by Nicholas Rivers

- Canada’s industrial carbon pricing systems, covering roughly 40 percent of national emissions, aim to reduce greenhouse gases while protecting competitiveness, but are being undermined by a poorly designed federal “benchmark.”

- The current benchmark relies on a subjective and opaque “demand test” to assess system stringency, resulting in overly generous performance standards, low compliance credit prices, and inconsistent outcomes across provinces.

- This report proposes introducing a price floor for compliance credits that ensures a minimum carbon price across jurisdictions while allowing flexibility in performance standards.

- A price floor would improve transparency and enforceability, reduce transaction costs, align incentives across regions, and decouple emissions reductions from competitiveness concerns – enabling more effective and durable carbon pricing in Canada.

Introduction

One of Mark Carney’s first acts as prime minister was to eliminate Canada’s consumer carbon tax, ending the consumer-facing carbon pricing policy regime that began in British Columbia and Quebec and was later expanded nationally under Justin Trudeau.11 Major, Darren. 2025. “Carney Kills Consumer Carbon Tax in First Move as Prime Minister.” CBC News. March 14. https://www.cbc.ca/news/politics/mark-carney-drops-carbon-tax-1.7484290 However, despite this rollback, carbon pricing remains in place for large industrial emitters. Canada’s industrial carbon pricing systems cover about 40 percent of total greenhouse gas emissions (Canadian Climate Institute 2025) and are at the core of the country’s climate change plan,22 440 Megatonnes. 2024. “Which Canadian climate policies will have the biggest impact by 2030?” March 21. https://440megatonnes.ca/insight/industrial-carbon-pricing-systems-driver-emissions-reductions/ as they are for nearly all OECD countries.33 World Bank. 2025. “State and Trends of Carbon Pricing Dashboard.” https://carbonpricingdashboard.worldbank.org/

Canada’s industrial carbon pricing systems aim to reduce emissions cost-effectively while preserving the international competitiveness of regulated industries such as steel, cement, oil and gas, and fertilizers.

Both provinces and territories and the federal government implement these systems.44 Environment and Climate Change Canada. 2025. “Carbon Pricing Systems Across Canada.” December 17. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work.html Reflecting overlapping constitutional authority over greenhouse gas regulation, the federal government has established minimum standards for carbon pricing referred to as the “benchmark.”55 Environment and Climate Change Canada. 2023. “The Federal Carbon Pollution Pricing Benchmark.” June 5. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work/carbon-pollution-pricing-federal-benchmark-information.html Provinces and territories can either implement their own carbon pricing systems that satisfy the benchmark or, if they do not, federal regulations apply to large emitters in that jurisdiction to ensure consistency across the country. This approach is one form of “equivalency agreement,” a long-standing component of environmental federalism in Canada.66 Environment and Climate Change Canada. 2026. “Canadian Environmental Protection Act: Equivalency Agreements.” February 25. https://www.canada.ca/en/environment-climate-change/services/canadian-environmental-protection-act-registry/agreements/equivalency.html

Despite its promise, industrial carbon pricing is not delivering on its full aims in Canada. As this report explains, this shortfall is partly due to a poorly structured federal “benchmark,” which determines whether provincial and territorial systems are sufficiently stringent. The federal government has an opportunity to address this shortcoming as part of its scheduled 2026 review of carbon pricing.77 Environment and Climate Change Canada. 2025. “Discussion Paper: Driving Effective Carbon Markets in Canada.” December 19. https://www.canada.ca/en/environment-climate-change/corporate/transparency/consultations/comment-driving-effective-carbon-markets/discussion-paper.html It has also indicated its intent to improve system performance through its Carbon Competitiveness Strategy88 Environment and Climate Change Canada. 2025. “Strengthening Carbon Markets.” November 9. https://www.canada.ca/en/environment-climate-change/news/2025/11/strengthening-carbon-markets.html and a recent memorandum of understanding with Alberta.99 Prime Minister of Canada. 2025. “Canada-Alberta Memorandum of Understanding.” November 27. https://www.pm.gc.ca/en/news/backgrounders/2025/11/27/canada-alberta-memorandum-understanding

This Commentary proposes amending the benchmark to require a price floor in all price-based carbon pricing systems in Canada. A price floor would reduce ambiguity and subjectivity associated with the current benchmark and help ensure that all emitters across the country face similar incentives to reduce emissions.

The report begins by outlining how industrial carbon pricing currently works in Canada. It delineates how the benchmark is applied to evaluate carbon pricing systems proposed by provincial and territorial governments and focuses on shortcomings of the existing benchmark and its consequences. Finally, it proposes introducing a price floor to solve these shortcomings and explains how this amendment to the benchmark would work and what outcomes it could produce.

Background: How Canada’s Carbon Pricing System Currently Works

In 2018, Canada passed the Greenhouse Gas Pollution Pricing Act (GGPPA), which aims to mitigate climate change through the “Pan-Canadian application of pricing mechanisms to a broad set of greenhouse gas emission sources.”1010 Greenhouse Gas Pollution Pricing Act, S.C. 2018, c. 12, s. 186. The Act has two parts. Part 1 implements a fuel charge under which fossil fuels such as natural gas and gasoline face a charge in proportion to their carbon content. This charge has been set to zero as of April 2025, which effectively ends direct exposure to carbon pricing for most Canadians.1111 Canada Revenue Agency. 2025. “Fuel Charge Rates.” April 1. https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/fcrates/fuel-charge-rates.html Part 2 focuses on emissions from large industrial facilities, which are exempt from the fuel charge. Large industrial carbon pricing remains in place in Canada.

