 3 and 11 percent of invitees (see Table 1), is a telling example.

Other Challenges

Fortin (2023) identifies many other complicating factors to greater tax filing automation in Canada. Some institutions do not systematically share data used for income tax reporting. Greater integration of third-party information from non-conventional employment, providers of deductible services, or charities receiving donations could facilitate tax filing automation. At the same time, greater data centralization raises significant privacy and cybersecurity risks. This issue, which is ever-present in the United Kingdom, remains a key consideration in the feasibility of automatic tax filing (Fortin 2023).

Cost is a related issue. Building and maintaining the IT infrastructure needed to support large-scale automated filing could lead to overruns and delays, as seen in projects such as the Phoenix pay system and ESDC’s Benefits Delivery Modernization initiative. The CRA also faces scrutiny over service quality. The Auditor General found that call centres provided accurate answers to individual tax questions only 17 percent of the time, often after long wait times (OAG 2025). This does little to build confidence in the CRA’s capacity to automatically optimize tax returns.

Finally, the provincial dimension cannot be overlooked. Quebec administers its own income tax through Revenu Québec, meaning any move toward greater automation would require coordination across federal and provincial systems.

Can Canada Emulate the UK?

At first glance, the UK’s PAYE system looks like a possible template for making taxation “automatic” for most workers and pensioners. Under cumulative withholding, the design objective is that by year-end the accurate tax has been withheld and “the taxpayer does nothing in the way of compliance” (APPTG 2017).

But the UK experience is also a cautionary tale, as over time the PAYE system reacted to labour market changes and additional provisions to be administered by asking for more information and involvement from taxpayers. As the UK Parliament’s All-Party Parliamentary Taxation Group (APPTG) argues, beginning in the 1990s, modern labour markets (job switching, multiple jobs, variable pay, and growth in self-employment) make it increasingly hard for an exact employer-withholding model to “get it right” without continual notifications and corrections from taxpayers. This reality has “underscored the weakness and inflexibility of the PAYE system” (APPTG 2017).

In particular, the growing use of the tax system to deliver transfers (via refundable tax credits) raised error and overpayment risks, in part because the state lacked timely, complete information about people’s circumstances. HMRC’s response was not greater automation, but more taxpayer responsibility, requiring claimants to file a form that “essentially looks like a preliminary tax return” (APPTG 2017).

In effect, as complexity increased, PAYE shifted away from passive automation toward more active taxpayer reporting. Canada faces all the information problems highlighted in the UK case and arguably more, since the CRA serves two orders of government (federal and provincial) and their intertwined tax credits and benefits. As already said, Canada’s high reliance on credits, deductions, and income-tested transfers means that tax optimization requires up-to-date information on family status, caregiving arrangements, disability status, childcare expenses, tuition, moving expenses, medical expenses, transferred credit amounts to spouses and dependent children, and other items such as work-from-home expenses often provided by taxpayers. And as in the UK, rising gig work, multiple jobholding, and income volatility1010 At the end of 2022, roughly 2.4 million Canadians had performed gig work at some point during the previous 12 months, while 0.5 million Canadians had completed digital platform employment in 2023 (Canada 2024). further limit the completeness of third-party data.

True hands-off tax automation in Canada for all would face significant error and tax-optimization challenges, requiring frequent taxpayer engagement to fill gaps. In fairness, the most recent federal government proposal is targeted at selected non-taxable individuals for whom the CRA is likely to have complete income information. Pre-filled returns could make filing easier for these individuals.

CRA-prepared returns for this group are similar to existing tax software with auto-filled slips, except that the task of calculating taxes is performed by the tax authority. The policy question therefore becomes less about feasibility and more about trade-offs. These trade-offs involve error risks and accountability, as well as costs and capacity constraints.

The risk of errors is obvious. The CRA cannot know in advance whether it has complete income information for a filer and their spouse. While statistical inference may reduce this risk for individuals with stable, predictable income, uncertainty remains. Evidence from the UK suggests that “the system has left taxpayers largely disengaged from their tax affairs, which means that errors go unnoticed and accumulate within the tax system” (APPTG 2014).

Pre-filled returns may also create a false sense of completeness, discouraging individuals from reporting additional income. Even when no tax is owing, omissions can affect benefit entitlements. For example, the Canada Workers Benefit is phased in at a rate of 27 cents per dollar of earnings above $3,000, up to a maximum benefit amount. An individual who accepts a CRA-prepared tax return and omits to report a small amount of gig income, assuming it would have no impact on tax payable, could end up leaving more than $1,500 in benefits unclaimed.

