Surveys consistently show that most homebuyers in the Greater Toronto and Hamilton Area, including first-time and immigrant households, prefer ground-related housing, particularly single-detached homes and more affordable substitutes such as semi-detached homes, townhouses, and stacked townhouses. Yet the types of housing being built in the region have become increasingly misaligned with these preferences.

Surveys consistently show that most homebuyers in the Greater Toronto and Hamilton Area, including first-time and immigrant households, prefer ground-related housing, particularly single-detached homes and more affordable substitutes such as semi-detached homes, townhouses, and stacked townhouses. Yet the types of housing being built in the region have become increasingly misaligned with these preferences.- Since the mid-2000s, land-use planning policies have largely favoured higher-density apartment development in built-up areas over development on greenfield lands. This approach has limited the supply of preferred ground-related housing types and contributed to housing affordability challenges.

- Better aligning land-use planning with market preferences would improve housing affordability and market efficiency. This E-Brief concludes that greenfield land development is an essential component of any strategy to expand the supply of ground-related housing and improve affordability in the region.

Surveys consistently show that most homebuyers in the Greater Toronto and Hamilton Area, including first-time and immigrant households, prefer ground-related housing, particularly single-detached homes and more affordable substitutes such as semi-detached homes, townhouses, and stacked townhouses. Yet the types of housing being built in the region have become increasingly misaligned with these preferences.

Surveys consistently show that most homebuyers in the Greater Toronto and Hamilton Area, including first-time and immigrant households, prefer ground-related housing, particularly single-detached homes and more affordable substitutes such as semi-detached homes, townhouses, and stacked townhouses. Yet the types of housing being built in the region have become increasingly misaligned with these preferences.Introduction

Housing policy in the Greater Toronto and Hamilton Area (GTHA)11 The GTHA encompasses Toronto, York Region, Peel Region, Halton Region, Durham Region, and Hamilton. has become increasingly disconnected from the housing preferences of its residents. A majority of homebuyers, including first-time and immigrant households, prefer ground-related housing. That means single-detached homes or more affordable, reasonably close substitutes, such as semi-detached homes, townhouses, and stacked townhouses. Yet, recent land-use policies have favoured denser apartment developments in built-up areas rather than greenfield development that could provide more of the preferred ground-related housing stock.

This disparity limits the supply of preferred housing stock, drives up single-detached house prices, and negatively impacts overall affordability in urban areas. A larger supply and greater competition, supported by land-use planning that better aligns with market preferences, would improve affordability and facilitate filtering.

Further, this mismatch also has consequences. The supply of existing houses available for sale is reduced as traditional move-up buyers remain in their current homes rather than moving into new houses on greenfield sites. Homebuyers move farther from employment hubs in search of more affordable housing. Renters, who traditionally serve as a source of first-time buyers, remain in rental accommodation due to diminished affordability, thereby reducing turnover in the existing rental stock. These impacts exacerbate wealth inequality, as fewer households can access housing assets that appreciate over time.

This E-Brief analyzes homebuyer preferences using survey data, assesses supply trends, and examines land-use planning policies and their effects on specific housing types. It provides policy recommendations to better align land-use planning approaches with market preferences, thereby improving overall affordability and market efficiency.

Homebuyers Prefer Ground-Related Housing

Many GTHA homebuyers strongly prefer housing at or near ground level that offers an exterior entrance, a garage, and a plot of green space. Surveys show a strong preference for single-detached homes or more affordable, reasonably close substitutes, such as semi-detached homes, townhouses, or stacked townhouses.

A comprehensive, regular database of homebuyers in the GTHA and their housing-type preferences (whether owner-occupants or rental investors) does not exist. However, three survey datasets of actual or likely buyers (sometimes referred to as intending buyers) make it possible to construct a profile of buyer preferences by unit type. The three datasets are:

- Canada Mortgage and Housing Corporation’s (CMHC) annual Mortgage Consumer Survey – first-time and repeat home purchasers in Ontario obtaining a mortgage from 2017 to 2024;

- Toronto Regional Real Estate Board’s (TRREB) annual survey of Greater Toronto Area (GTA) households intending to purchase a home over the next 12 months from 2015 to 2024; and,

- Sagen Canada’s survey of types of housing units bought by first-time buyers in the GTA and the rest of Ontario in 2021 and 2023.

These buyers are largely owner-occupants rather than investors. The datasets vary in geographic coverage and buyer segment, but their consistent findings on unit-type preferences lend support to the thesis that buyers prefer single-detached houses. These are examined below.

