by Colin Busby and Nicholas Dahir

- Canada’s NATO commitment to raise defence spending to 5 percent of GDP by 2035 will prompt a reshaping of federal finances. Defence spending will approach $150 billion by 2034/35, roughly triple current levels, and rival the annual amount of major transfers to provinces.

- Under the status quo, higher defence spending would significantly increase deficits and put both the deficit-to-GDP and debt-to-GDP ratios on upward trajectories.

- Weak productivity, slow economic growth, an ageing population, and high debt levels limit Canada’s ability to accommodate the NATO defence spending commitment without broader fiscal changes. Some combination of tax increases, spending cuts, or taking on more debt is required.

- A mixed approach that combines a modest GST increase with slower growth in non-defence spending offers a practical path to meeting NATO commitments while maintaining fiscal sustainability, alongside clearer budget reporting on defence spending to track progress toward the target.

Introduction

In response to Russia’s annexation of Crimea in 2014, NATO members gathered in Wales that September and committed to spend at least 2 percent of their annual national income, GDP, on defence by 2024. Canada and some other NATO countries failed to meet this pledge, arriving at the target only by early 2026.

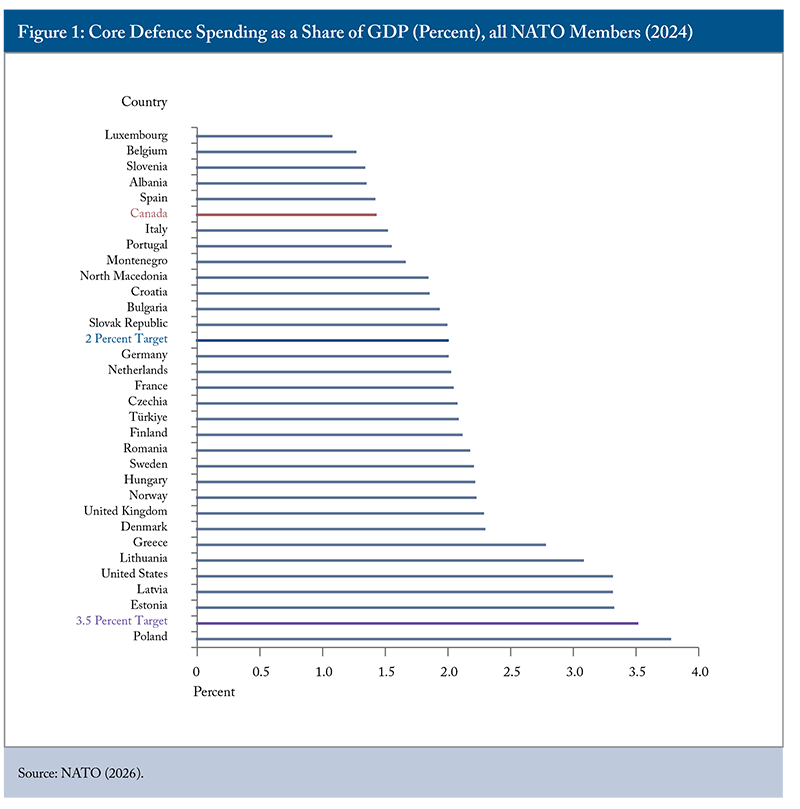

During this decade, NATO grew increasingly frustrated with members’ lack of compliance, notably Canada. In 2024, Canada was spending only some 1.5 percent of its GDP on defence (Figure 1), and people noticed. The NATO Secretary General publicly mentioned Canada’s lack of compliance, and the US Speaker of the House called Canada a “free rider,” essentially riding on the back of other countries to ensure its safety (Taylor 2024; Van Dyk 2024).

In June 2025, with concerns about Russia’s widening military aggression in Europe, Canada and other NATO members signed onto a new Defence Investment Pledge under which countries commit to spend 5 percent of GDP on defence by 2035 (NATO 2025). Only 3.5 percent of GDP need be devoted to “core defence”11 Core defence spending effectively extends the 2014 Wales Declaration, raising the 2-percent target to 3.5 percent, with the additional 1.5 percent covering categories of spending that NATO previously did not include. capabilities (20 percent of which would go to equipment and R&D) while the remaining 1.5 percent can be spent toward dual-use and defence-related infrastructure and other investments.

Recent shocks to the international order, pressure from NATO allies, and what defence minister David McGuinty described as “a world of growing threats” have made national security a top priority (Canada 2025d). Expanding Canada’s defence capabilities and meeting NATO commitments will require Canada to spend more on defence. A lot more.

This Commentary investigates the fiscal implications of meeting the NATO defence target by 2035 and outlines the challenges higher defence spending poses to federal finances. It also looks at the federal government’s options to meet the target while maintaining a sustainable fiscal regime.

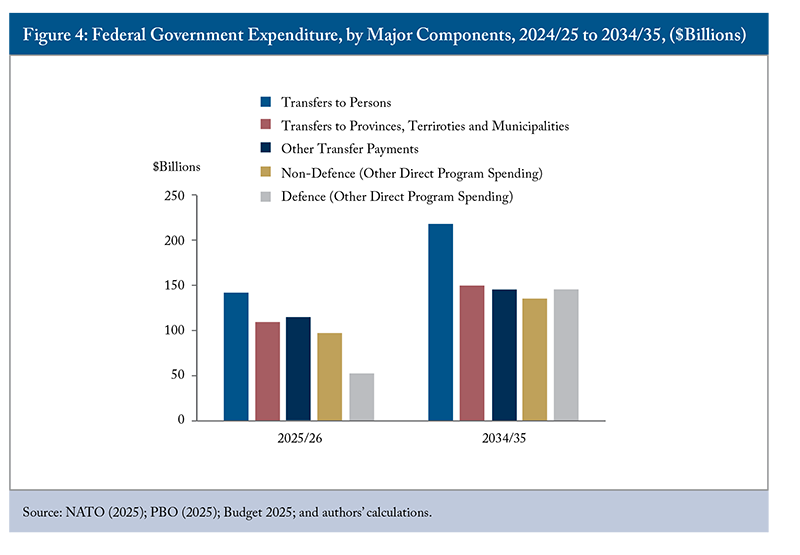

We anticipate that the federal government will spend more on defence by 2033/34 than on direct non-defence program spending (on a comparable accrual basis). By 2034/35, defence spending would rival what the federal government would spend on transfers to other levels of government. In that fiscal year, defence spending, on an accrual basis, would approach $150 billion, up from just over $50 billion in 2025/26. This tripling would be a sea change in the allocation of federal government resources.

Finally, we project that, without further fiscal restraint, the federal government will not be able to maintain Budget 2025’s planned downward trajectory for its deficit-to-GDP fiscal anchor ratio and will instead see substantial growth in deficits and debt.

Canadians, in other words, must make some hard fiscal choices about taxes, non-defence spending, and debt if we are to renew our national defence and security and meet our 2035 NATO commitment without sacrificing fiscal discipline.