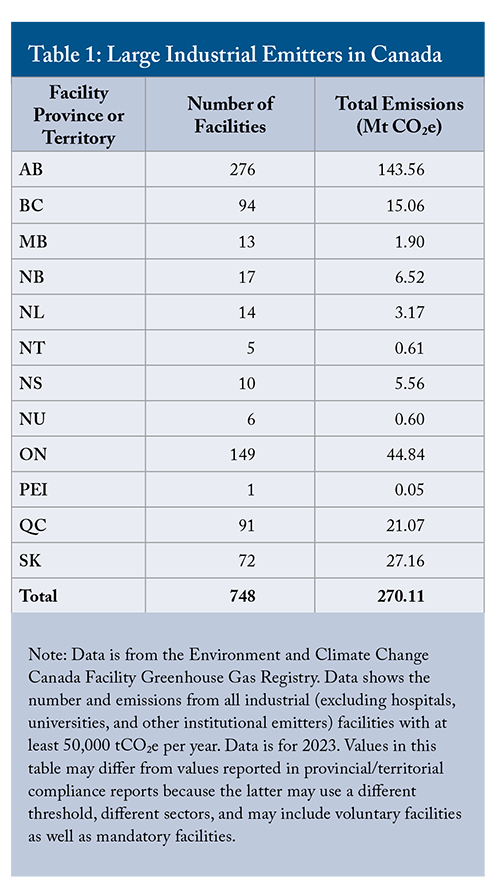

Large industrial facilities are defined in different ways across the country, and there is no consistent national index of facilities defined as large emitters (Cui 2025). However, a widely adopted definition for a large industrial emitter is an industrial facility that emits more than 50,000 tonnes of CO2e annually. Table 1 shows that based on this definition, there are roughly 750 large industrial emitters across Canada, with total emissions of 270 Mt CO2e in 2023, roughly 40 percent of the Canadian total. These large industrial emitters continue to be exposed to carbon prices through Part 2 of the GGPPA.

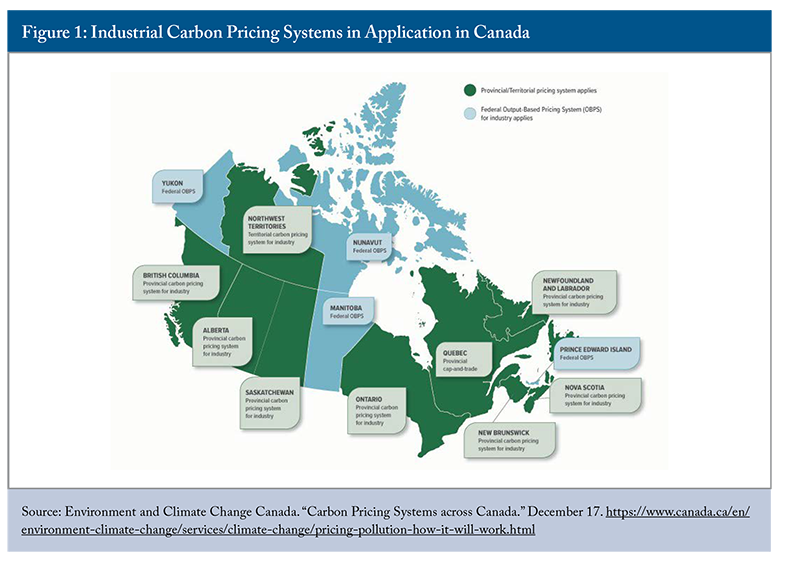

Two features of the GGPPA shape how carbon pricing applies to these facilities. First, the GGPPA reflects a federalist approach. Part 2 of the Act implements a federal carbon pricing system for large industrial emitters.1212 Environment and Climate Change Canada. 2026. “Output-Based Pricing System.” February 6. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work/output-based-pricing-system.html However, the federal system only applies to provinces and territories (P&Ts) that are explicitly listed in the Act. Jurisdictions are listed if they do not implement an industrial carbon pricing system of their own of sufficient stringency. Currently, Manitoba, Prince Edward Island, Yukon, and Nunavut are listed P&Ts, meaning the federal industrial carbon pricing system applies, as shown in Figure 1. Other P&Ts implement their own carbon pricing system for large industrial emitters, so the federal system does not apply.1313 Environment and Climate Change Canada. 2025. “Carbon Pricing Systems Across Canada.” December 17. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work.html

Whether a P&T is listed (and thus subject to the federal industrial carbon pricing system) is determined by comparing its carbon pricing system to the federal benchmark.1414 Environment and Climate Change Canada. 2021. “Update to the Pan-Canadian Approach to Carbon Pollution Pricing 2023-2030.” August 5. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work/carbon-pollution-pricing-federal-benchmark-information/federal-benchmark-2023-2030.html The federal benchmark requires that P&T systems meet minimum standards for carbon price levels, emissions coverage, and reporting.

Second, Canada’s industrial carbon pricing systems vary in design. There are provisions to allow for both explicit price-based systems, such as a carbon tax, as well as quantity-based systems, such as a cap-and-trade system.1515 In practice, most carbon pricing systems in place in Canada are hybrid price-quantity systems, and the distinction between price-based and quantity-based systems in the current benchmark should be re-evaluated to determine if it is still appropriate. For example, in Alberta’s system, which is considered price-based, the maximum quantity of emissions that can be produced depends on the number of compliance permits in circulation (a feature normally associated with quantity-based systems). In Quebec’s system, which is considered quantity-based, compliance credit prices are bounded by a price floor, which in practice is determinative of the price most of the time (a feature normally associated with price-based systems). Both systems contain elements of price-based and quantity-based systems. The current approach to classifying systems as quantity-based or price-based should thus be reconsidered. This point will not be further developed here, although it should be taken up in evaluating the benchmark. In practice, most existing industrial carbon pricing systems in Canada are considered price-based systems and function using tradable performance standards (TPS). The federal Output-Based Pricing System (OBPS) and Alberta’s Technology Innovation and Emissions Reduction (TIER) system are examples of this approach.