Ontario Mortgage Buyers Prefer Single-Detached Homes

Each January, CMHC surveys a sample of mortgage consumers who are the primary decision-makers in their households and who have undertaken a mortgage transaction within the previous 18 months (the Mortgage Consumer Survey).22 A mortgage transaction is defined as the obtaining, renewing, or refinancing of a mortgage. CMHC provided the author with data on households buying a home, including a breakdown of first-time and repeat buyers, for Canada and Ontario from 2017 to 2025. The survey includes households that obtained a mortgage to purchase a first or subsequent home.33 Excluding homes purchased without mortgage financing does not materially affect the overall mix of homes purchased (with and without a mortgage). Almost all first-time buyers (95 percent) take out a mortgage. Most mortgage-free purchasers are older repeat buyers (21-22 percent). These buyers include affluent households moving up to more expensive single-detached houses and seniors moving down to less expensive homes such as condominiums (see Teranet 2023).

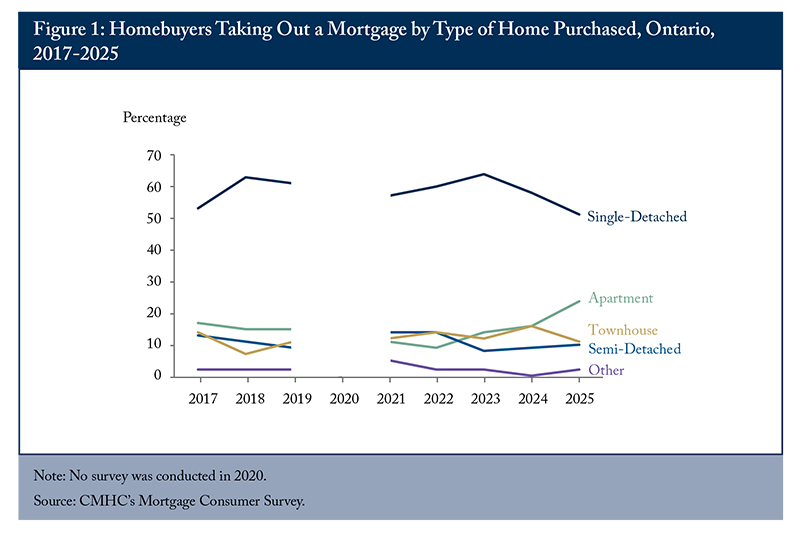

Among surveyed buyers in Ontario, single-detached houses are the most common housing type, accounting for 52-65 percent of purchases during 2017-2025 (Figure 1). Other ground-related housing (semi-detached and townhouses) accounted for 18-28 percent of purchases. Condominium apartments accounted for less than a quarter of purchases.

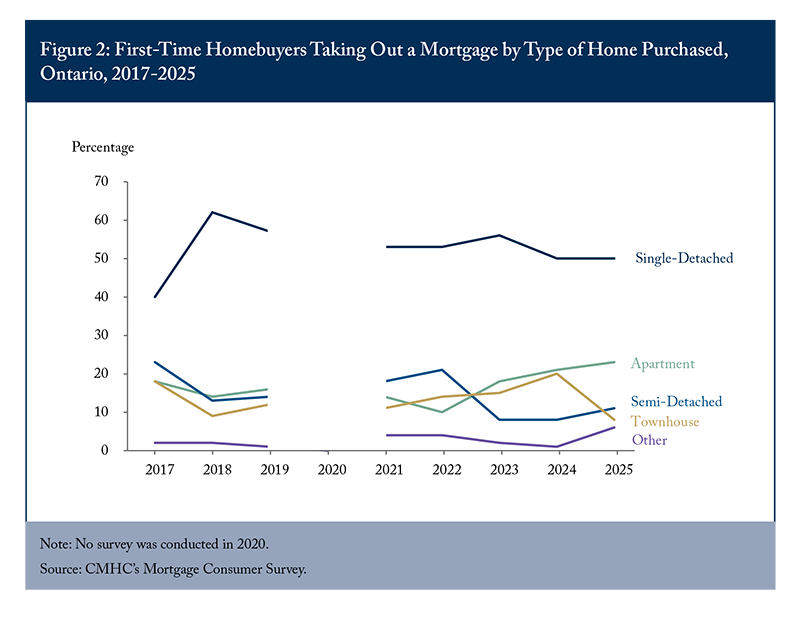

Survey results for Ontario first-time buyers categorized by unit type are presented in Figure 2. Single-detached houses also dominated first-time buyers’ purchases, accounting for 40-62 percent of all purchases during 2017-2025. The proportion of first-time buyers purchasing a condominium apartment ranged from 10-23 percent, with the remainder comprising semi-detached homes and townhouses.