On the other hand, the risk of tax avoidance increases when taxpayers accept pre-filled returns that omit income sources the CRA does not observe (Petit et al. 2021). Yet accepting an incorrect return can still expose taxpayers to legal action or penalties. Evidence from a Danish tax audit experiment shows that underreporting is much higher for self-reported income than for income subject to third-party reporting and pre-filled in tax returns (Kleven et al. 2010; Fochmann et al. 2021). In Sweden, many taxpayers who omit income do so because they assume the pre-filled return already reflects all relevant information (FTATSS 2006). In Denmark, failing to correct an incorrectly pre-filled return can itself constitute tax fraud (FTATSS 2006).1111 This raises broader taxpayer rights concerns – particularly for vulnerable individuals with limited digital literacy or language barriers – that warrant particular attention for Canada’s deemed filing proposal. These considerations are especially relevant to Budget 2025’s proposal to amend the Income Tax Act to allow the CRA to automatically file returns on behalf of eligible individuals who fail to review and confirm the return prepared by the agency.

Cost considerations also matter. Moving the preparation of tax returns from taxpayers to the CRA may redistribute costs between the private and public sectors but does not necessarily reduce overall costs. Budget 2025 estimates that the CRA’s new tax-preparation service for low-income individuals will carry an annual administration cost of about $18 million once it is fully implemented – likely a lower bound given frequent overruns – serving 5.5 million invited individuals.

If 3 to 11 percent of invitees take up the offer – consistent with existing SimpleFile take-up rates (Table 1) – the service would process roughly 165,000 to 605,000 returns, implying an administrative cost of about $30 to $110 per return. This estimate is within the range of the cost of administering PAYE in the United Kingdom, estimated at £24 (about $44) per taxpayer in 2023-24 (see Box 1).

Accounting for the broader economic costs associated with raising additional tax revenue,1212 The marginal cost of public funds (MCF) measures the social cost of raising an additional dollar of tax revenue, reflecting the dollar lost to the private sector and economic distortions created by taxation. See Dahlby and Ferede (2022) for recent federal personal and corporate tax estimations. The MCF for the top rate of federal personal income tax is $2.87, and the MCF for the corporate income tax is $2.02. the present-value total cost to society would be at least double the amount, roughly $60 to $220 per return filed through the CRA’s tax-preparation service. This figure would be at the lower end of the average private cost of preparing a return for the population eligible for the CRA service.1313 Roughly estimated based on two observations. First, most certified tax software allows individuals with modest incomes to file a basic return for free using NETFILE. Second, about 55 percent of CRA-filed returns would have been prepared by paid tax preparers, at an average cost of roughly $100. CRA’s Individual Statistics by Tax Filing Method (2022) show that 59 percent of individuals with simple returns, income below $25,000, and whose main income source was not self-employment, investment, or multiple sources filed using EFILE, most of which (but not all) are submitted by paid tax preparers.

Another factor to consider is the current federal budgetary focus on reducing spending on government operations, mainly by shrinking the size of the federal public service. The proposed automatic tax preparation service is targeted at a subset of existing filers with a history of very low income and basic returns. Clearly, the targeting of simple non-taxable filers considerably reduces the cost of implementation. But in this deficit-reduction context, scaling the initiative beyond the current targeted initiative to include taxable returns risks being much more expensive, operationally difficult, and politically fragile.

Policy Discussion

The policy challenge, which is to provide benefits to individuals who do not participate in the tax system, affects a relatively small share of Canadians. Including late filers, about 96.4 percent of expected filers participate, leaving 1.2 million individuals in 2023 who are unlikely to ever file a return for that year. Considering that not all potential filers are eligible for cash benefits (e.g., deceased and higher-income individuals, recent immigrants, and some temporary residents), the number of non-filers eligible for cash benefits is lower.

Targeting a subset of the population – those with income below the basic personal amount and for whom the CRA believes it has all of the income information – could help identify non-filers, reduce costs, and concentrate the energy where the chances of success are the greatest. However, the participants in the “automatic federal benefits” initiative will be known filers who have had prior interactions with the CRA.

The CRA does not seem to anticipate that the automatic benefit initiatives will drive a large number of new filers. Budget 2025 anticipates that the initiative will increase cash benefits by $103 million in 2029/30. Given the average cost of the GST Tax Credit, the Canada Child Benefit, and the Canada Workers Benefit, this corresponds to only about 44,000 new recipients by 2029/30.1414 Rough calculation using average 2023 payments for the GST Tax Credit and CCB for those earning less than $20,000, and average 2022 payments for the CWB, grown with inflation to the year 2029.

Clearly, inciting vulnerable people to participate in the tax system is different than delivering benefits and financial assistance to them. The automatic federal benefits initiative may be helpful, but it is trying to achieve two goals at once: first, making it easier and cheaper for targeted individuals to file their taxes, and second, paying benefits to hard-to-reach non-filers.