Canada had made this commitment amid ongoing economic headwinds. An ageing population will put upward spending pressure on demographically sensitive programs, such as Old-Age Security (OAS) and the Guaranteed Income Supplement (GIS), as well as downward pressure on revenue (Robson and Mahboubi 2024). Meanwhile, challenges with traditional international trade partners and weak productivity also risk being a drag on revenues. Any tax increases must therefore minimize harm to economic growth. And rising federal debt and interest costs make borrowing less attractive, as it shifts more of today’s costs onto future generations. Some difficult decisions must be made.

We argue that a mixed financing approach is most pragmatic. It reduces the risks of relying on any single option. Curbing the growth of non-defence spending can be tempered with an increase in the GST rate to help finance defence commitments while limiting the issuance of debt and the burden on future generations. The federal government should present its incremental path to meeting its NATO spending pledge by embedding a line item for defence spending (on an accrual basis) in federal budgets and by establishing a House of Commons committee to oversee progress in strengthening military capabilities.22 This includes greater transparency around the 1.5-percent NATO benchmark for spending on defence-related infrastructure, including clear reporting on whether and how it has been achieved.

Canada’s Defence Commitment and the Federal Fiscal Picture

Catching Up to Peers: Where Do We Stand?

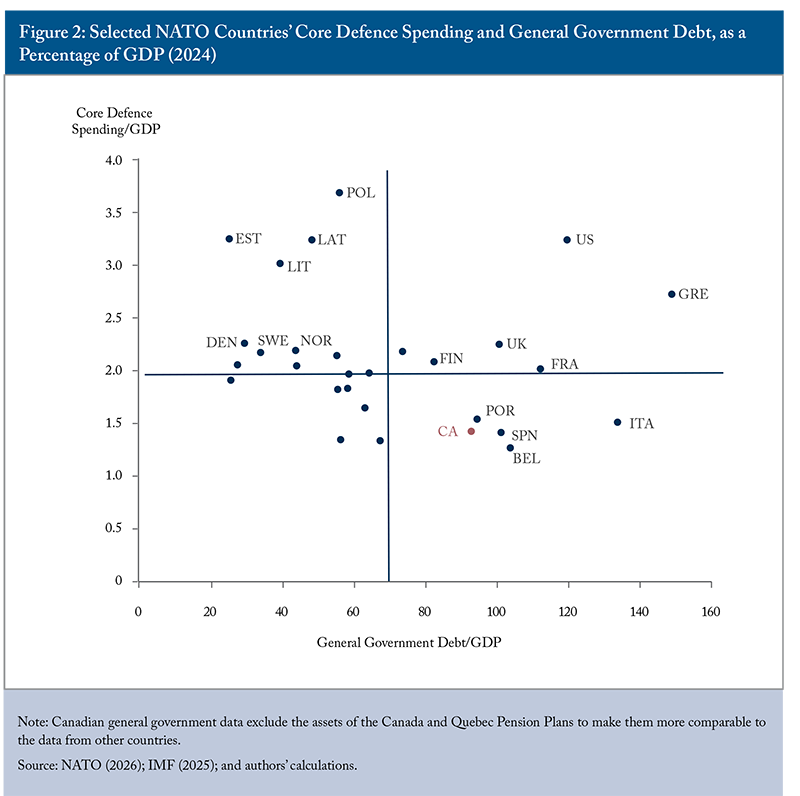

Canada has a lower debt-to-GDP ratio than many G7 countries, but it is running its largest deficit as a share of the economy outside a recession since the mid-90s.33 There were notably larger federal deficits as a percentage of the economy in the 1980s, a period when Canada was entering a fiscal crisis that demanded major reforms to federal finances. More concerning, Canada’s military readiness lags and its defence spending fell well short of the 2024 NATO average of 2.2 percent. This puts Canada near other laggards, notably Belgium and Spain. Another laggard, Slovenia, spends a similar share of GDP on defence but carries slightly less debt. Having to ramp up from this starting point will be daunting for Canada.

Figure 2 shows NATO countries’ 2024 core defence spending and debt as shares of GDP. The figure is split into quadrants, with a horizontal line at 2 percent – the 2024 NATO spending target for direct defence spending (now 3.5 percent for 2035) – and a vertical line at the average level of country indebtedness (excluding the top and bottom 5 percent of countries).

Countries in the upper-left part of the graph are those spending above previous NATO requirements on defence and also carry relatively less debt. Those in the upper right are also spending above the previous NATO target, but are in a less advantageous fiscal position and may find it difficult to reach the 2035 target. Countries in the lower-right portion of the graph are in the most precarious position: they need to make up a lot of ground to improve their defence capabilities, but have less fiscal room to do so. Canada falls into this group, making prudent management of its fiscal situation in pursuit of increased defence capabilities even more important.

Projections of Federal Finances: Fiscal Assumptions and Spending Required to Meet NATO 2035 Target

To better analyze the implications of Canada’s NATO commitment on federal finances, we make several assumptions regarding the spending pledge, as well as future revenues and expenses. We first outline the key elements of the pledge and our analytical focus. We then lay out how we use Budget 2025’s economic and fiscal projections and other data sources as the basis for our fiscal projections for revenues and non-defence spending over the next decade.

The Defence Spending Pledge

NATO’s 5-percent target has two parts: 3.5 percent of GDP for core defence and an additional 1.5 percent for systems and infrastructure that support military operations. The latter leaves room for interpretation. Canada and several other NATO countries are interpreting this to mean that investments in roads, ports, airports, and telecommunications networks, which can serve defence readiness, should qualify.

Indeed, Budget 2025 reinforces this approach by committing tens of billions of funds in infrastructure projects and in the renewal of existing projects. For this analysis, we assume that combined federal, provincial, and territorial spending will meet the 1.5-percent target.44 Chapter 4 of Budget 2025 makes that assumption. See https://budget.canada.ca/2025/report-rapport/chap4-en.html. For this reason, we focus on how Canada can meet the 3.5-percent core defence target.

NATO allies also agreed that at least 20 percent of core defence expenditure should be devoted to major new equipment, including associated research and development. This requirement was designed to ensure that enough military spending goes into modernizing equipment and to ensure a reliable industrial base. As NATO (2025) notes, “[w]here expenditures fail to meet the 20-percent guideline, there is an increasing risk of equipment becoming obsolete, growing capability and interoperability gaps among Allies, and a weakening of Europe’s defence industrial and technological base.” Our projections therefore assume core defence spending of 3.5 percent of GDP, with at least 20 percent allocated to equipment and R&D as the basis for our fiscal projections.55 For spending on equipment and R&D, we take what is projected by the PBO (2025) and adjust upwards in the last few years of our forecast to ensure that Canada meets the 20-percent sub target.