Likely GTA Buyers Prefer Single-Detached Homes

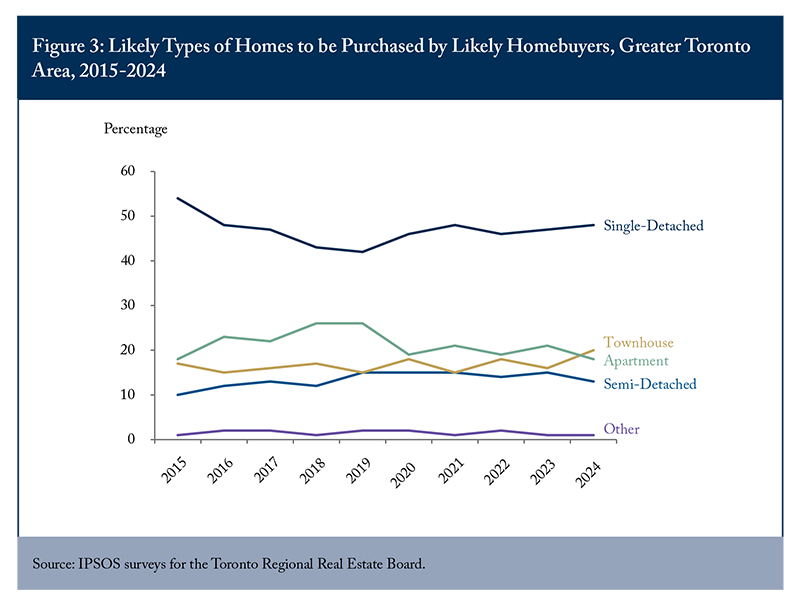

For the past 10 years, the Toronto Regional Real Estate Board has retained Ipsos to survey likely buyers, both repeat and first-time, in the GTA and categorize them by the type of housing they intend to purchase. Likely buyers are respondents who indicate that they are very likely or somewhat likely to purchase a home to live in within the next year (Figure 3).

Over the past 10 years, condominium apartments have accounted for 18-26 percent of likely purchases, with an overall average of 21 percent. Single-detached houses dominated ground-related housing types, accounting for 42-54 percent of all likely purchases (with an overall average of 47 percent).

Condominium apartments were more likely to be purchased in Toronto than in the GTA, at 25 and 16 percent respectively, but they still lagged single-detached houses by a wide margin.

GTA First-Time Buyers Buy Ground-Related Homes, but Few Single-Detached Homes

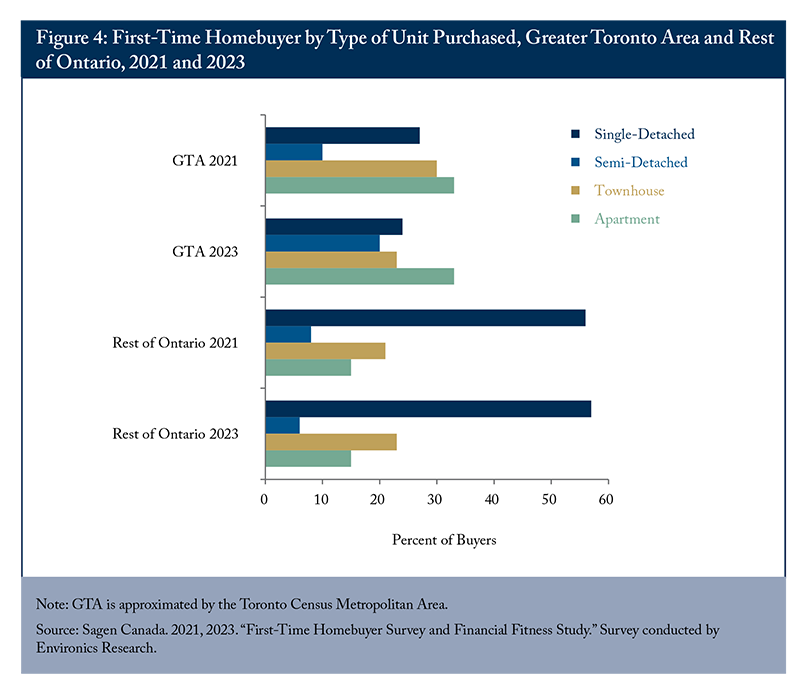

Sagen Canada retained Environics to survey first-time buyers and intending first-time buyers across Canada in early 2021 and 2023. Figure 4 presents the housing types purchased by first-time buyers in the GTA and the rest of Ontario.

In both years, two-thirds of the GTA’s first-time buyers purchased a ground-related home, with the remaining third purchasing a condominium apartment. More than 20 percent bought a single-detached house.

The housing preferences of first-time buyers were markedly different in the rest of the province. Nearly 60 percent of this group purchased a single-detached house, with townhouses the next most common option. Only 15 percent of these buyers preferred an apartment.

Planning Restrictions on Greenfield Development

A prominent theme in urban planning in Ontario and many other jurisdictions over the past two decades has been that new housing should be constructed primarily in the built-up areas of large urban centres (called intensification or redevelopment), rather than on fringe, vacant lands (typically farmland, often referred to as greenfield areas). There is little to no indication that planners adequately considered households’ housing type preferences.

