Edited remarks delivered to the Toronto Association for Business and Economics (TABE) webinar, “Living on the Edge: Federal Budget Post-Mortem,” on November 13, 2025.

In isolation, the words and numbers in the federal budget presented on November 4, 2025, show a government getting a grip on the excesses that doubled its debt over the past decade. But the budget’s projections through to the 2029/30 fiscal year provide fresh evidence that the government’s past fiscal forecasts were wildly off the mark. The federal government has issued four sets of fall projections since most COVID-related restrictions ended in 2022: three fall economic statements (FESs) in 2022, 2023 and 2024, and the latest budget. Each blew past previous projections for spending, deficit, the debt-to-GDP ratio and total liabilities. With that context, and especially against a background of economic stagnation, the budget’s projections and the government’s assurances about a change in fiscal direction are not credible.

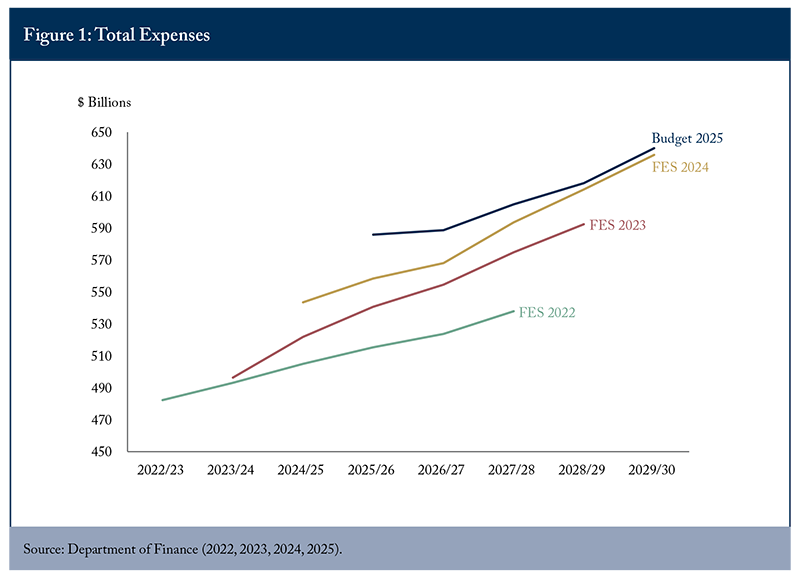

Relentlessly Higher Expenses

Spending – the government’s total expenses as shown in the public accounts – is core to any fiscal projection. The government must cover its expenses – all of them, including the debt charges and losses on its pension obligations that it omits from program spending in many presentations (Robson and Dahir 2025) – through taxes or additional debt. Notwithstanding the budget’s words about restraint, comparing total expenses projected in the past three fall statements and the budget (Figure 1) reveals two key facts. One is that the budget projects higher expenses in every year than the 2024 FES did. The other is that higher spending throughout the projection period is nothing new.

The recurring overshoots add up. The 2022 FES said expenses in the current fiscal year, 2025/26, would be $515 billion. Just four years later, the November budget said expenses would be $586 billion – more than $70 billion higher. Do we have any reason to think that a new set of projections a year from now, accompanied by repeated references to a weak economy, will not show spending another $15 to $20 billion higher yet? We do not.