How We Construct Our Defence Spending Projection

We use publicly available data to build projections for the 3.5 percent of GDP on core defence spending, starting in 2026/27. We take GDP projections from Budget 2025. Because the budget’s forecast horizon ends in 2029, we extend it by applying the average nominal GDP growth rate for 2025–2029 (3.72 percent) to subsequent years. The NATO requirement is interpreted as applying by January 2035, making 2034/35 our target fiscal year.

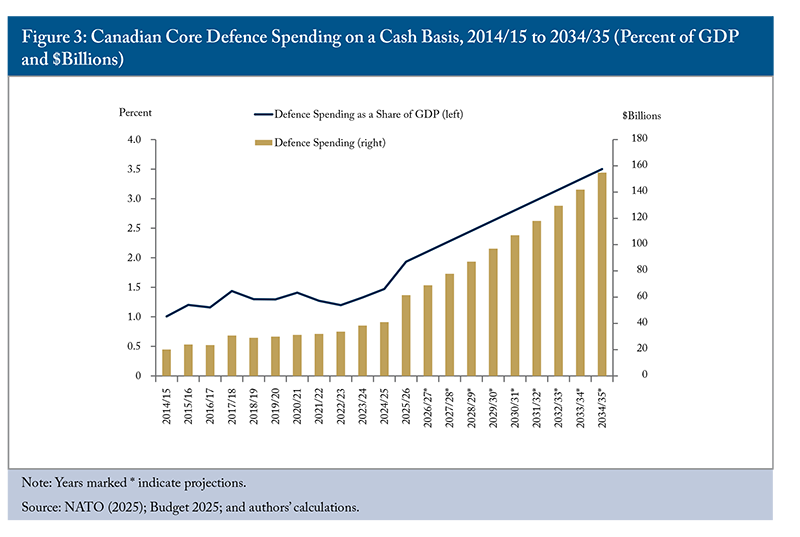

We assume Canada increases core defence spending as a share of GDP in equal annual increments from 2026/27 until it reaches 3.5 percent in 2034/35. Under this baseline, defence spending (cash-basis) rises from around $41 billion in 2024/25 to $96.9 billion by 2029/30, and to $154.8 billion by 2034/35 (see Figure 3).

Accrual Defence Spending

NATO measures defence spending on a cash basis, while Canada’s budgets and financial statements report it on an accrual basis. Converting between the two requires adjusting the treatment of capital purchases. Under cash accounting, governments record the full cost of capital purchases in the year the cash changes hands. Under accrual accounting, they spread costs over assets’ useful lives, recording only annual depreciation as an expense.

To convert cash-basis spending to an accrual basis, we: (1) identify the share of cash-basis defence spending allocated to new capital investment; (2) subtract these capital outlays from total spending; and (3) add back annual depreciation expenses, calculated using straight-line amortization – the Department of National Defence’s method (Canada 2025c) – over a 10-year period, assuming assets depreciate at 10 percent annually. This produces an accrual measure consistent with Canada’s budgeting and fiscal reporting framework.

After estimating the annual cash-basis spending needed to reach 3.5 percent of GDP, we convert it to accrual terms. We draw capital spending levels and projections from the Parliamentary Budget Officer (PBO). When PBO projections fall below 20 percent of total spending, we adjust them upward to meet NATO’s requirement that at least 20 percent of defence spending go to major equipment.

Using these assumptions, we project annual new capital outlays and associated amortization costs. We then calculate accrual defence spending by adding amortization expenses to operating spending (cash spending minus new capital outlays).

How We Build Our Fiscal Projection

To project federal finances for the coming decade, we rely primarily on Budget 2025 for economic growth and revenue assumptions. Because the budget forecast ends in 2029/30, we assume revenues grow in line with GDP from 2030/31 to 2034/35.

We also project major spending areas using the following assumptions:

- transfers to persons (e.g., OAS/GIS, Canada Pension Plan, Canada Child Benefit, etc.) grow at 5.3 percent annually, consistent with the budget’s average annual growth;

- transfers to provinces, territories, and municipalities (e.g., the Canada Health Transfers, Canada Social Transfer, Equalization, etc.) grow with GDP;

- debt financing charges remain at 4.96 percent annually, the same as the percentage of federal debt in 2029/30; and

- other direct program expenses (including transfer payments610 One main reason for its middle-of-the-pack ranking is that it can lend directly to the government. In reality, however, this is a weak concern. The Bank has not provided a formal direct advance to the government since 1935, the first and only year it happened (Chant 2022). The Bank does purchase government debt at auction in primary markets, making the distinction with a formal advance somewhat overstated. However, the vast majority of these purchases have been made to offset currency in circulation and to smooth financial markets. and other direct program spending) grows at the same rate as the GDP.

For other direct program spending, we separate defence from non-defence components. We start with 2024/25 defence spending (cash-basis) as reported to NATO, convert to an accrual basis, and subtract it from other direct program spending to derive a 2024/25 non-defence baseline. We then grow this non-defence spending in line with GDP over the projection period, adjusting it for spending cuts outlined in Budget 2025.77 Budget 2025 announced a comprehensive expenditure review that sees direct program expenses reduced by over $60 billion over the next five years. We reduce spending by $9.2 billion in 2026/27, $11.3 billion in 2027/28, $12.8 billion in 2028/29, $13.6 billion in 2029/30, and $12.5 billion on an ongoing basis.

Interpreting the Baseline Scenario

Measuring Fiscal Sustainability

Starting from Budget 2025 and assuming core defence spending would hit 3.5 percent of GDP by 2035, we look at federal finances under a status quo, baseline scenario. To assess fiscal sustainability, we focus on three key fiscal metrics: 1) the budget balance; 2) the deficit-to-GDP ratio, which indicates short-term fiscal standing under the federal government’s current fiscal anchor; and 3) the debt-to-GDP ratio, which signals long-term sustainability of public finances.

- The budget balance is the difference between government revenues and spending in a given year. A balanced budget means annual government revenues equal expenditures. Deficits indicate when annual spending exceeds revenues and requires the government to borrow.