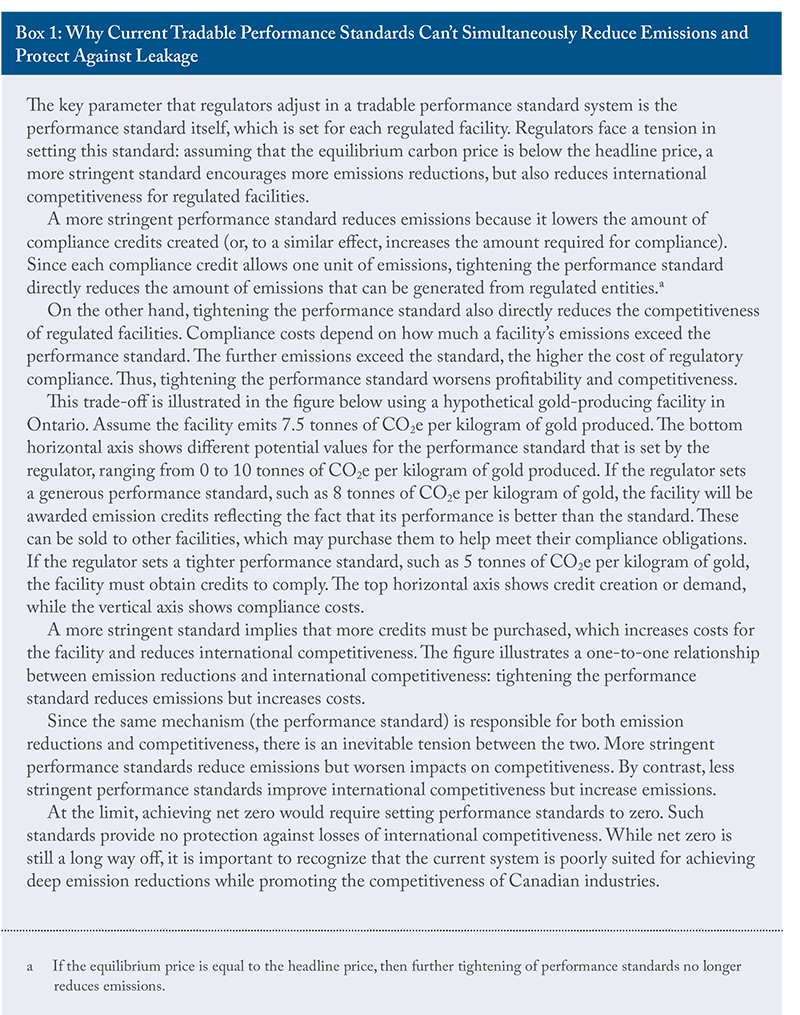

A tradable performance standard sets a performance standard for each regulated facility expressed in tonnes of allowable emissions per unit of facility output. Regulators can base these standards on sector average emissions intensity, best available technology, historical facility performance, or other factors. For example, a standard might be set at 90 percent of industry-average emission intensity or 85 percent of a facility’s recent historical emission intensity. Total allowable facility emissions are calculated as the product of the performance standard, measured in tonnes of greenhouse gases per unit of facility output, and the facility output. For example, in Ontario, gold facilities can emit a maximum of 7.21 tonnes of CO2e per kilogram of gold, so a facility producing 1,000 kilograms of gold would have an emission limit of 7,210 tonnes of CO2 (Ontario Ministry of Environment, Conservation and Parks 2024).

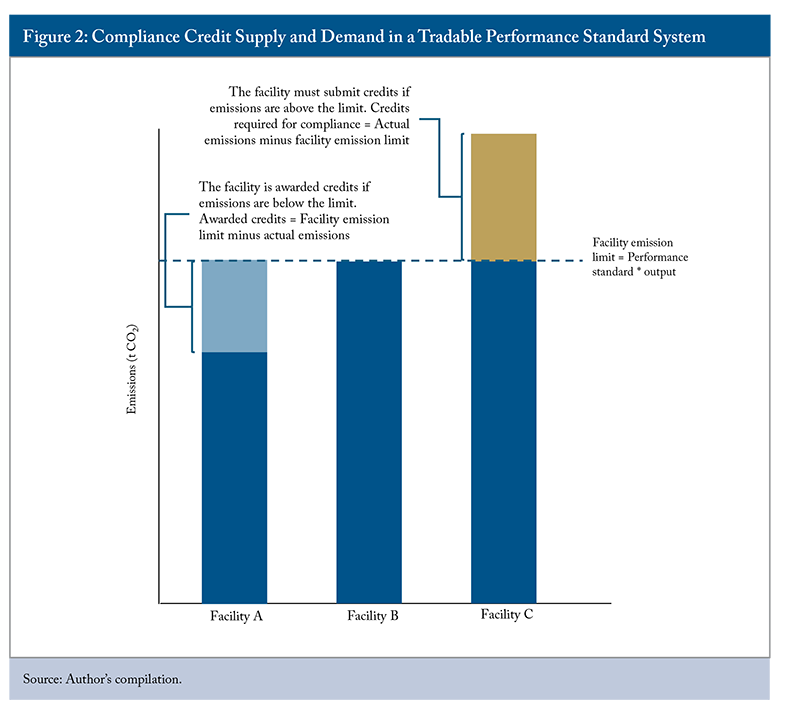

As shown in Figure 2, a facility that emits less than its limit earns one compliance credit for each tonne below the threshold.1616 Throughout the paper, the term “compliance credit” is used to refer to any credit that permits the release of one unit of greenhouse gas emissions, with no distinction between “excess emissions payments” (compliance credits purchased at the headline carbon price) and “surplus credits” (compliance credits awarded to firms with emissions below their facility limit). If it exceeds the limit, it must obtain sufficient compliance credits to close the gap between the limit and its actual emissions. Facilities can purchase credits from other firms at market prices or buy them from the regulator at the headline carbon price.1717 It can also use retained credits from a prior period or use credits generated under an offset protocol. The regulator’s standing offer to sell credits at this price effectively sets a ceiling on compliance credit prices.

Tradable performance standards limit the overall costs of carbon pricing for regulated facilities and preserve competitiveness and profitability in international markets. Facilities incur costs only to the extent that their emissions intensity exceeds the standard. Facilities that perform better than the standard can generate credits, creating an additional revenue stream and potentially improving competitiveness, as shown in Figure 2.