Chronically Overshooting Deficits

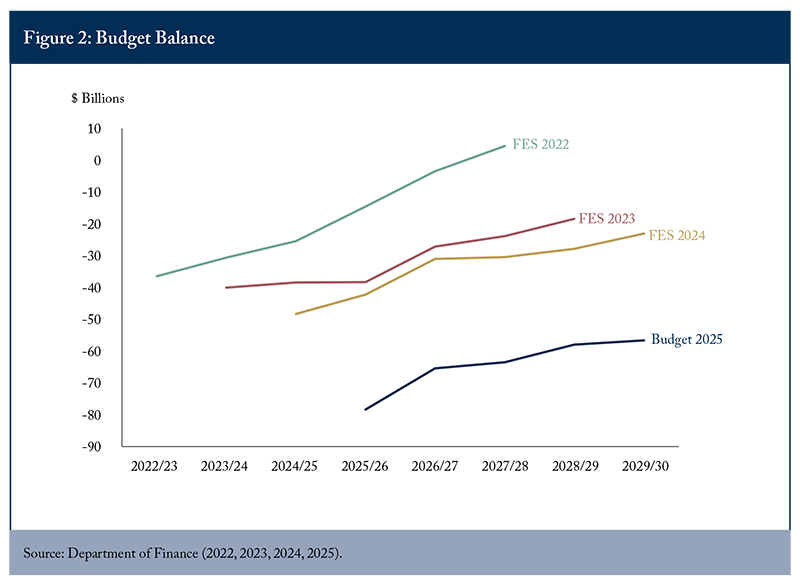

What about the deficit – the amount by which the government’s expenses exceed its revenues, adding to its debt and reducing its capacity to deliver future services without imposing higher taxes? The November budget shows bad news in the near term, and an improving trend thereafter. Compare its budget-balance projections with those in the past three fall statements (Figure 2), however, and optimism about later improvement evaporates.

Every set of projections has shown shrinking future deficits. But every set of projections has also shown overshoots of previous projections. In the fall of 2022, the government put the deficit in the current fiscal year, 2025/26, at $15 billion. The November budget put it at $78 billion. Should we expect the bottom line to constrain the government any more in the future than in the past? We should not.

Consistently Heavier Debt Burdens

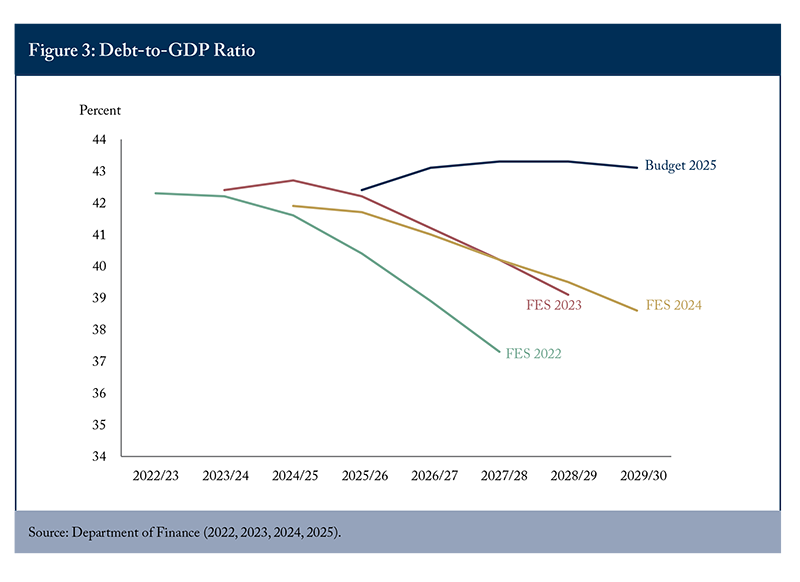

Many observers of government finances consider the budget balance a less compelling target than the ratio of the government’s accumulated deficit, the most widely cited measure of its debt, to gross domestic product (GDP). The debt-to-GDP ratio is a well-known measure of fiscal sustainability: the higher the ratio, the more of our national income the government must take to service the debt. Over the past few years, the government has talked repeatedly about reducing it. The recent budget forecasted slower GDP growth in the near term, which – combined with much larger deficits – means the projections show a higher debt ratio in the 2027/28 and 2028/29 fiscal years before a decline in 2029/30.

Comparing the budget’s projection with those in the previous three fall statements (Figure 3) eliminates any comfort from the later forecast decline. The 2022 fall statement said the debt ratio in 2025/26 would be 40.4 percent. The budget raises it to 42.4 percent. Successive projections have shown this key measure of fiscal sustainability to be worse than its predecessors. Can we trust the government to pursue it more resolutely in the future? We cannot.