The 2006 Growth Plan for the Greater Golden Horseshoe (GGH)44 Located in southern Ontario, the GGH wraps around the western end of Lake Ontario. This urban region encompasses the GTA and major surrounding cities, including Hamilton, St. Catharines, Niagara Falls, Kitchener, Waterloo, Guelph, Barrie, and Peterborough. in southern Ontario (hereafter referred to as the Growth Plan) is a prime example of how planning policies and initiatives have overlooked consumer preferences.55 Ontario Ministry of Public Infrastructure Renewal. 2006. Growth Plan for the Greater Golden Horseshoe. June. The province merged the Growth Plan and the Provincial Policy Statement into a single, streamlined Provincial Planning Statement. Effective October 20, 2024. The plan sought to create transit-supportive, “complete communities” with a diverse mix of jobs and housing, along with local retail and services, to reduce dependence on automobiles and increase transit use, walking, and cycling. To the extent that greenfield areas were developed, they were to be compact and transit-supportive. While single-detached and semi-detached houses on small lots could be included under the umbrella of compact urban form, the focus was primarily on townhouses, walk-up apartments, or apartments above retail space (Ontario Ministry of Public Infrastructure Renewal 2006).

This meant that over time residents increasingly would not be living in single- or semi-detached houses. Instead, they would live close to transit and could walk or bike to retail, medical, educational, and even employment opportunities without needing a car. The influence of the Growth Plan on the inventory of residential land by type is evident in the supply of approved and proposed housing units in the development approval process. According to a survey conducted by the Regional Planning Commissioners of Ontario, this inventory in the GTHA totalled 911,748 units at the end of 2022, split between apartments at 86 percent and ground-related homes at 14 percent (Regional Planning Commissioners of Ontario 2023).

Why were single-detached houses in low-density, car-dependent suburbs sidelined? In 2015, an Advisory Panel headed by David Crombie, reviewing the Growth Plan, deemed this pattern of suburban development to be sprawl. The panel considered sprawl harmful because of its negative effects on farmland, congestion, air and water quality, human health, and the loss of green space, habitats, and biodiversity, all exacerbated by climate change.66 The Advisory Panel for the Coordinated Review of the Growth Plan, Greenbelt Plan, Oak Ridges Moraine Conservation Plan, and Niagara Escarpment Plan (2015), 9. The Task Force did acknowledge that this development pattern “…provided many residents with affordable, single-detached houses.” However, no overall benefit-cost analysis was conducted. In particular, the review gave no consideration to the impact of this development pattern on housing affordability.

The household surveys reviewed show a strong preference for single-detached houses. When constrained supply drives up prices, households cannot buy homes in their preferred locations, reducing economic well-being. Suboptimal choices include accepting smaller, denser accommodation or moving farther away to find more affordable houses.

The outflow of many residents to other parts of the province is a byproduct of the lack of affordable ground-related housing in the GTA. Between 2019 and 2024, the GTA experienced a net outflow of residents to other parts of the province averaging 62,109 persons per year (Clayton and Petramala 2026). According to a 2022 Statistics Canada survey, the most frequent reasons given for moving from one municipality to another in Ontario were to become a homeowner (22 percent) and to find bigger or better housing (21 percent) (Song et al. 2026).77 Statistics Canada provided the author with Ontario-specific data.

To encourage densification of built-up areas and compact suburban development, the 2006 Growth Plan required municipalities to direct at least 40 percent of all residential development to built-up areas and to adopt a minimum density target of 50 residents per hectare in greenfield areas.88 The 2006 Growth Plan provided no guidance on housing types, except that complete communities should offer a full range of housing, including affordable housing in their existing housing stock and newly built housing. The 2015 Advisory Panel recommended higher minimum intensification and density targets, which the provincial government subsequently implemented. As minimum density targets rise, fewer single-detached houses can be accommodated on greenfield lands.

Whether development occurs in built-up areas or on greenfield lands largely determines the types of housing that can be built. Apartments dominate new housing construction in built-up areas, while ground-related homes predominate in greenfield land development (Clayton 2022).

In the 14 years before the June 2018 general election, provincial governments paid scant attention to the types of housing preferred by residents of the GGH. Rather than considering consumer preferences, policymakers relied on minimum intensification and greenfield density targets to shape the housing mix (Ontario Ministry of Municipal Affairs 2018). A focus on the total number of units, their size, and the number of bedrooms obscures the equally important dimension of housing type and consumer preference.

Since the election of a new provincial government in 2018, policy has shifted toward requiring municipalities to accommodate a full range of housing, including single-detached houses. The Growth Plan was recently merged into a new Provincial Planning Statement, and compulsory minimum intensification and density targets were eliminated. Ontario also simplified the process for designating greenfield development lands. However, policy still emphasizes total new housing production, as reflected in the province’s municipal housing targets, which are based solely on the total number of units.99 The More Homes Built Faster Act 2022 empowers the province to establish municipal housing targets. Housing type and consumer preferences remain largely overlooked.

From Houses to Apartments

New housing production and sales data are not limited to homes purchased by owner-occupants. Housing starts include all new residential structures, whether intended for ownership or rental, and whether market or social housing. Sales of new homes marketed for ownership also include sales to investors, who have until recently been prevalent in the condominium apartment market. Both measures illustrate a significant shift toward apartments and away from single-detached houses in the GTHA’s housing market since the early 2000s.

