April 23, 2026 – The C.D. Howe Institute’s Monetary Policy Council (MPC) calls for the Bank of Canada to keep its target for the overnight rate, its benchmark policy interest rate, at 2.25 percent at its next announcement on April 29, maintain it at that level until October of this year, and raise it to 2.5 percent by April 2027.

The MPC is chaired by Jeremy Kronick, the Institute’s President and CEO, and includes the chief economists of the six largest Canadian banks, alongside six leading academic economists and financial market experts.

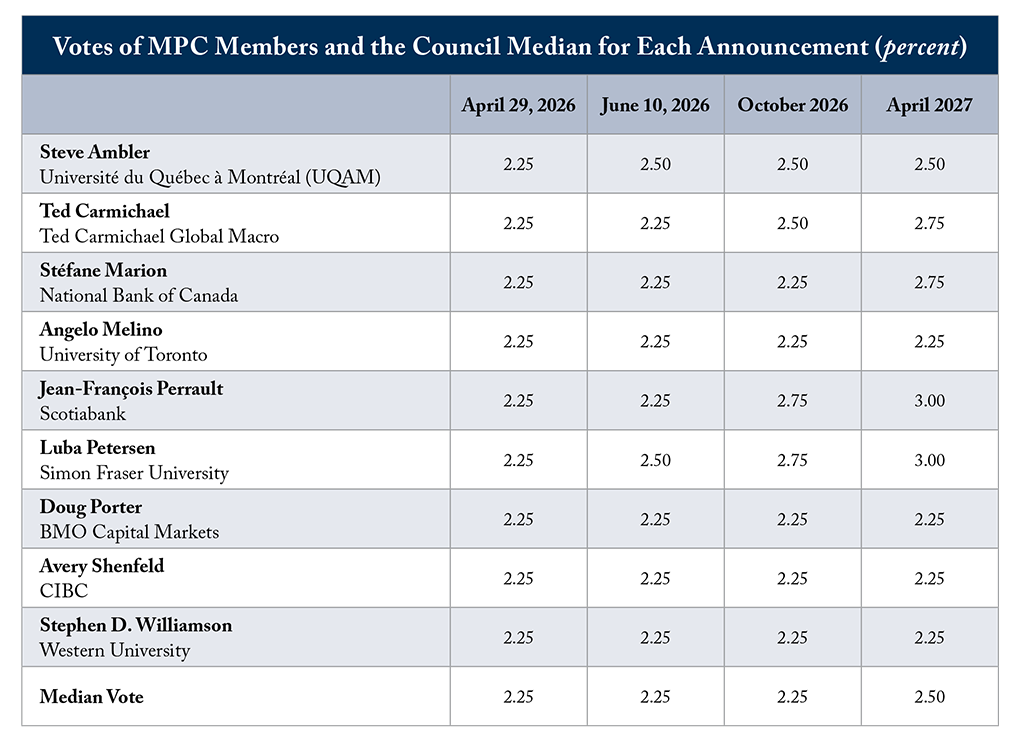

Acting as a shadow Bank of Canada Governing Council, the MPC provides an independent assessment of the monetary stance needed to achieve the Bank’s 2-percent inflation target. Its formal recommendation for each interest rate announcement is the median vote of members in attendance. Members vote on the upcoming announcement, the subsequent announcement, and the announcements six months and one year ahead.

All nine MPC members in attendance called for the Bank of Canada to hold the overnight rate target at 2.25 percent next week. At the Bank’s next announcement in June, seven of the nine members recommended holding at 2.25 percent, while two members voted for a hike to 2.5 percent. Six months ahead, five members voted to keep the overnight rate target at 2.25 percent, two members recommended the rate be set at 2.5 percent, while two others argued for a rate at 2.75 percent. By next April’s meeting, four members recommended 2.25 percent, one voted for 2.5 percent, two argued for a target of 2.75 percent, while two more thought the rate should rise to 3 percent (see table below).

Members highlighted uncertainty in the direction of the war in the Middle East and the upcoming review of CUSMA as two main drivers for holding the overnight rate target steady at this upcoming meeting and those in the near future. Members also noted that weakness in the economy, coupled with upward pressures on inflation, is creating a stagflationary-type scenario. Until there is more clarity, members saw this as justification for holding the overnight rate at its current level.

The group pointed to closures of the Strait of Hormuz as affecting more than just the price of oil. The impact is significant on a host of other commodities, which have increased in price, creating a broader-based negative supply shock on both global economic growth and growth here in Canada. Members also noted that ongoing closures are disrupting supply chains, meaning the economic impact of the war will likely last beyond the conflict itself. Canada had already been mired in a manufacturing slump long before the war began.

Members made the case that inflation expectations risk becoming de-anchored in the current environment. Both consumer and business inflation expectations are not back to pre-pandemic levels. The Business Outlook Survey highlighted an increase in inflation expectations and a willingness among businesses to increase prices and pass them on to consumers.

Offsetting the inflationary environment, members highlighted weakness in the economy across a number of fronts. Labour market data has been soft over the first few months of the year. Canada experienced an annual population decline in 2025 for the first time since Confederation. Housing markets are flat despite earlier rate cuts. Even with higher oil prices, members questioned whether this would lead to any tangible increase in investment at home as businesses await more certainty from trade negotiations and federal-provincial discussions. Members made the comparison with the post-COVID inflation surge, with less stimulative interest rates and government support today.

That said, members emphasized that next week’s spring fiscal update will be important for the future direction of monetary policy. More demand-side policies beyond the fuel tax cut might require the Bank to tighten monetary policy in an inflationary environment. If the fiscal actions to come are more investment-based, the Bank may be able to remain on the sidelines for now.

The views and opinions expressed by the participants are their own and do not necessarily reflect the views of the organizations with which they are affiliated, or those of the C.D. Howe Institute. Forecasters’ recommendations may differ from their predictions.

The MPC’s next vote will take place on June 4, 2026, prior to the Bank of Canada’s overnight rate announcement on June 10.

* * * * *

For more information, contact: Lauren Malyk, Manager, Communications, 416-873-6168, lmalyk@cdhowe.org.

Want more insights like this? Subscribe to our newsletter for the latest research and expert commentary.