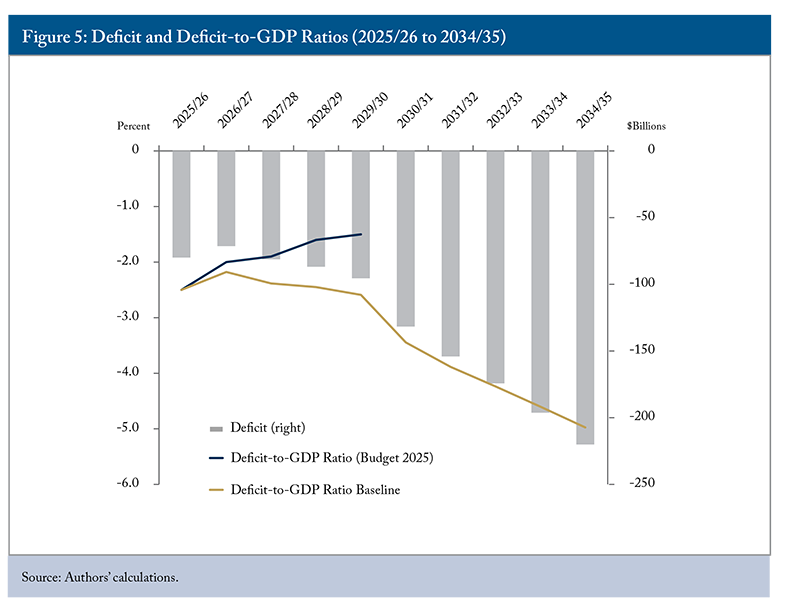

- The deficit-to-GDP ratio measures when annual government spending exceeds revenues as a share of GDP. A rising ratio signals an increasing reliance on borrowing compared to prior years. Budget 2025 notes that a declining deficit-to-GDP ratio is the government’s fiscal anchor of choice.

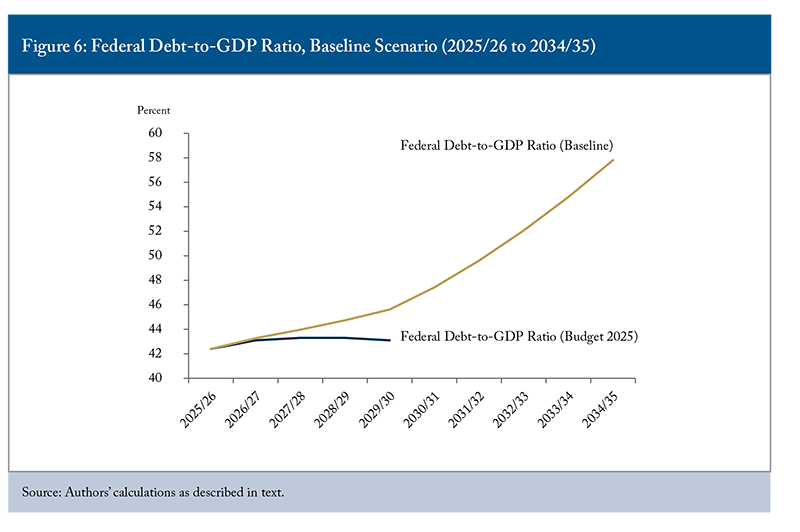

- The debt-to-GDP ratio expresses total public debt as a share of GDP. A high ratio indicates that public debt is large relative to the size of the economy, which limits fiscal flexibility. A growing debt-to-GDP ratio signals that debt is increasing faster than the economy. For most of the decade prior to Budget 2025, a declining debt-to-GDP ratio was the federal government’s preferred fiscal anchor.

Baseline Results: How Big is the Challenge?

Figure 4 compares accrual-based defence spending with major transfers to persons, major transfers to provinces, territories, and municipalities, other transfer payments, and other non-defence direct program spending. Under our baseline, defence spending surpasses non-defence program spending by 2033/34 and approaches transfers to other levels of government by 2034/35. It rises to nearly $150 billion, up from just over $50 billion in 2025/26 – a tripling over a decade. This shift would make defence one of the largest components of federal spending and would be a sea change not seen for generations.

Under our baseline scenario, we project deficits to get bigger, a lot bigger, along with deteriorating federal deficit-to-GDP and debt-to-GDP ratios. Over the next decade, our projected increase in defence spending results in a much higher deficit compared to the 2025 Budget’s forecasted trajectory. We estimate the deficit will exceed $95 billion by 2029/30, some $38 billion more than the budget predicts. As a result, the federal government will not be able to maintain its planned downward trajectory for its deficit-to-GDP fiscal anchor (Figure 5), and debt will grow substantially, further challenging Canada’s fiscal position (Figure 6).

Putting the Challenge into Focus

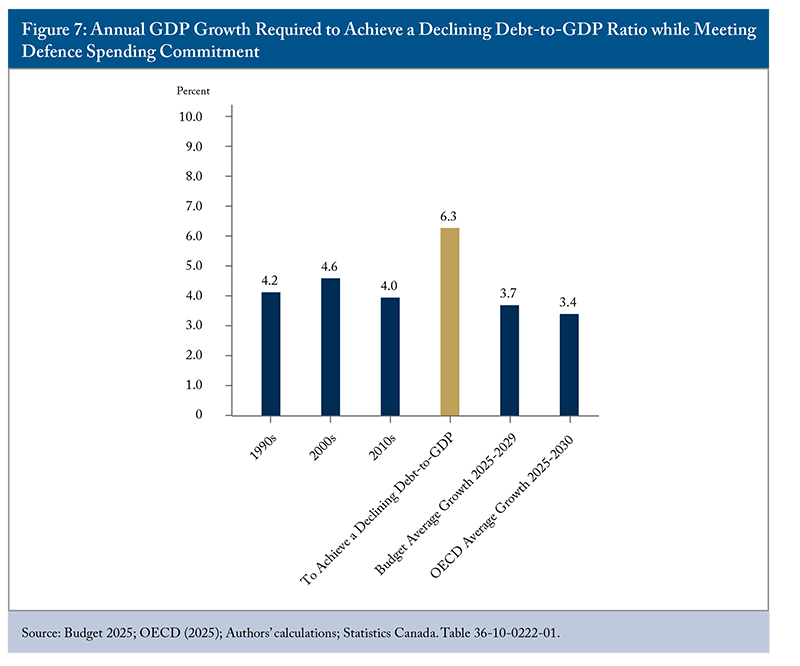

We frame the size of the challenge by estimating the economic growth required to achieve the federal government’s fiscal targets and key fiscal indicators in good health. This scenario assumes that the federal government relies on growth to pay for increased defence spending while meeting its fiscal targets.

Some argue that increased spending on defence will have broader economic benefits that outweigh the current costs (Perry and Stone 2021). The idea is that each dollar spent produces more than a dollar of economic activity. Recent research indeed finds positive effects, but their magnitude is a matter for debate (Ilzetzki 2025). Other meta-analyses demonstrate more ambiguity in the level of the GDP impact (Checherita-Westphal and Særkjær 2025). Defence spending may also support innovation and productivity (Surico and Antolin Diaz 2025; Schwanen and Wyonch 2018).

However, these effects face important limits in the current context, particularly constrained labour supply. Fiscal multipliers tend to be larger during recessions, when unused labour is available. As of winter 2026, Canada is not in a recession, and skilled labour remains scarce. This constraint is especially relevant with Canada planning a series of major infrastructure projects that will put pressure on labour markets.

This situation could change were Canada to face a more serious economic downturn, and we acknowledge that there may be larger productivity increases, along with increased forms of dual-use technology growth over the long run from more robust defence spending. But for now, we simply ask ourselves: what level of GDP growth would allow defence spending to effectively “pay for itself”?