Digitalization has already cut the cost of filing by more than half since 1985 (Vaillancourt 2024). The cost of complying with the personal income tax, however, increases with tax complexity (Vaillancourt and Li 2024). AI-driven tools may greatly reduce the cost of excessive complexity. But the root of the problem remains the underlying complexity. In the long term, the most effective way for governments to implement greater tax-filing automation is through a concerted effort by federal and provincial governments to simplify the underlying tax system, at least for the majority of taxpayers who rely mainly on employment and pension income (Laurin and Dahir 2022; Fortin 2023; Genest et al. 2024).

For benefit delivery, strategies specifically targeting hard-to-reach individuals may be more effective. One option is to decouple benefit eligibility from tax filing and assign benefit administration to a separate body, as Laurin and Dahir (2022) suggest.

This approach aligns with the UK experience. Initially, poverty-reduction tax credits were administered through employers and the PAYE system. However, the lack of current information about individuals’ circumstances led to errors in determining eligibility, as well as over- and under-payments. The UK ultimately consolidated programs into the Universal Credit, administered separately and requiring a dedicated application process (APPTG 2017).

Separating benefit delivery from tax filing could help reach more vulnerable individuals who do not file tax returns. Some may be more willing to provide information or consent to data sharing if benefits are not administered by the tax authority. The low take-up of SimpleFile suggests that the CRA may not be well positioned to reach these populations.

One option is to establish a government body specifically responsible for administering income-tested benefits and coordinating entitlements across programs (Laurin and Dahir 2022). Such a function could be housed within ESDC, as suggested by Robson and Schwartz (2021). ESDC already administers a range of core federal income-support programs, including Old Age Security, Canada Pension Plan, and Employment Insurance. It has also launched the Benefits Delivery Modernization programme, a multi-year, multi-billion-dollar effort to significantly upgrade its ageing IT systems and modernize the way ESDC serves Canadians.

Such a body could coordinate with provincial governments, which administer social assistance, and use information from other sources to determine benefit eligibility. A dedicated benefits body could also support more frequent third-party income reporting, which would improve the responsiveness of benefit programs to changes in individuals’ circumstances (Petit et al. 2021).

Alternatively, a benefit delivery function could also remain within the CRA but operate with greater independence. An illustrative example within the CRA is the Charities Directorate, which operates under the Agency’s umbrella but with a functionally distinct mandate, client relationship, and service orientation that differ from its core compliance and audit functions. However, the CRA’s tax compliance-oriented mandate may limit its effectiveness in engaging hard-to-reach populations, particularly those who distrust the Agency.

Granted, decoupling benefits from tax filing could introduce new challenges, including risks of increased non-filing, fraud, privacy issues, and potential resistance from provinces or existing beneficiaries. Even so, improving benefit delivery outside the tax-filing system warrants serious consideration (Laurin and Dahir 2022).

Conclusion

The “automatic federal benefits” commitment blends two distinct objectives: reducing compliance costs for existing low-income filers and extending benefits to hard-to-reach non-filers. The evidence presented throughout this paper – including persistently modest uptake of SimpleFile, behavioural barriers to filing, the finding that users of CRA automation tools largely would have filed anyway, and the role of tax simplicity in enabling effective automation – suggests that a single policy instrument is unlikely to achieve both goals efficiently.

Automatic tax filing can help simplify compliance for some Canadians with very simple tax situations, particularly those whose income is fully reported to the tax authority. However, the overall complexity of the Canadian tax system, its reliance on taxpayer-reported income, personal circumstances governing eligibility for deductions and credits, and the addition of a provincial dimension to tax and benefit policies, limit the scope for fuller cost-effective automatic tax filing solutions.

Moreover, tax automation alone is unlikely to reach hard-to-engage individuals. More meaningful progress in benefit delivery would likely require a broader strategy, including delinking benefit eligibility from tax filing and possibly establishing a clear administrative separation between tax collection and the delivery of income-tested benefits.

REFERENCES

All-Party Parliamentary Taxation Group (APPTG). 2014. Tax simplification in the United Kingdom. London: All-Party Parliamentary Taxation Group.

______________. 2017. Report on the Administration of Pay As You Earn (PAYE). London: All-Party Parliamentary Taxation Group.

Canada Revenue Agency (CRA). 2022. “File my return – Qualitative Research.” Final Report: Quorus Consulting Group Inc.

______________. 2024. Statistical report on the participation of the hard-to-reach populations in the tax and benefit systems. 2024 Edition (2020 tax year).

Canada. 2020. Taxpayer Rights in the Digital Age: The Benefits and Risks of Digitalization for Vulnerable Populations in the Canadian Income Tax Context. Ottawa: Office of the Taxpayers’ Ombudsman. May.

______. 2024. “Defining and measuring the gig economy using survey data.” Statistics Canada, Catalogue no. 75-004-M2024001.