Apartments Dominate Housing Starts

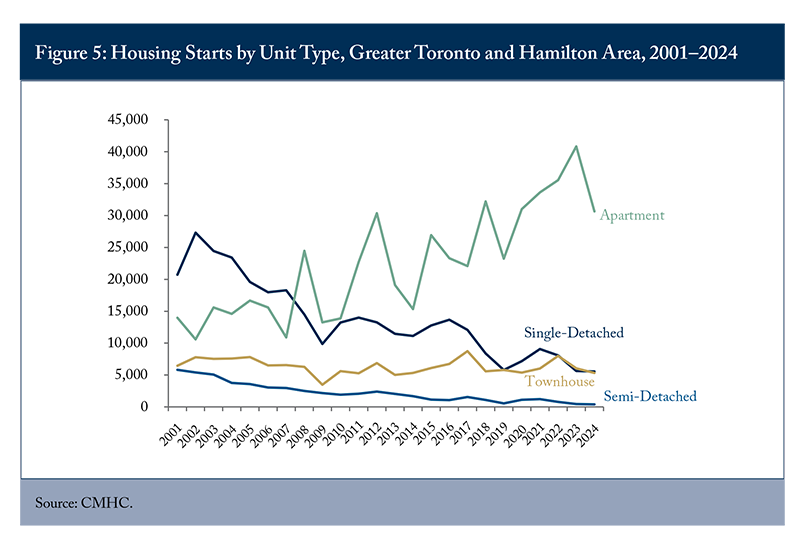

The trend toward apartments and away from single- and semi-detached houses is evident in housing starts by dwelling type in the GTHA since 2001 (Figure 5):1011 The primary data source of new housing supply through the construction of new residential structures is CMHC’s Starts and Completions Survey. The survey excludes net housing added through the conversion of non-residential buildings to residential use or through the creation of units in existing residential structures (such as secondary suites). Unit types include single- and semi-detached houses, townhouses (row), and apartments. All types and tenures of new self-contained dwelling units are surveyed.

- Single-detached houses accounted for 44 percent of total starts in 2001, followed by apartments (30 percent), townhouses (14 percent), and semi-detached homes (12 percent).

- By 2024, apartments dominated, accounting for 73 percent of total starts, while single-detached house starts had dropped to just 13 percent.

- Semi-detached house starts also declined sharply over the period, while townhouse starts remained more or less flat.

The decline in semi-detached starts in part reflects competition from small-lot single-detached houses.1112 Historically, semi-detached houses had a significant cost advantage over single-detached houses because they were sited on lots about half the size. But over time, the lots for single-detached houses have shrunk in size, reducing this cost advantage. However, the planning policy’s de-emphasis of greenfield development contributed to stagnation in townhouse starts, a decline in semi-detached starts, and a shift away from single-detached houses.

New Home Sales Mirror the Shift to Apartments

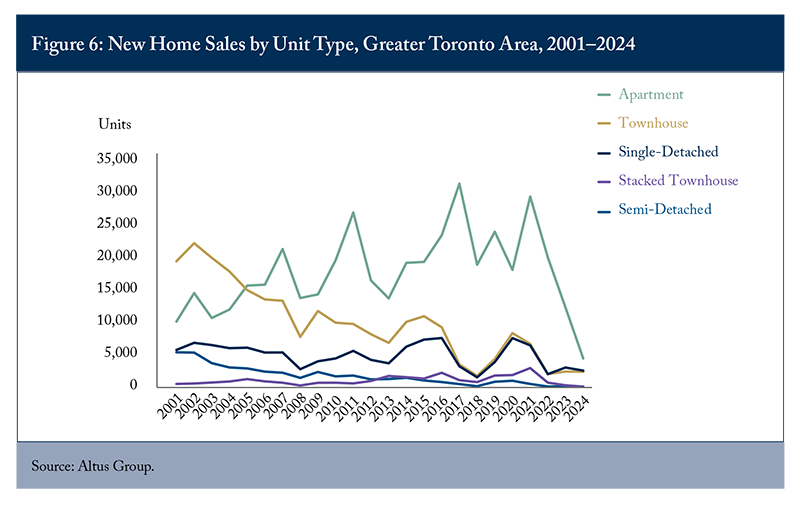

A marked shift from sales of single- and semi-detached homes to apartment sales is also evident in the GTA’s “for sale” new home market (see Figure 6).1213 A second source of new housing supply data is new home sales in the GTA, tabulated by Altus Group for the Building Industry and Land Development Association. It surveys all residential projects being marketed for sale with more than 10 units, regardless of whether the buyers intend to occupy or rent out the units. It separates stacked townhouses from other apartments and includes conversions in existing office and other types of non-residential buildings. Townhouse and stacked townhouse sales were essentially flat. Restrictions on greenfield development also constrained stacked townhouse development and other ground-related housing types.1314 Special tabulations of CMHC data show that while missing middle starts are prominent in the regions around Toronto, they are negligible in Toronto, suggesting the economics of development are more benign on greenfield lands. See: Clayton and Nomani (2023).