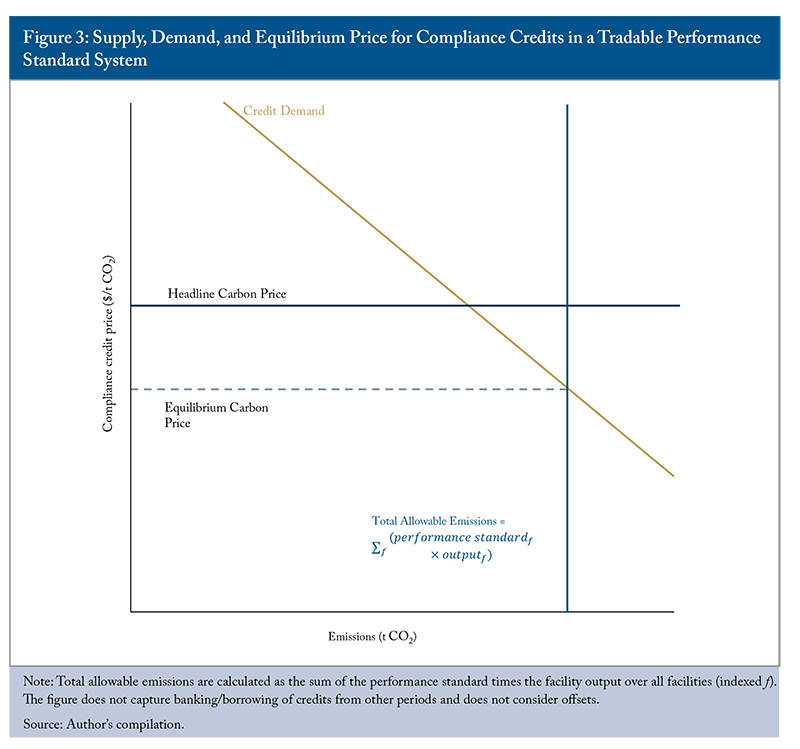

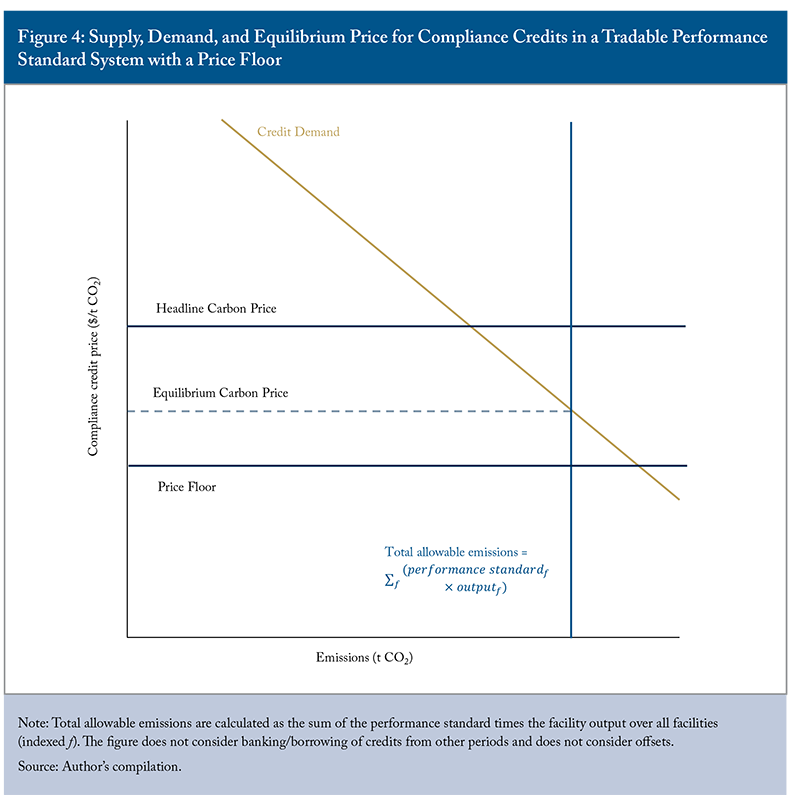

Across all regulated facilities in a system, the sum of the facility emission limits determines total allowable emissions.1818 In practice, total allowable emissions can be augmented from previously banked compliance credits. Likewise, carrying forward compliance credits to a future period reduces allowable emissions this period. For simplicity, banking and borrowing of credits have been abstracted here. Demand for compliance credits depends on the availability of emissions-reducing technologies and access to capital. Facilities demand more compliance credits when their price is lower. The intersection between total allowable emissions and credit demand determines the equilibrium price of compliance credits, as shown in Figure 3.1919 Demand for credits at the market level is illustrated as a straight downward-sloping line, as is conventional, although, in reality, credit constraints, lumpy investments, and other factors imply the true relationship between credit demand and price is not perfectly linear. This price will not exceed the headline carbon price, since facilities can purchase compliance credits from the regulator at this price.2020 In practice, most tradable performance standards differentiate between credits purchased from government for compliance (at the headline price) and credits awarded to facilities for being below their performance standard, and so there are limited cases where the price of performance credits may exceed the headline price. In Canada, most tradable performance standard systems allow credits awarded for performance to be banked for future periods, but banking is disallowed for excess emission payment credits. For simplicity, there is no distinction between the different types of credits in this analysis. The equilibrium carbon price is the price facilities actually face when buying or selling compliance credits on the market, and is an important determinant of how willing they are to pursue or forgo opportunities to invest in emission-reducing projects.2121 The analysis presented here is purely static, whereas carbon pricing systems in Canada typically change over time and allow banking and borrowing of compliance permits. These features complicate the analysis but do not fundamentally alter the logic, so they are not discussed further here.

Under Canada’s current tradable performance standard systems, the federal benchmark requires all regulators to apply a common “headline carbon price.” However, each regulator independently sets performance standard for regulated facilities. As shown in Figure 3, less stringent performance standards shift the vertical line to the right. This should result in more overall emissions and a lower equilibrium price for compliance credits. Under the current system design, the level of performance standard is a critical design parameter that determines the stringency of the carbon pricing system. As described in the following section, the federal government evaluates these choices using the “demand test.”

What’s not working?

In theory, the GGPPA’s approach to carbon pricing is pragmatic and effective. It has encouraged the widespread adoption of tradable performance standards. This type of policy reduces the overall cost burden of carbon pricing on regulated industries, while maintaining an incentive for facilities to reduce emissions (Bohringer, Fischer, and Rivers 2023). This approach is especially suitable to address concerns about carbon leakage and losses in international competitiveness.2222 In Quebec, which uses a cap-and-trade system, competitiveness/leakage impacts on trade-exposed and emission-intensive industries are avoided in essentially the same way as in tradable performance standard systems prevalent in the rest of the country: https://www.environnement.gouv.qc.ca/changements/carbone/methode-calcul-en.htm.

Its federalist design is also, in theory, elegant. The federal government sets a minimum standard for carbon pricing which all P&Ts must meet. Where a P&T does not implement a sufficiently stringent system, the federal government applies its own. At the same time, P&Ts have considerable latitude to design a system in a way that works best for their jurisdiction. Smaller jurisdictions with lower administrative capacity can elect to delegate development of their system to the federal government. P&Ts with carbon pricing systems that predate the GGPPA can continue to use their existing systems. In theory, this approach should result in a comparable set of carbon pricing systems across the country, but with specific design details tailored to each region, where beneficial.

In practice, however, the GGPPA’s approach to carbon pricing is not achieving the federal government’s stated greenhouse gas reduction goals (Government of Canada 2025). The core issue is the poorly structured federal benchmark used to evaluate P&T carbon pricing systems. The benchmark sets requirements for scope, stringency, and reporting, and determines whether a system is comparable to the federal OBPS.2323 Separate criteria are used to evaluate price-based and quantity-based systems. While this report argues that this is no longer a valid categorization (see footnote 5), it focuses on price-based systems, which are the main type of carbon pricing system in use across Canada. This report focuses on how the benchmark evaluates the stringency of P&T carbon pricing systems. As explained above, stringency depends heavily on how performance standards are set. Less stringent performance standards mean lower emissions and a lower equilibrium price for compliance credits (see Figure 3 and associated text).