To achieve a declining debt-to-GDP ratio, we find that nominal GDP would need to grow at 6.3 percent annually between 2026/27 and 2034/35 (Figure 7).88 Our target for a declining debt-to-GDP ratio is for it to be below 42 percent by 2034/35. Economic growth fluctuates with the business cycle: some years see stronger growth, while in recessionary episodes, growth is negative. So, sustained annual growth of 6.3 percent is highly unlikely. Moreover, it is highly unlikely that any multiplier effect, if it exists, would generate this much growth this quickly.99 Recall that when GDP increases, so does the actual required defence spending to meet the NATO target. Also, so do revenues and the growth of certain spending programs designed to stay the same size of the economy (transfers to provinces). Budget 2025 forecasts average annual growth to be 3.7 percent over the next five years, and the OECD’s outlook is less optimistic at an average annual rate of growth of 3.4 percent between 2025 and 2030.

Clearly, relying on economic growth alone is not an option. The economic growth required to achieve the NATO and fiscal targets suggests that the federal government must adjust revenue, spending, or issue much more debt.

How to Tackle the Challenge

Given the scale of the problem, what choices could the government make and what trade-offs would be involved? We explore these questions in the following sections.

Benefits and Costs of Different Financing Approaches

There are, of course, some valid arguments in favour of debt financing to help pay for the costs of defence spending and procurement. Borrowing takes a current expense and spreads the cost across generations. Provided that the benefits of these costs accrue to other generations and have value over time, debt allows future beneficiaries to share the cost, rather than placing the entire burden on today’s taxpayers.

Defence spending is, however, not the type of service where benefits accrue equally to future generations as they do to existing ones. True, some defence investments – naval vessels, planes, and other forms of heavy equipment – provide services over decades and can reasonably be debt-financed. Furthermore, to the extent that preparation for conflict today could prevent a future war, the indebtedness case is strengthened. However, during periods of insecurity, the generation that receives the services that protect them should arguably carry the bulk of the tax burden.

With political pressures and concerns around intergenerational equity, and given the current state of Canada’s finances, fully debt-financing a major defence build-up would be unwise (Laurin and Lester 2023). In other words, Canada will have to make some hard choices about taxation and spending to achieve the NATO target while maintaining fiscal discipline.

Tax Increases

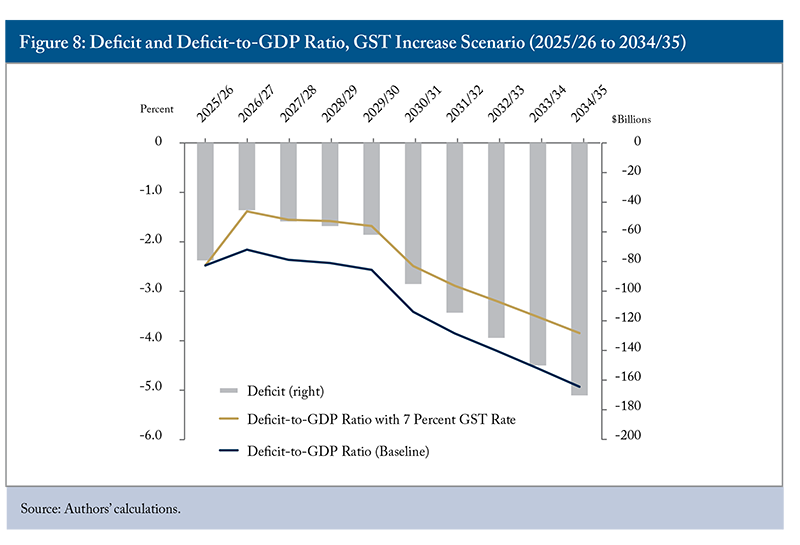

One option is to raise taxes. However, given the need to boost economic growth and productivity, we reject increased taxes on income and savings (Mintz, Laurin, and Dahir 2026). Instead, we look at raising the GST rate by two percentage points from 5 percent to 7 percent.

Unlike taxes on income and savings, consumption taxes such as the GST create fewer distortions and are less harmful to economic growth. In Canada, their regressive effects are mitigated by the GST tax credit that is designed to compensate lower-income people who would pay a larger share of their income in GST than those with higher incomes. When the GST rate was reduced in the mid-2000s from 7 percent to 5 percent, the GST credit was maintained at its original level. As a result, the regressive effects of increasing the GST by two percentage points were mitigated. Restoring the GST to 7 percent would raise federal government revenue by around $25 billion dollars in 2026/27, with revenues rising over time.

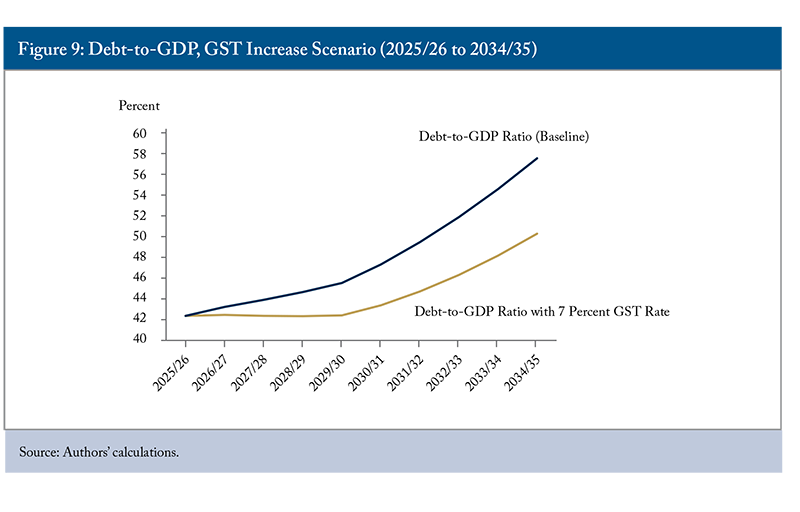

Still, while Canada’s fiscal position under this option would improve, it would not sufficiently improve the current fiscal anchors. A two-percentage-point increase would not permanently flatten the debt-to-GDP ratio (Figure 9). Although the government’s chosen fiscal anchor – a declining deficit/GDP ratio – would improve in the early part of the decade, it would worsen to below 2025/26 levels by the end of the forecast horizon (Figure 8).