Proposed Alternatives to Ground-Related Housing on Greenfield Lands

As previously noted, planning policy has often overlooked housing types when determining what new housing should be accommodated in built-up areas. More recently, there has been growing recognition that high-rise apartment buildings with predominantly small units are not a substitute for single-detached houses for many homebuyers. The planning literature offers several alternatives to suburban greenfield development. These include:

- transit-oriented development in built-up areas;

- downsizing by seniors living in existing single-detached houses;

- permitting missing middle housing options in existing lower-density neighbourhoods;1415 The permitted missing housing forms are typically less encompassing than the standard definition, which includes a spectrum of housing from semi-detached to apartment structures of up to four storeys. Typically, up to four or six units are permitted on existing single-detached lots, depending upon lot size. and,

- focusing on larger sizes and more bedrooms for new apartments in built-up areas.

These alternatives largely substitute apartments in existing built-up areas for ground-related homes on greenfield lands.1516 As noted earlier, most housing built on greenfield sites are ground-related homes with some apartments, while most new housing in built-up areas are apartments with some townhouses. Depending on the option, these apartments can include both high-rise and missing-middle formats. The problem is that many households do not regard these apartments as viable alternatives to single-detached houses. They do little to improve ground-related housing affordability.

Missing Middle Housing Is Only a Partial Substitute

There is a continent-wide movement to introduce more housing options into conventional single-detached neighbourhoods, providing alternatives to suburban single-detached houses and mid- to high-rise apartments. Known as missing middle housing, these options encompass housing types between single-detached houses and apartment buildings with five or more storeys. They include semi-detached houses, duplexes, triplexes, quadruplexes, townhouses, stacked townhouses, and low-rise apartments (garden apartments).

Ontario’s More Homes Built Faster Act (2023) allows up to three units “as of right” per single-detached lot in most existing low-density neighbourhoods (Barnett, Barz and Rintoul 2022). In 2023, Toronto amended its official plan and zoning by-law to permit duplexes, triplexes, and fourplexes city-wide (so-called gentle density). In June 2025, the council approved as-of-right zoning for up to sixplexes in some parts of the city. One rationale for missing middle housing is that households unable to afford an entire single-detached house may be able to access a smaller unit in the same neighbourhood (City of Toronto 2021).

Building more housing in built-up areas should be encouraged, but in a way that provides alternatives that compete with suburban ground-related homes by offering ground-level entrances, private outdoor space, and often parking. Unfortunately, much of the planning discussion focuses on expanding the supply of missing middle housing rather than on the housing preferences of households (Burda and Chapple 2024).

Senior Turnover Is Not Enough

There is a general recognition that as many babyboomers living in single-detached houses encounter serious health issues or die, their homes become available for younger households to purchase. Many seniors living in single-detached houses are, in fact, considered “overhoused.” This has been defined by experts as one or two people living in homes with three or more bedrooms (City of Toronto 2020).

A 2021 City of Toronto study estimated that the turnover of homes owned by seniors could accommodate an additional 207,240 people within the existing housing stock. The study suggested that the city could expedite turnover by increasing the supply of affordable housing, requiring a minimum share of two-bedroom-or-larger units in new developments, and permitting secondary suites and laneway housing (City of Toronto 2021).

However, the supply of single-detached houses occupied by seniors that are put on the market in any year will likely be small. A 2023 CMHC study found that movement by seniors into condominiums is modest and that few senior homeowners are interested in moving into rental housing. The study noted downsizing is somewhat more common in the Toronto and Vancouver metropolitan areas (CMHC 2023).

The bottom line is that while all existing single-detached houses occupied by seniors will eventually become available on the market – dictated by choice, health, or death – their numbers are insufficient to eliminate the need for new single-detached and other ground-related housing, particularly in high-growth regions like the GTHA. Much of this new ground-related housing will need to be built on greenfield sites.

Larger Apartments Are Not a Substitute

Various planners and housing advocates support requiring developers to make new apartment projects more family-friendly by incorporating larger units that might encourage families to remain in built-up areas rather than move to suburban single-detached houses. In practice, however, developers in Toronto have built relatively few larger units. In 2020, Toronto adopted guidelines encouraging new apartment developments to include at least 25 percent of large units (15 percent two-bedroom units and 10 percent three-bedroom units). However, research and market evidence suggest that many families seeking additional space prefer a single-detached house or a reasonably close substitute, rather than a larger unit in a high-rise apartment building (Sherman 2024).

Policy Directions for Accommodating Buyer Preferences for Single-Detached Houses

It is time to recognize homebuyers’ housing preferences when planning the types and locations of new housing across the GTHA. While developing large tracts of greenfield land for single-detached houses is a thing of the past, the main alternative offered to date, high-rise apartments, is not regarded as an acceptable substitute by most buyers. Consequently, many households bid up the prices on existing houses or move farther afield in search of more affordable single-detached houses, resulting in longer commutes.