The current benchmark has weaknesses in both its administration and its economic outcomes.

Administrative Deficiencies of the Federal Benchmark

Subjectivity

The current benchmark introduces significant subjectivity in evaluating the stringency of a P&T’s existing carbon pricing system. As a result, judgments about whether a system is compliant can be influenced by analyst assumptions and political considerations. This subjectivity makes it difficult for the federal government to enforce the benchmark, since enforcement is more likely to be seen as arbitrary. It also invites P&Ts to submit weaker carbon pricing systems, expecting that they can negotiate over enforcement. Overall, the current benchmark does not allow for a clear and unambiguous determination of whether a P&T system is compliant with the benchmark or not: there is no clear red line that separates a compliant system from a non-compliant system.

This subjectivity is exhibited in the federal government’s use of the “demand test” to determine whether a P&T carbon pricing system will result in a price for compliance credits that is comparable to the headline price.2424 Environment and Climate Change Canada. 2021. “Update to the Pan-Canadian Approach to Carbon Pollution Pricing 2023-2030.” August 5. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work/carbon-pollution-pricing-federal-benchmark-information/federal-benchmark-2023-2030.html With reference to Figure 3, the demand test aims to determine whether the performance standards implemented by a P&T will lead to an equilibrium carbon price at least as high as the headline price. The federal government implements this test using an in-house economic model (EC-PRO).2525 Environment and Climate Change Canada. 2018. “Cost-Benefit Analysis Framework for an Output-Based Pricing System.” December 20. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work/output-based-pricing-system/cost-benefit-analysis-framework-regulations.html But models such as EC-PRO are not designed for this purpose. They rely on “representative firms” that aggregate all existing facilities and do not typically account for technological differences or real-world constraints. Economic models have a substantial number of uncertain parameters, including elasticities, model closure assumptions, and behavioural assumptions, which are not verified and mean that results are uncertain and can significantly affect results (Antimiani, Costantini, and Paglialunga 2015). They are best used for “what-if” analyses rather than for detailed, facility-level calculations.2626 The recent Alberta-Canada memorandum of understanding commits the parties to developing appropriate performance standards. While this is potentially encouraging, it does not resolve the problem identified here: it is difficult to set a performance standard to accurately hit a price target.

Lack of transparency

The current benchmark relies on inputs that are not easily visible. To judge the stringency of a P&T system, the “demand test” models net credit supply and demand. Credit supply is determined by P&T administrative decisions about performance standards that are often complex and not publicly available. In some cases, multiple methodologies exist for setting performance standards, yet neither the final standard nor facility-level emissions relative to that standard are disclosed.

Although the benchmark requires some reporting about compliance outcomes, reporting is limited, often delayed, and typically excludes information about prices or exchange of compliance credits or facility-level compliance metrics. This lack of information and complexity makes it difficult to assess the effectiveness of existing carbon pricing systems. Finally, while the federal government uses the demand test to evaluate stringency, it does not publish the inputs or results, making it impossible for third parties to scrutinize the inputs, the approach used, or the results.

Economic Deficiencies of the Federal Benchmark

High transaction costs

The current system does not keep transaction costs low. Carbon pricing is typically considered the most cost-effective approach to reducing greenhouse gas emissions. However, this depends on transparent prices and the ability to trade compliance credits easily (Hahn and Stavins 2011). When transaction costs are high, this cost-effectiveness breaks down.

In practice, many Canadian systems exhibit these challenges. Some provinces have fewer than two dozen covered entities, no central exchange, and limited information about compliance credit trading prices or volumes. In this context, buyers and sellers of credits can’t easily find each other, don’t know the going price of compliance credits, and are less likely to engage in trade. These frictions hinder the cost-effectiveness of the system. The federal benchmark does not create this problem, but neither does it resolve it.

Unequal prices across jurisdictions

The current system also does not maintain consistent carbon prices across jurisdictions. As shown in Table 1, Canada has less than 1,000 large industrial emitters, and only Alberta and Ontario have more than 100. Many regions have only a handful of large emitters: Nova Scotia has 10, Newfoundland and Labrador has 14, and New Brunswick has 17. Liquidity is likely low in carbon pricing regimes in these regions, meaning that buyers and sellers will have difficulty finding others to trade with at any given time.

In addition, the highly fractured nature of carbon pricing across the federation means that carbon prices can be different in each region. If, for example, the carbon price is high in province A but low in province B, emitters in province A will need to evaluate options to manage their carbon compliance costs, including the cost to significantly curtail emissions, while those in province B will not. This discrepancy in emission reduction effort is costly and undermines the value of carbon pricing. Once again, this is not a problem directly created by the federal benchmark, but it persists under the existing benchmark.

Tension between decarbonization and competitiveness

The current system also creates a tension between decarbonization and competitiveness. Without a globally harmonized approach to decarbonization, efforts to reduce emissions need to consider emissions leakage and potential impacts on international competitiveness. Canada’s carbon pricing policies are intended to reduce emissions while avoiding losses to international competitiveness and emissions leakage due to uneven climate policies between countries.2727 Environment and Climate Change Canada. 2026. “Output-Based Pricing System.” February 6. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work/output-based-pricing-system.html

Unfortunately, in the carbon pricing systems as currently implemented, protecting competitiveness comes at the expense of decarbonization, and vice versa, as described in Box 1. This trade-off is already important but will become more evident as deeper emission reduction targets are pursued.