______. 2025. Annual Report 2024–2025: Clearing the Path. Ottawa: Office of the Taxpayers’ Ombudsman. June.

______. 2026. “Question No. Q-720 (House of Commons, 45th Parliament, 1st Session). Asked by Gérard Deltell, December 9, 2025. Answered January 26, 2026.” Ottawa: Parliament of Canada. January.

Dahlby, B., and E. Ferede. 2022. “What Are the Economic Costs of Raising Revenue by the Canadian Federal Government?” Vancouver: Fraser Institute.

Fochmann, M., F. Hechtner, T. Kolle, and M. Overesch. 2021. “Combating Overreporting of Deductions in Tax Returns: Pre-filling and Restricting the Deductibility of Expenditures.” Journal of Business Economics 91 (1): 935–64.

Fortin, C. 2023. “Analyse des systèmes de production automatisés de l’impôt sur la scène internationale : Étude des cas du Royaume-Uni et de la Finlande ainsi que de leur compatibilité pour le Canada et le Québec.” Université de Sherbrooke: Chaire de recherche en fiscalité et en finances publiques.

Forum on Tax Administration Taxpayer Services Subgroup (FTATSS). 2006. “Using Third Party Information Reports to Assist Taxpayers Meet Their Return Filing Obligations – Country Experiences with the Use of Pre-populated Personal Tax Returns.” Paris: Organisation for Economic Co-operation and Development. March.

Genest-Grégoire, A., J. Robson, S. Schwartz, and J. Dadjo. 2024. “What Proportion of Tax Returns Could the Canada Revenue Agency Complete?” Canadian Public Policy 50 (3): 292–310.

Hawara, Cathy. 2024. “Exploring the Impact of Emerging Technologies on Tax Administrations: A Compliance Perspective.” Perspectives on Tax Law and Policy 5 (2): June.

HM Revenue & Customs (HMRC). 2015. “P800 End of Year Tax Calculation Notice: Evaluation of P800 End of Year Tax Calculation Communication amongst PAYE Customers.” Research Report. October.

Kleven, H., M. Knudsen, C. Kreiner, S. Pedersen, and E. Saez. 2010. “Unwilling or Unable to Cheat? Evidence from a Randomized Tax Audit Experiment in Denmark.” NBER Working Paper 15769. Cambridge, MA: National Bureau of Economic Research. February.

Laurin, A., and N. Dahir. 2022. Automatic Tax Filing: A Challenging Idea for Canada. Commentary 616. Toronto: C.D. Howe Institute. https://cdhowe.org/publication/automatic-tax-filing-challenging-idea-canada/.

Messacar, D. 2017. “Big Tax Data and Economic Analysis: Effects of Personal Income Tax Reassessments and Delayed Tax Filing.” Canadian Public Policy 43 (3): 261–283.

National Audit Office (NAO). 2025. “The Administrative Cost of the Tax System.” London: National Audit Office. February 10.

Office of the Auditor General of Canada (OAG). 2025. “Report 1—Canada Revenue Agency Contact Centres.” In 2025 Reports of the Auditor General of Canada to the Parliament of Canada. Ottawa: Office of the Auditor General of Canada.

Parliamentary Budget Officer (PBO). 2024. “Expansion of SimpleFile by Phone and the Implementation of an automatic tax filing system.” June 13.

Petit, G., M.L. Tedds, D. Green, and R.J. Kesselman. 2021. “Policy Forum: Re-Envisaging the Canada Revenue Agency – From Tax collector to Benefit Delivery Agent.” Canadian Tax Journal 69 (1): 99–114.

Revenu Québec. 2025. Rapport annuel de gestion 2024-2025. Québec: Revenu Québec.

Robson, J., and S. Schwartz. 2020. “Who Doesn’t File a Tax Return? A Portrait of Non-Filers.” Canadian Public Policy 46 (3): 323–39.

______________. 2021. “Policy Forum: Should the Canada Revenue Agency also Be a Social Benefits Agency?” Canadian Tax Journal 69 (1): 87–98.

Stapleton, J. 2018. “A Fortune Left on the Table: Why Should Low-Income Adults Have to Pass Up Government Benefits?” West Neighbourhood House. June.

Vaillancourt, F. 2024. “Tax Complexity and Individual Tax Compliance Costs of the Personal Income Tax in Canada, 1985–2023: A Synthesis.” CIRANO Working Paper 2024s-13. Montréal: CIRANO.

Vaillancourt, F., and N. Li. 2024. “Personal Income Tax Compliance for Canadians: How and at What Cost?” Vancouver: Fraser Institute.

Young, Conrad. 2024. “Tax and Technology: Opportunities and Challenges.” Perspectives on Tax Law and Policy 5 (2): June.