The solution is to increase the supply and lower the cost of suitable substitutes for subdivisions composed exclusively of single-detached houses. Greenfield developments consisting of townhouses, stacked townhouses, and other low-rise apartments, such as garden apartments, along with single-detached houses on small lots (as narrow as 28 front feet), have gained market acceptance and improved affordability by increasing densities. This approach has been adopted in several municipalities, including Oakville (North Oakville), Waterloo Region, and Ottawa (Kanata).

Why Homebuyers Prefer Single-Detached Homes

The desire for a single-detached house on a decent-sized lot is deeply ingrained in the Canadian psyche. A Statistics Canada analysis found that owners and renters living in low-density housing, such as single-detached houses, report higher levels of housing satisfaction than those living in more compact dwellings (Pârvulescu, Chen and Kavaslar 2024).

For many potential purchasers in Ontario, preferred features of single-detached houses include a backyard, a finished basement, and a non-urban location. In a 2025 Canada-wide survey commissioned by Wahi, 81 percent of respondents stated that if they were in the market to own or rent a new home, a backyard would be important or very important (76 percent among seekers of ground-related homes). A finished basement was considered important by 42 percent of respondents, indicating a preference for larger spaces. A quieter environment was mentioned by 36 percent of respondents (Sherman 2025). Only a third of Ontario’s potential buyers surveyed in 2024 preferred an urban location. The majority preferred a suburban (42 percent) or rural (26 percent) location (Sherman 2024).

Realistic Substitutes for Single-Detached Homes

Many observers believe the way forward is to encourage a plentiful supply of missing middle housing in built-up areas while freezing greenfield development. Increasing densities on existing single-detached lots, whether by adding units to an existing house (e.g., secondary suites), replacing an existing house with up to six new units (e.g., triplexes to sixplexes), or adding a free-standing dwelling to the property (e.g., a garden home), should be encouraged. This approach offers many advantages and is often referred to as gentle densification, in contrast to building mid- and high-rise apartments (high densification).

Proponents of gentle densification often argue that the new housing units created are suitable for a range of households, including prospective buyers of single-detached houses. Some go so far as to say that adding missing middle housing in built-up areas will erase the need for suburban ground-related housing in greenfield areas.1617 The City of Hamilton is a conspicuous example of this perception. Council voted for nil greenfield expansion of its urban boundary on the premise that 100 percent of housing needs can be satisfied by redevelopment and infilling. But more in-depth analysis is needed to understand why households prefer single-detached houses and the trade-offs they are willing to make between denser housing in built-up areas and lower-density housing forms on greenfield lands. Affordability, living space, private outdoor space, and parking availability are among the considerations.

Maintaining an Adequate Supply of Serviced Land for Ground-Related Housing

A 2023 Toronto Metropolitan University study found a severe shortage of shovel-ready land for ground-related housing in the GGH (Clayton and Amborski 2023). The region had only a 1.9-year supply of ground-related land, compared with the four-year minimum required for each housing type under the now Provincial Planning Statement, with annual monitoring. This scarcity has kept the price of zoned and serviced land elevated.

The report recommended the province consider: (1) placing more emphasis on increasing the supply of affordable housing options that are closer substitutes to ground-related housing (i.e., stacked townhouses, garden apartments, and fourplexes) than high-rise apartments, and establishing supply targets for these housing types; and (2) making the maintenance of an ample supply of shovel-ready land by housing type a provincial priority by enforcing or incentivizing compliance with policy 2.1.4b of the 2024 Provincial Planning Statement.1718 Previously, policy 1.4.1b of the Provincial Policy Statement.

Reducing Housing Production Costs

Most observers would accept the premise that developers and builders must charge prices or rents that cover all costs and provide an expected risk-adjusted competitive return; otherwise, they will not continue to build new housing. Currently, the cost of approved and serviced sites is exceptionally high because of land scarcity, government-imposed costs, and limited competition in the land development industry.

A recent study estimated that government taxes and fees in Ontario accounted for 35.6 percent of the average price of new housing (all types) in September 2024, up from 31 percent in 2021 (Canadian Centre for Economic Analysis 2024). Reducing these costs is necessary if housing prices are to become more affordable.

Conclusions

Since the mid-2000s, land-use planning policies in the Greater Golden Horseshoe have largely disregarded the housing preferences of residents. While demand for ground-related homes, especially single-detached houses, has remained strong, planning policies – for environmental and infrastructure reasons – have instead promoted mid- and high-rise apartments. This mismatch has increased pressure on the prices of ground-related housing and pushed households farther from jobs and amenities in search of more affordable homes.

The recent focus on intensifying existing lower-density neighbourhoods by allowing more units on a single-detached lot is a step in the right direction because it will provide housing types that could serve as substitutes for some homebuyers. However, these policies are insufficient to accommodate affordable housing preferences. The housing provided will often not be competitive with housing on greenfield land. Units will typically be smaller, lack parking, offer less privacy, and be more costly per square foot.