Consequences of Benchmark Deficiencies

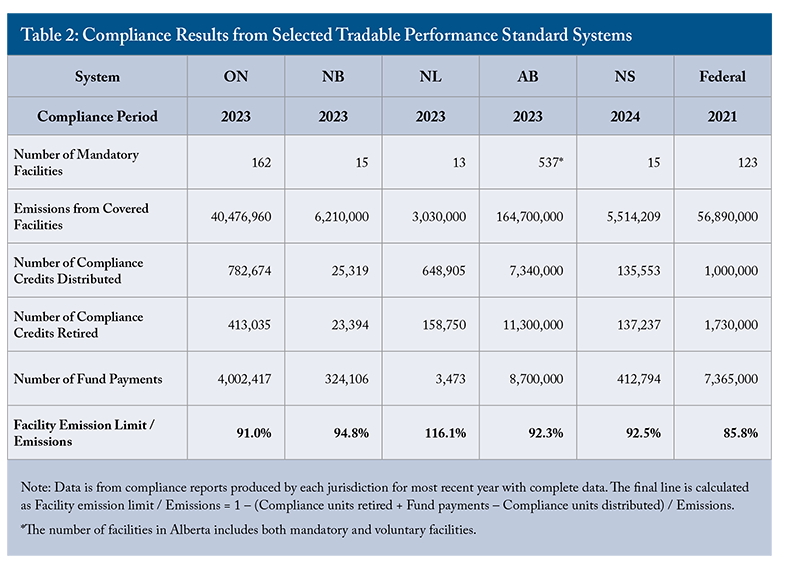

These deficiencies in the benchmark have led to clear problems with Canada’s carbon pricing systems. First and most importantly, the difficulty, subjectivity, and opacity associated with applying the “demand test” have led regulators to set relatively generous performance standards. Table 2 shows compliance results for selected tradable performance standard-type systems in operation in Canada.2828 No report is available for Saskatchewan (which has effectively paused its system) or for British Columbia (which recently transitioned from a carbon tax to a tradable performance standard-type system). The table shows the number of compliance credits distributed in each system for the year indicated. These credits are created by facilities that have emission intensity below (better than) their performance standard, as shown in Figure 2. Setting more stringent performance standards results in fewer compliance credits being distributed.

The table also shows how facilities with emission intensity above their performance standard comply: either by retiring compliance credits or by paying for excess emission units at the headline price. Using an accounting identity, it is possible to calculate the average performance standards set in each province as a fraction of emissions. Most systems set relatively generous performance standards requiring less than a 10 percent reduction in emissions on average.

The results also highlight significant discrepancies in the stringency of carbon pricing across provinces. Facilities regulated by the federal system must reduce emissions by almost 20 percentage points more than those in Newfoundland and Labrador. This wide variation suggests that the “demand test” used to evaluate provincial plans for credit allocation is not serving its purpose. Additional evidence comes from compliance credit prices: although systematic public data on prices is nonexistent, ad hoc data suggests that the equilibrium compliance credit prices are well below the headline price in Alberta2929 Ryan, Madeline, and David Lademan. 2025. “Alberta TIER Prices Jump 25% After MOU, But Outlook Remains Uncertain.” S&P Global News. December 3. https://www.spglobal.com/energy/en/news-research/latest-news/electric-power/120325-alberta-tier-prices-jump-25-after-mou-but-outlook-remains-uncertain and Ontario.3030 Ontario Ministry of Environment, Conservation, and Parks. 2026. “Emissions Performance Standards (EPS) Program Aggregated Compliance Data.” January. https://data.ontario.ca/dataset/emissions-performance-standards-eps-program-aggregated-compliance-data/resource/221b875b-86dc-4c9d-80a4-3fcf1d3f5277

Second, the lack of a clear, objective, and well-enforced benchmark has opened the door to P&Ts to weaken their carbon pricing systems. For example, Alberta has recently introduced legislation that will create additional compliance units when a facility undertakes a defined emission reduction project.3131 Technology Innovation and Emissions Reduction Amendment Regulation. Order in Council 369/2025. While this policy will create incentives for selected projects, the additional compliance credits will result in a net increase in emissions if the equilibrium carbon price is below the headline price, since each credit allows one tonne of emissions. Alberta has also suspended increases to its headline carbon price, limiting future emissions reductions.3232 McCarthy Tétrault. 2025. “Alberta Government Indefinitely Freezes Cost of TIER Fund Credits at $95 per Tonne.” May 15. https://www.mccarthy.ca/en/insights/blogs/canadian-energy-perspectives/alberta-government-indefinitely-freezes-cost-tier-fund-credits-95-tonne

Saskatchewan has taken an even more dramatic move by ceasing enforcement of its performance standard for large industrial emitters altogether.3333 Government of Saskatchewan. 2025. “Saskatchewan is the First Province in Canada to be Carbon Tax Free.” March 27. https://www.saskatchewan.ca/government/news-and-media/2025/march/27/saskatchewan-is-the-first-province-in-canada-to-be-carbon-tax-free While these political manoeuvres do not directly result from the benchmark’s design, a clearer and more objective benchmark would make enforcement easier. Overall, the over-allocation of credits along with other measures that reduce credit prices and increase supply weaken carbon pricing markets in Canada and limit their effectiveness in reducing emissions.

Proposal for a price floor to address problems with the current benchmark

To address these shortcomings, the federal government should update the carbon pricing benchmark to require all price-based systems to implement a standing offer to purchase any amount of compliance credits generated at a fixed and gradually increasing price.3434 The price could be differentiated according to compliance credit vintage and could be designed to only apply to newly issued permits, not to held-over permits from prior periods. This would establish a price floor. The floor could be set exactly equal to the current headline carbon price, or could be set at a fixed decrement to the headline carbon price (e.g., 10 percent or $25/t below), or could be set independently of the current headline carbon price (e.g., equal to the price floor used in the Western Climate Initiative or set at a politically determined level, such as $130/t as agreed upon in the Alberta-Canada MOU3535 Prime Minister of Canada. 2025. “Canada-Alberta Memorandum of Understanding.” November 27. https://www.pm.gc.ca/en/news/backgrounders/2025/11/27/canada-alberta-memorandum-understanding). In all cases, the unconditional buy offer would ensure that compliance credit prices never traded below this level.3636 The federal benchmark mandates the stringency of P&T carbon pricing systems without prescribing particular design elements. It is unclear whether the price floor proposed here would be considered too prescriptive to be included in the benchmark. An alternative approach would be to require that all compliance credits transact above a minimum level (the price floor) while remaining agnostic as to the mechanism to create this condition. Details of the price floor mechanism could be provided as “guidance” consistent with the existing benchmark.

Figure 4 illustrates the proposed system. Under the current design, regulators sell an unlimited amount of compliance credits at the pre-specified (headline) price. These compliance credits can be used by facilities whose emissions exceed their performance standard as part of regulatory compliance. The price floor would work in the same way, but in reverse. Regulators would purchase an unlimited amount of compliance credits at a pre-specified (floor) price. Together, the ceiling and floor would bound compliance credit prices within a defined range.

The equilibrium price within this range would still depend on the performance standard set by the regulator. A weaker (higher) performance standard would introduce a larger number of compliance credits into the market and shift the blue vertical line to the right in Figure 4. This greater supply of credits puts downward pressure on prices. However, prices will not fall below the floor, since the government stands ready to purchase credits at that level.

