From: Don Drummond and Parisa Mahboubi

To: Fiscal and monetary policy decision-makers

Date: April 22, 2026

Re: Canada's Economy Is Growing Far Slower Than Ottawa Thinks

Canada’s official economic forecasters are projecting growth that may exceed what its new demographic reality can support. With a federal Economic Statement imminent and the Bank of Canada’s next Monetary Policy Report approaching, that gap deserves attention.

The federal government has sharply reduced immigration targets to just under 1 percent of the population annually, down from the record inflows of recent years. That policy shift is defensible given pressures on housing, infrastructure, and public services. But it also has consequences that have not yet been fully incorporated into official macroeconomic forecasts.

Fewer newcomers mean slower labour force growth. Slower labour force growth means slower potential output growth. The result is a lower growth trajectory than projections currently embedded in Budget 2025 and Bank of Canada’s forecasts.

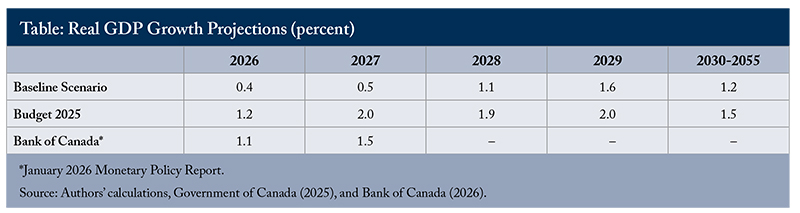

Supply-side projections derived using a growth-accounting framework following Laurin and Drummond (2021) – combining Statistics Canada’s 2026 population outlook under a medium immigration scenario, Canada’s post-2000 productivity growth of 0.84 percent annually, and observed hours-worked patterns – point to real GDP growth of just 0.4 percent in 2026 and 0.5 percent in 2027. That is well below official projections (see Table).

The gap is not marginal. Budget 2025 assumes growth this year roughly three times higher than the supply-side estimate. By 2029, the level of real GDP implied by the baseline is about 3.4 percent below the budget path. Over the longer run, the difference between 1.2 and 1.5 percent average growth, the respective figures from the supply-side estimates and those used in the 2025 Budget, translates into a GDP level roughly 7.7 percent lower by 2055. Including near-term deviations, the cumulative gap exceeds 10 percent.

These differences reflect different analytical frameworks. Official projections are implicitly more demand-led, assuming that domestic and external spending will be sufficient to sustain growth near historical norms. The supply-side framework takes a different approach. It asks what the economy can produce under normal conditions – neither overheated nor demand-constrained – given its demographic inputs, productivity trends, and labour supply constraints. Under current immigration policy, that answer is materially lower.

This distinction matters because it shapes policy decisions now being made. On the fiscal side, planning around 1.5 to 2.0 percent annual growth when underlying capacity supports barely half that level risks systematic forecast errors. Revenues will underperform relative to expectations, and debt dynamics will be less favourable than projected. The forthcoming Economic Statement should explicitly reconcile fiscal assumptions with demographic realities rather than relying on outdated growth paths.

For monetary policy, the implications are highly consequential as they alter the perception of the cyclical state of the economy. Weak output and employment data in 2026 and 2027 may resemble a cyclical slowdown driven by insufficient demand. But if the underlying constraint is labour supply rather than spending, conventional policy responses – particularly aggressive rate cuts – risk adding inflationary pressure without restoring lost capacity. Misdiagnosing a structural slowdown as a cyclical one is not just a technical error; it is a policy risk.

None of this implies that Canada’s economy is in crisis. It is adjusting to a deliberate shift in immigration policy and, with it, a lower long-run growth trajectory. That adjustment may be consistent with broader policy objectives. But it does require a corresponding shift in expectations.

As the Economic Statement and the next Monetary Policy Report take shape, policymakers must stop projecting growth that reflects yesterday’s demographic reality and align forecasts with the one now in place with the new immigration targets.

That alignment is no longer optional; it is foundational to sound fiscal planning, effective monetary policy, and credible economic stewardship.

Don Drummond is a Stauffer-Dunning Fellow at Queen’s University and a Fellow-In-Residence at the C.D. Howe Institute, where Parisa Mahboubi is an Associate Director of Research.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.