There is also a need for ground-level housing forms and close substitutes, such as duplexes and stacked townhouses, on greenfield lands. In this context, urban areas must grow outward through greenfield development as well as upward through intensification.

The author extends gratitude to David Amborski, Colin Busby, Ben Dachis, Nicholas Dahir, Tasnim Fariha, Brian Johnston, Nik Luka, Stu Niebergall, Steve Pomeroy, Peter Weltman, Rosalie Wyonch, and several anonymous referees for valuable comments and suggestions. The author retains responsibility for any errors and the views expressed.

References

Advisory Panel on the Coordinated Review of the Growth Plan for the Greater Golden Horseshoe, Greenbelt Plan, Oak Ridges Moraine Conservation Plan, and Niagara Escarpment Plan. 2015. Planning for Health, Prosperity and Growth in the Greater Golden Horseshoe: 2015–2041. Toronto: Queen’s Printer for Ontario. December.

Barnett, Chris, Evan Barz, and Andrew Rintoul. 2022. “Bill 23 – More Homes Built Faster Act, 2022… Passed Fast.” Osler. November 29.

Burda, Cherise. 2014. 2014 Home Location Preference Survey: Understanding Where GTA Residents Prefer to Live and Commute. Toronto: Pembina Institute.

Burda, Cherise, and Karen Chapple. 2024. “What Types of Housing Do We Actually Need?” More and Better Housing Canada. April.

Calthorpe, Peter. 1993. The Next American Metropolis: Ecology, Community and the American Dream. New York: Princeton Architectural Press.

Canada Mortgage and Housing Corporation (CMHC). 2023. “What Do We Know About Elderly People’s Behaviour on the Canadian Real Estate Market?” Housing Market Insight. November.

Canadian Centre for Economic Analysis. 2024. The Increasing Tax Burden on Ontario Homes: 2024. Report commissioned by the Residential Construction Council of Ontario (RESCON). November.

City of Toronto, City Planning Division. 2020. “Growing Up: Planning for Children in New Vertical Communities.” Toronto. May.

————. 2021a. “Right-Sizing Housing and Generational Turnover.” Bulletin. May.

Clayton, Frank. 2016. “Will GTA Homebuyers Really Give Up Ground-Related Homes for Apartments?” Centre for Urban Research and Land Development. August 15. 22–23.

————. 2022. “No to Urban Boundary Expansion: Halton Region Is Not Hamilton, but Still Challenges Provincial Directives for 30-Year Land Supply.” Centre for Urban Research and Land Development. July 22. 5–6.

Clayton, Frank, and David Amborski. 2023. “Expanding Housing Supply and Improving Housing Affordability in the GGH Are Pipedreams Without an Ample Inventory of Shovel-Ready Sites.” Centre for Urban Research and Land Development. May 25.

Clayton, Frank, and Diana Petramala. 2026. “Significant Net Resident Outflows from the City of Toronto and Peel Region to Elsewhere in Ontario Continue in 2025.” Centre for Urban Research and Land Development. March 10.

Clayton, Frank, and Maaha Nomani. 2023. “Missing Middle Housing Starts in the Greater Toronto and Hamilton Area, 2006–2022.” CUR Blog. Centre for Urban Research and Land Development. December 18.

Environics Research. 2024. Housing Preferences in the GTA: Summary Report. June.

Ontario Ministry of Municipal Affairs. 2018. Land Needs Assessment Methodology for the Greater Golden Horseshoe. Toronto: Queen’s Printer for Ontario.

Ontario Ministry of Municipal Infrastructure Renewal. 2006. Growth Plan for the Greater Golden Horseshoe. Toronto: Queen’s Printer for Ontario.

Ontario Ministry of Municipal Affairs and Housing. 2024. Provincial Planning Statement, 2024. Toronto: King’s Printer for Ontario.

Pârvulescu, Radu Andrei, Wanlin Chen, and Cesur Kavaslar. 2024. “New Housing Supply: Urban Sprawl and Densification.” Housing Statistics in Canada. Statistics Canada.

Regional Planning Commissioners of Ontario. 2023. “News Release and Media Package: Inventory of Ontario’s Unbuilt Housing Supply.” March 7.

Sherman, Josh. 2024. “Wahi Survey Reveals What Canadians Want Most in a Home.” Based on Wahi’s 2024 Great Canadian Dream Home Survey. September 12.

————. 2025. “The Top Features of a Home in 2025, According to Canadians.” Based on Wahi’s 2025 What Homeseekers Want survey. March 19.

Song, Gordon, Karl Chastko, Silvia Grueva, and Patrick Charbonneau. 2026. “Why Do People Move Within Canada? A Study on the Reasons for Internal Migration and Mobility Using the Canadian Housing Survey.” Demographic Documents. Statistics Canada. February 16.

Teranet. 2023. “The Impact of Interest Rate Increases on Ontario’s Housing Market.” Market Insights Report, Q1.