Likewise, a more stringent standard would reduce the supply of compliance credits, shifting the vertical line in Figure 4 to the left. This reduced supply increases prices. However, prices would not rise above the headline level, since the government has a standing offer to sell credits at this price. Together, the headline price and the price floor create a price “collar” that bounds compliance credit prices within a defined range. The regulator controls the width of this collar by setting the headline carbon price and the price floor.

Under the proposed system, regulators in P&Ts would continue to set facility-specific performance standards just as they do today. Differences in performance standards across facilities and regions could continue to reflect facility- or sector-specific constraints, the international competitive environment, available decarbonization technologies, and provincial priorities.

However, unlike under the current system, the price of compliance credits would be bounded from below by the price floor. As a result, regulators could set more generous performance standards without undermining emissions reductions. This change would allow the federal government to shift its evaluation of stringency away from evaluating performance standards using the complex “demand test” and instead focus on whether a price floor is in place, which is more straightforward.3737 Under the proposed system, regulators would be able to set performance standards that account for the international competitive environment facing regulated facilities. One way to do so would be to set performance standards equal to the greenhouse gas intensity of international competitors in the same industry. This would ensure that the domestically regulated industry was not placed at a competitive disadvantage internationally. Other aspects of the benchmark, such as reporting requirements and the rule that revenues must not be returned in a way that offsets the carbon price, could remain unchanged.

Administrative Benefits of a Renewed Benchmark

Objectivity

From an administrative perspective, this proposal for a renewed benchmark is objective. It is straightforward to determine whether a regulatory system is compliant with the requirement for a price floor. Evaluation requires establishing whether a standing purchase offer is in place and the price paid for bought credits. Both aspects can be evaluated in a straightforward and evidence-based manner, making it simple to determine whether a proposed carbon pricing system complies with the benchmark.

Transparency

With a price floor in place, the benchmark becomes more transparent. It is no longer necessary to conduct a “demand test” to evaluate the stringency of performance standards. Most importantly, this approach eliminates the need for modelling and avoids the opaque and subjective exercise that is part of the current process of evaluating the benchmark. Evidence-based evaluation helps all parties. P&Ts proposing a regulatory system can clearly determine whether it complies with the benchmark. The federal government can assess compliance more easily, and because the rules are straightforward, enforcement is more likely to be viewed as reasonable. Regulated firms also gain greater certainty about the future evolution of regulatory stringency, allowing for better planning.

Economic Benefits of a Renewed Benchmark

Lower transaction costs

From an economic perspective, the proposed benchmark reduces transaction costs. Regulatory markets in Canada are small, as shown in Table 1. Facilities with excess permits to sell may not be able to identify trading partners that wish to purchase an equal number of permits at the same time. Moreover, the lack of information about trades means that facilities may have little understanding of current valuations for compliance permits and a limited sense of the opportunity to buy or sell credits.

These “transaction costs” inhibit trades and, as a result, get in the way of cost-effective distribution of emission mitigation investments. The proposed changes to the benchmark help lower these costs by providing increased information and more certainty about compliance credit prices. Under the proposed system, a facility with compliance credits to sell does not need to search for a buyer but can always sell additional permits at the price floor to the government. Facilities also no longer need to guess compliance credit prices, as they know the bounds of current and future prices. This helps facilities plan decarbonization investments and significantly reduces uncertainty in future regulatory exposure.

Greater price consistency across jurisdictions

The proposal also improves price consistency across jurisdictions. Current rules generally prevent trading of compliance credits across jurisdictions (although some credits are fungible between the federal and certain provincial systems). As a result, it is likely that some regulatory systems will be “tight” – with high compliance credit prices and few available compliance credits – while others are “loose” – with low compliance credit prices and few compliance credit buyers.

Although Table 2 does not report prices, it indicates that this situation existed in 2022. Excess permits were held in Ontario, Alberta, and Newfoundland and Labrador, while permits were scarce in Nova Scotia and the federal system. This divergence implies that emission allocation is not being cost-effectively pursued across the federation.

The proposed changes to the federal benchmark would reimpose comparable compliance credit prices across all jurisdictions. By introducing a price floor, credit prices would be bounded within a narrow range, ensuring that all regions face similar incentives to reduce emissions. This alignment is a defining feature of a cost-effective, price-based approach to emissions mitigation.

Reducing the tension between decarbonization and competitiveness

The proposal also enables leakage and competitiveness protection alongside deep decarbonization. The tradable performance standard approach to reducing emissions is chosen for the federal OBPS and across most P&Ts because it incentivizes facilities to reduce emissions while at the same time protecting them against losses in international competitiveness.3838 Environment and Climate Change Canada. 2026. “Output-Based Pricing System.” February 6. https://www.canada.ca/en/environment-climate-change/services/climate-change/pricing-pollution-how-it-will-work/output-based-pricing-system.html. See also: Böhringer, Christoph, Carolyn Fischer, and Nicholas Rivers. 2024. Rebating Revenues from Unilateral Emissions Pricing. CESifo Working Paper No. 11376. Under the current benchmark, however, these objectives are linked: the same mechanism – the performance standard – both drives emissions reductions and provides competitiveness protection (see Box 1).

As a result, tighter standards increase emissions reductions (if compliance credit prices are below the benchmark) while looser standards do the opposite. Achieving net-zero emissions under the current system would require setting performance standards to zero, eliminating all protection against leakage and losses in international competitiveness. This is clearly a serious problem for the current approach to decarbonization in the long run and would necessitate some other mechanism, like carbon border adjustments, to protect competitiveness in a deep decarbonization scenario (Commission on Carbon Competitiveness 2024).

The proposed amendment breaks this link. With a price floor in place, regulators can set more generous performance standards to protect competitiveness without weakening incentives to reduce emissions, since the price floor ensures that compliance credit prices remain above a minimum level regardless of how standards are set. This decoupling allows regulators under the proposed system to both pursue deep decarbonization and protect competitiveness, which is impossible under the present system without carbon border adjustments. Competitiveness can be protected by setting performance standards that reflect threats of international leakage, while considering fiscal implications (see below). For example, performance standards could be aligned with the emissions intensity of trading partners, while the price floor maintains incentives for emissions reductions. In this manner, the proposed benchmark enables both objectives to be achieved as decarbonization deepens, which is not possible under the current system.