Spending Reductions

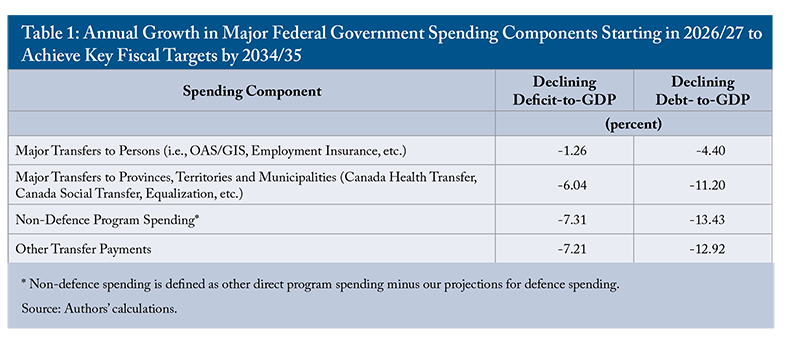

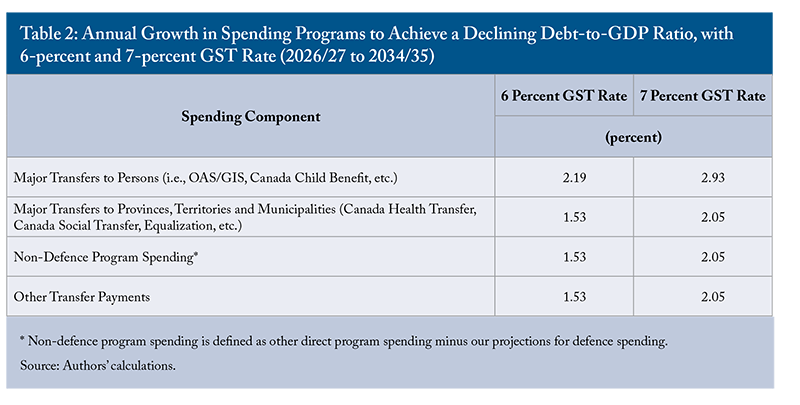

Having established that a two-percentage-point GST increase is insufficient to meet fiscal anchors – and that larger GST hikes or higher taxes on income and savings are undesirable – we now turn to spending-reduction options. Table 1 shows the annual growth in major spending categories required to meet the NATO target and place the deficit-to-GDP and debt-to-GDP ratios1010 We consider a debt-to-GDP ratio to be declining over time, should it fall below 42 percent by 2034/35. For a deficit-to-GDP ratio to be declining, we assume it must fall below 2.5 percent by 2034/35. on a declining path, assuming the increase in defence spending is financed entirely through restraint in that spending area starting in 2026/27.

The results are sobering. The government’s chosen fiscal anchor – a declining deficit-to-GDP ratio – is less challenging than a declining debt-to-GDP ratio. In concrete terms, if the federal government financed higher defence spending entirely through reductions to major transfers to persons, these transfers would have to be slashed to 73 percent of their 2024/25 value by 2034/35 – about $96 billion – to raise the required defence spending while achieving a declining debt-to-GDP ratio. If financed through cuts to transfers to other levels of government, spending would need to fall to 36 percent of its 2024/25 value or $38 billion. Non-defence program spending would need to fall to about 76 percent of its 2024/25 value.

Cutting non-defence spending is no easy task. Canadians have, in the past, wanted their governments to spend on things other than defence. Any attempts to reduce spending on the social programs that Canadians enjoy, or the transfers that individuals receive, are sure to face major public opposition. Concentrating cuts in any single area is therefore not a viable approach. Spreading restraint across multiple categories reduces the burden on any one program.

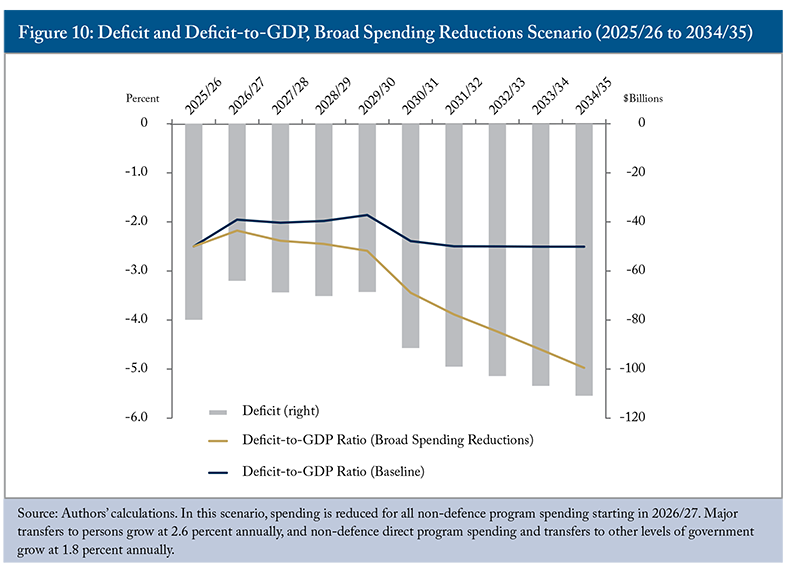

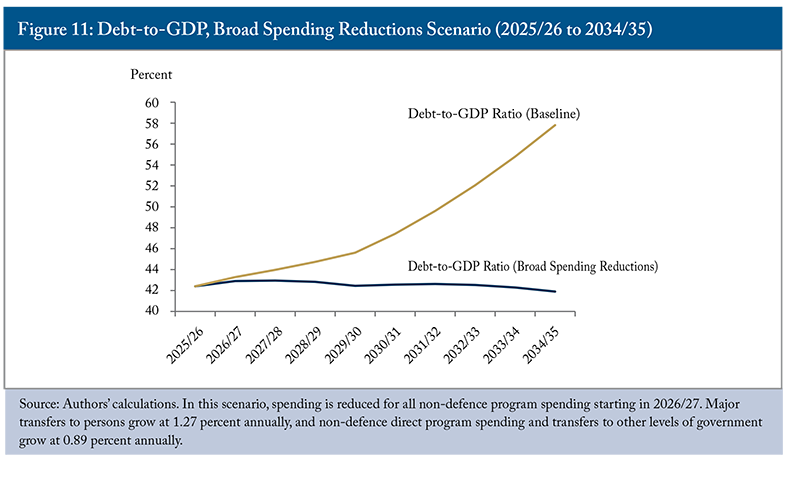

We therefore estimate how much these spending components would need to be curbed to achieve a declining deficit-to-GDP ratio (Figure 10) and a declining debt-to-GDP ratio (Figure 11) if the federal government decided to enact broad cuts to all of them at the same time.

Under this scenario, no single program would need to be cut outright, but spending growth would need to be curbed significantly. Raising defence spending to 3.5 percent of GDP by 2034/35 while still meeting the declining debt-to-GDP target would require non-defence direct program spending and transfers to other levels of government to grow only slightly, about 0.89 percent annually between 2026/27 and 2034/35, with transfers to persons growing at only 1.27 percent annually. This compares to annual growth in spending of 1.8 percent and 2.6 percent, respectively, to achieve the declining deficit-to-GDP ratio, which is the less stringent of the two evaluated fiscal anchors.