Ominously Ballooning Liabilities

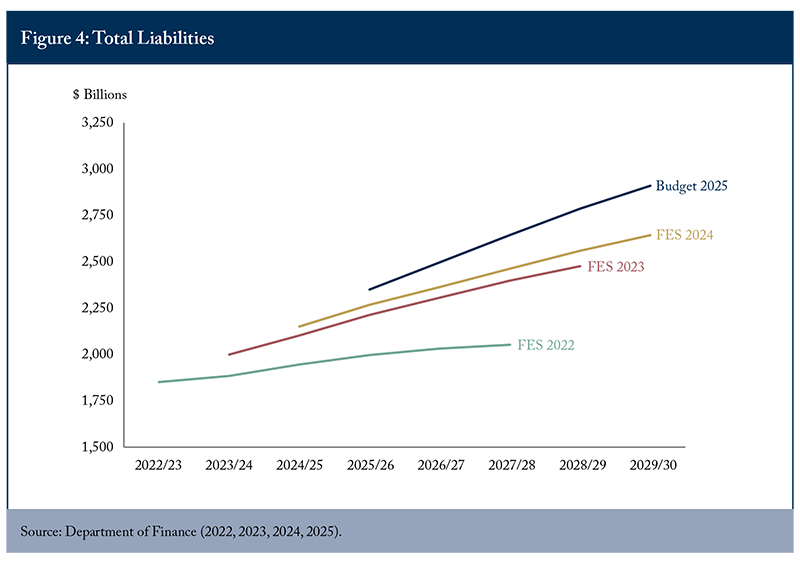

A less noted measure of the federal government’s fiscal hyperextension is its total liabilities. The accumulated deficit that is the normal focus of attention is the difference between the government’s liabilities and its assets. Historically, federal assets were not an exciting story: the government’s holdings of property and other nonfinancial assets were relatively small, and its financial assets – its loans, investments and advances to Crown corporations and other entities – tended not to vary much. More recently, and especially since COVID, the federal government has been lending big-time.

The government does not show loans as expenses, but every dollar it lends, like every dollar it spends, adds to its borrowing. And since the recipients of federal credit are borrowing from the government rather than on the market, we can reasonably worry that the returns on this lending will be below-market in the future, as they have been in the recent past.1Comparing annual returns on investment to beginning- and end-of-year financial assets in the Fiscal Reference Tables (https://www.canada.ca/en/department-finance/services/publications/fiscal-reference-tables/2025.html) shows that the rate of return on the government’s financial assets has averaged 1.49 percent over the past three fiscal years. The average interest rate on its gross debt, calculated the same way, was 2.24 percent.

The total liabilities projected in the fall of 2022 showed relatively low growth after the previous spike of COVID-related lending, anticipating just under $2 trillion by the end of the current fiscal year (Figure 4). Budget 2024, however, raised that estimate to $2.4 trillion by the end of this year – about double the increase in debt required to finance the deficit. The budget’s projections show equally fast growth ahead, with total liabilities approaching $3 trillion four years later. These astonishing numbers have so far attracted attention mainly from credit rating agencies (Fitch 2025). But uneconomic loans are transfer payments in disguise. One more time, we have to ask if future projections will show even more alarming changes in a key measure of fiscal risk. If recent experience is a guide, they will.

Fiscal Fantasies Will Not Fix Canada’s Problems

In context, the November 4th budget’s words and numbers heralding a change from recent fiscal excesses look far less reassuring than they do in isolation. Four years ago, the federal government showed much less spending and borrowing, a markedly lower debt-to-GDP ratio, and far less growth in total liabilities than the November budget prefigured. The government’s new projections are uniformly worse than those it presented just last fall, and preposterously worse than it showed in the fall of 2022.

The government will have excuses. Indeed, the optimistic economic projections built into the later years of the budget make disappointment likely – especially since the federal government’s high expenses and excessive borrowing are squeezing the private investment needed to make the economy grow (Robson and Bafale 2024). But credible fiscal policy requires managing setbacks, not succumbing to them. As things stand, the likelihood is that future projections will show further deterioration in these key measures of fiscal soundness. The federal government's fiscal projections in the fall of 2022, 2023 and 2024 were fantasies. Canadians need proof that they should take the projections in its November budget seriously.

I thank Nicholas Dahir for help with data in the fiscal projections, and Don Drummond, Alex Laurin and Daniel Schwanen for comments. Any mistakes and conclusions are my responsibility.

References

Department of Finance. 2022. Fall Economic Statement, 2022. Ottawa. November.

___________________. 2023. Fall Economic Statement, 2023. Ottawa. November.

___________________. 2024. Fall Economic Statement, 2024. Ottawa. December.

___________________. 2025. Canada Strong: Budget 2025. Ottawa. November.

Fitch Ratings. 2025. “Persistent Fiscal Expansion Underscores Canada Rating Pressures.” November 6th. https://www.fitchratings.com/research/sovereigns/persistent-fiscal-expansion-underscores-canada-rating-pressures-06-11-2025

Robson, William B.P., and Mawakina Bafale. 2024. Underequipped: How Weak Capital Investment Hurts Canadian Prosperity and What to Do about It. Commentary 666. Toronto: C.D. Howe Institute.

Robson, William B.P., and Nicholas Dahir. 2025. Making the Grade: The Fiscal Accountability Report Card for Canada’s Senior Governments, 2025. Commentary 695. Toronto: C.D. Howe Institute.