A Mixed Approach

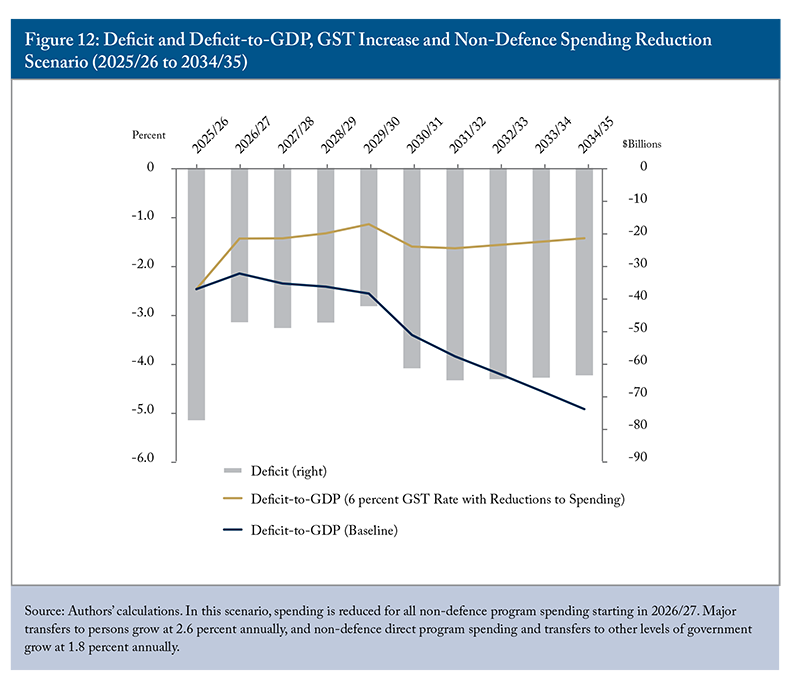

As just shown, broad spending cuts across major areas relieve the pressure on any one item, even though these reductions painfully compress these areas of traditionally steady spending. Pairing this with some extra revenue from an increase in the GST rate, and the pressure is relieved even more. Committing to NATO’s spending target will reshape federal spending. Accommodating this will require difficult decisions. We present our preferred mix of financing options.

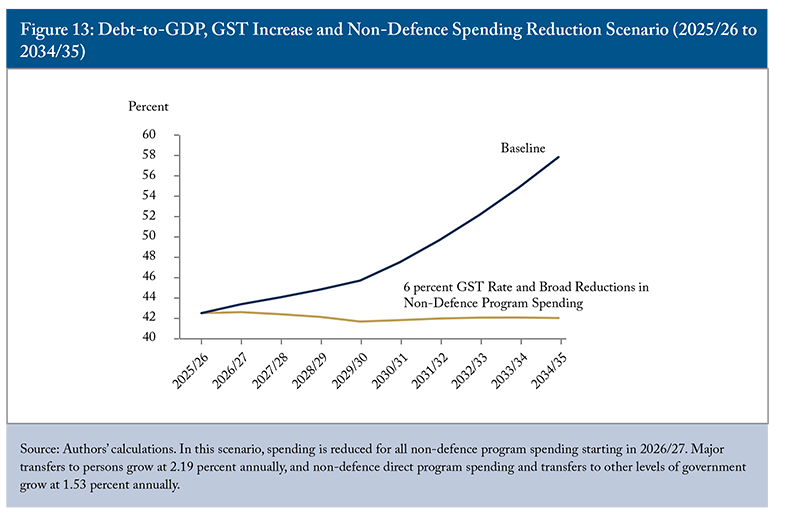

In this scenario, we apply expenditure reductions evenly among the federal government’s major spending areas after raising the GST rate by one percentage point. In Table 2, we present the annual program growth, assuming the government takes immediate action in 2026/27. This scenario would result in a declining deficit-to-GDP ratio (Figure 12), and the debt-to-GDP ratio would remain below 42 percent in 2034/35 (Figure 13).

The Fiscal Crunch in Boosting Military Capabilities under the NATO Pledge

Adopt a Mixed Financing Approach

The projected increase in defence spending will transform Canadian public finances. Accommodating this spending and the increase in security it will provide will require some hard fiscal choices about raising revenue, reducing spending, and borrowing. Each option has its trade-offs. We encourage the federal government to use a mix of existing tools to create fiscal room and avoid scrapping its fiscal anchor as defence spending ramps up.

Spreading the reductions across many programs would avoid having to make major, radical transformations in any single area. In our scenario, we avoided prescribing specific changes to any single area of spending, but the government has no such restriction. Slower growth in transfers to persons will require adjustments to programs such as OAS/GIS. Changes to these programs, such as benefit levels, benefit reductions due to income, or even age of eligibility (in the case of OAS), must be carefully considered.

As a federation, Canada gives provinces and territories extensive taxation powers. However, Canada’s federal government must uniquely finance and deliver national security. Given the major transformation of federal finances required to bring this about in a more dangerous world, the federal government should reduce its ever-growing role in funding provincially delivered social programs and encourage provinces to assume a greater share or improve efficiency.

Increasing revenue through a GST increase should also form part of the solution. It ensures that spending reductions need not be overly severe and is among the least harmful taxes on economic growth. This approach is also attractive because its regressive incidence is mitigated by GST credits.

Present a Plan

Budget 2025 commits to higher defence spending but does not set out a clear path to meet the NATO target. Our projections suggest that maintaining a linear path to 3.5 percent of GDP in core defence spending by 2034/35 would require around $111 billion between 2026/27 and 2029/30. Budget 2025 allocates only $81.8 billion in new defence spending in the decade beginning in 2025/26. Clearly, the gap between the required and announced amounts implies that Canada’s defence build-up is back rather than frontloaded.

A back-loaded approach risks delay and weakens credibility with NATO partners. To assuage concerns of NATO members and strengthen the fiscal picture for the federal government, it should publish a line item in its budget for defence spending to appear alongside other large spending categories.

Because NATO measures spending on a cash basis, the government should also report defence spending on a comparable basis to show progress toward its commitments. This would more clearly demonstrate the financial commitments of the country while also showing the pressures on federal finances.

Budget documents should further clarify what qualifies under the 1.5-percent dual-use and defence-related infrastructure target. Furthermore, those documents should also show how Canada will meet both components of the NATO pledge.

Improving Canada’s Military Capabilities Will Require Making Difficult Choices

Russian aggression helped to galvanize the political support for greater defence spending, especially in NATO’s Nordic countries. These countries have met their NATO 2-percent pledge, and most are planning to continue to expand defence spending in subsequent years. The political consensus has given way to a major modernization effort in military capabilities, but these Nordic countries are, for the most part, working from very solid public finances. This allows them to borrow and commit credibly to higher defence spending – a luxury Canada’s fiscal situation does not allow.

Critics of the projected increase in defence spending will point out that NATO’s defence spending-to-GDP measure reflects only a country’s annual allocation of its economic resources to defence and is not a reflection of a country’s military capabilities. However, given how far Canada has fallen behind on its military capabilities (Shimooka 2024), significant new investment is required regardless of NATO commitments.

Given that NATO capability targets are classified, public oversight is limited. The federal government should establish a parliamentary committee that has the necessary security clearance for this classified information. This could provide oversight as the government ramps up defence spending and ensures that the large injection of money in defence is being used to meet these capability targets.

Conclusion

The international order is being upended. Russia’s invasion of Ukraine has reminded Canadians that the risk of war is ever present. The potential for major armed conflict on a regional or global scale is a threat Canadians have not had to face since the end of the Cold War. To better improve our defence capabilities, Canada has committed to spending 5 percent of GDP on defence at a time of significant headwinds and when its public finances are deteriorating. The establishment of such a high defence spending target for NATO members by 2035 mirrors the dangers of the current geopolitical environment. Meeting it will require Canada to devote a much larger share of its income to defence than it does today.

To expand and modernize our military capabilities, Canada’s federal finances will undergo a major transformation over the next decade. We project that in 10 years’ time, the federal government should, according to its stated pledge, spend a similar amount on defence as it will on health, social programs, and equalization transfers to the provinces and territories. As a result, Canada is faced with hard fiscal choices: whether to finance this increase through higher taxes, reduced non-defence spending, or with debt to be paid for by future generations.

We recommend that the federal government present a comprehensive fiscal plan as to how it plans to meet its NATO pledge. The 2025 budget does not do so and there should be clearer plans in future budgets. There is no credible way for the economy to grow sufficiently to solve this budgetary dilemma. Nor are there straightforward spending reductions or tax increases that would not face major political pushback. Furthermore, asking future generations to pay the full cost for improved defence today would not be sustainable.

Canada must be adequately positioned to defend itself in a more dangerous world. Doing so requires some hard financial choices without a major run-up in debt. We recommend that Canada plan to phase in a one-percentage-point or greater increase in the GST. It should also limit the growth of non-defence spending over the next decade, including encouraging the provinces to take a large share of the fiscal costs for services that they – not the federal government – deliver.

Together, these steps would help finance a stronger military, restore fiscal discipline, and put Canada on a credible fiscal path for the coming decade.

The authors extend gratitude to Don Drummond, Jamie Golombek, Michael Langlais, Alexandre Laurin, John Lester, Nick Pantaleo, William B.P. Robson, Daniel Schwanen, and several anonymous referees for valuable comments and suggestions. The authors retain responsibility for any errors and the views expressed.

REFERENCES

Checherita-Westphal, Christina, and Laust Ladegård Særkjær. 2025. “Fiscal multipliers of defence spending: a short review of the empirical literature.” Economic Bulletin, Issue 6/2025. European Central Bank. September.

Canada. 2025a. Budget 2025: Canada Strong. Ottawa: Department of Finance. November 4. https://budget.canada.ca/2025/report-rapport/toc-tdm-en.html.

_______. 2025b. “Fiscal Reference Tables November 2025.” Ottawa: Department of Finance. November 7. https://www.canada.ca/en/department-finance/services/publications/fiscal-reference-tables/2025.html.

_______. 2025c. “Departmental Results Report 2024 25.” Ottawa: Department of National Defence. November 7. https://www.canada.ca/en/department-national-defence/corporate/reports-publications/departmental-results-report/2024-25-index.html.

_______. 2025d. “Statement from Minister McGuinty on Canadian Armed Forces Day.” Ottawa: Department of National Defence. June 1. https://www.canada.ca/en/department-national-defence/news/2025/06/statement-from-minister-mcguinty-on-canadian-armed-forces-day.html.

Hiebert, Daniel. 2025. Balancing Canada’s Population Growth and Ageing Through Immigration Policy. Commentary 682. Toronto: C.D. Howe Institute. May. https://cdhowe.org/publication/balancing-canadas-population-growth-and-ageing-through-immigration-policy.

Ilzetzki, Ethan. 2025. “Guns and Growth: The Economic Consequences of Defense Buildups.” Kiel Institute for the World Economy. February.

International Monetary Fund. 2025. “IMF Government Data.” IMF Data Portal.

Laurin, Alexandre, and John Lester. 2023. “Ottawa Needs a New Approach to Fiscal Policy.” E-Brief 338. Toronto: C.D. Howe Institute. March. https://cdhowe.org/publication/ottawa-needs-new-approach-fiscal-policy.

Mintz, Jack M., Alexandre Laurin, and Nicholas Dahir. 2026. “Big Bang” Tax Reform: Unleashing Growth in the Canadian Economy. Commentary 707. Toronto: C.D. Howe Institute. March. https://cdhowe.org/publication/big-bang-tax-reform-unleashing-growth-in-the-canadian-economy.

North Atlantic Treaty Organization. 2025. “Defence Expenditures and NATO’s 5 % Commitment.” North Atlantic Treaty Organization. June.

_______. 2026. “Secretary General’s Annual Report 2025.” March.

OECD. 2025. “Economic Outlook 117.” OECD Data Explorer. Accessed November 2025. https://data-explorer.oecd.org/vis?lc=en&df[ds]=dsDisseminateFinalDMZ&df[id]=DSD_EO%40DF_EO&df[ag]=OECD.ECO.MAD&df[vs]=1.3&dq=.GDPV_ANNPCT.A&lom=LASTNPERIODS&lo=5&to[TIME_PERIOD]=false.

Office of the Parliamentary Budget Officer (PBO). 2025. Planned Capital Spending under Canada’s Defence Policy: 2025 Update. October.

Perry, David, and Craig Stone. 2021. “Economic Benefits of Defence Spending.” Canadian Global Affairs Institute. December.

Robson, William B.P., and Parisa Mahboubi. 2024. Another Day Older and Deeper in Debt: The Fiscal Implications of Demographic Change for Ottawa and the Provinces. Commentary 665. Toronto: C.D. Howe Institute. https://cdhowe.org/publication/another-day-older-and-deeper-debt-fiscal-implications-demographic-change/.

Schwanen, Daniel, and Rosalie Wyonch. 2018. “Canada’s 2018 Innovation Policy Report Card.” E-Brief 273. Toronto: C.D. Howe Institute. August. https://cdhowe.org/publication/another-day-older-and-deeper-debt-fiscal-implications-demographic-change.

Shimooka, Richard. 2024. Canada’s Defence Capabilities Are in Disarray. Here Are the Three Biggest Reasons Why. Macdonald-Laurier Institute. August 16.

Surico, Paulo, and Juan Antolin-Diaz. 2025. “Defence spending fuels innovation – but not how you think.” Think (London Business School). April. https://www.london.edu/think/defence-spending-fuels-innovation-but-not-how-you-think?utm_source=copilot.com.

Taylor, Scott. 2024. “NATO Nagging? Defence Spending Takes Heat from Allies.” The Hill Times. July 15.

Van Dyk, Spencer. 2024. “‘I Expect More:’ NATO Head on Canada’s Need to Increase Defence Spending.” CTV News. June 20.