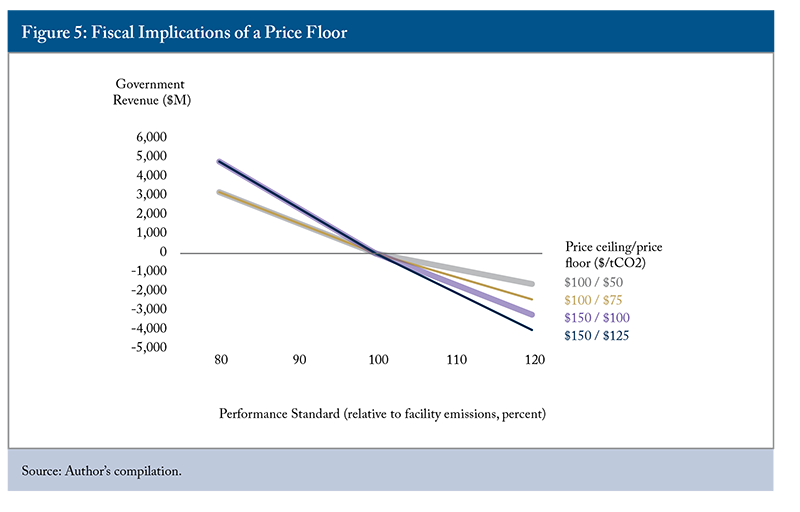

Fiscal Implications

Introducing a price floor creates potential new fiscal obligations for governments. These fiscal outcomes depend on two factors: first, the level of the price floor and headline price, which determine the prices at which governments purchase and sell compliance credits. And second, the level of the performance standard set by the regulator, which determines the amount of compliance credits issued to facilities and the amount of compliance credits that are required for regulatory compliance.

Holding the price floor and headline price constant, the choice of performance standard determines whether the system generates revenue or incurs costs for government:

- If regulators set performance standards, on average, equal to facility emission intensity, the system will be revenue-neutral;

- If regulators set performance standards below (i.e., more stringent than) facility emission intensity, then the system will be revenue-raising;

- If regulators set performance standards above (i.e., less stringent than) facility emission intensity, then the system will be cost-incurring (to government).

As a quantitative example, consider the Alberta TIER system – by far the largest price-based system in Canada (see Table 2). Figure 5 shows the potential revenue implications of the proposed system design. Two potential headline (ceiling) prices are illustrated: $100/t CO2e and $150/t CO2e. Two price floor scenarios are illustrated: $25/t CO2e and $50/t CO2e below the headline price.

The horizontal axis shows the average performance standard relative to average facility emission intensity, where 100 percent corresponds to standards equal to average performance. Performance standards below (i.e., more stringent than) 100 percent raise revenue in proportion to the headline price and the performance standard. Performance standards above (i.e., less stringent than) 100 percent cost revenue and act as an industrial subsidy.

Under the assumptions shown, the system can be revenue-neutral, generate up to $5 billion per year, or provide subsidies of up to $3 billion per year towards industry. While these choices have clear fiscal implications and important implications for industrial competitiveness, they do not affect decarbonization directly, which depends on marginal emission prices. Ultimately, the fiscal impact of the proposed system depends on how regulators set performance standards relative to existing emission intensity.

One benefit of the proposed system is that it connects regulators’ choices of performance standards to fiscal implications for that government. Under the proposed system, a regulator could choose to set less stringent performance standards. This choice could be appropriate and reflect concern about leakage or international competitiveness. But setting less stringent performance standards would also have negative fiscal implications for that government.

Likewise, a regulator could choose to set more stringent performance standards if it does not face significant competitiveness concerns, knowing that this choice would raise revenue. In contrast, under the current benchmark, regulators face no fiscal or other consequences for setting weak performance standards. As a result, many systems have adopted such standards, leading to over-allocation of compliance credits, low credit prices, and weaker incentives for decarbonization.

In addition to these fiscal considerations, existing stocks of banked compliance credits present an important issue. For example, Alberta’s TIER system currently holds approximately 47 million banked credits – credits generated in prior compliance periods and withheld for future use. These large inventories reflect historically generous performance standards combined with expectations of rising credit prices.3939 Smith, Laurie. 2026. “Canada’s Carbon Future: Unpacking the Alberta MOU, TIER, and Federal Benchmark Review.” January 15. https://www.clearbluemarkets.com/knowledge-base/canadas-carbon-future-unpacking-the-alberta-mou-tier-and-federal-benchmark-review This large supply of banked credits is likely to limit emission reductions in the near term and could pose challenges for the proposed price floor, as it creates a potentially significant fiscal liability. One way to potentially address this issue would be to apply price floors differently by permit vintage and to phase the price floor proposal in slowly.

Offsets

In some P&T carbon pricing systems and in the federal OBPS system, offsets are used in conjunction with the industrial carbon price. The presence of offsets does not markedly change the proposed system. Offsets introduce a new source of compliance credit supply, as shown in Figure 6. This additional supply contributes to the overall pool of compliance credits and thus affects the equilibrium in the compliance credit market.

However, with a price floor in place, compliance credit prices will remain at or above the floor, no matter how many offset credits are created. This creates a potential fiscal obligation, which should help discipline regulators to limit offset protocols to only the highest-quality offsets. This disciplining mechanism would help to limit the availability of low-quality offset credits, which have significantly undermined decarbonization in many prior carbon pricing markets (Calel et al. 2025).

Quebec

The price floor approach advocated in this report could work in all jurisdictions but would need special consideration in Quebec due to its linkage with other members of the Western Climate Initiative. These jurisdictions already set a price floor for credit prices at auction, which started at US$10/t CO2e in 2010 and has risen annually by 5 percent plus the rate of inflation. It is now about CA$35/t CO2e – significantly lower than the current “headline carbon price” of $95/t CO2e in the federal benchmark.4040 Ministere de l’Environnement, de la Lutte contre les changements climatiques, de la Faune et des Parcs. 2026. “The Carbon Market: Auctions.” https://www.environnement.gouv.qc.ca/changements/carbone/Ventes-encheres-en.htm Credit market prices have traded at levels close to the price floor since the establishment of the market more than a decade ago. Since the credit market is cross-jurisdictional, it is not straightforward to require a higher price floor in Quebec. This issue has been contentious, with provinces pointing to divergent carbon prices across Canada as both unfair and economically inefficient.

Several approaches could be considered to implement the proposed price floor given the Quebec-California linkage:

1 Adopt the Quebec-California price floor level across all jurisdictions in Canada. This would improve harmonization but would significantly lower carbon prices in most provinces and weaken the overall stringency of climate policy.

2 Maintain differentiated price floors between quantity-based and price-based systems. This would leave potential for higher price floors and more carbon mitigation in other regions, but would preserve existing regional differences in carbon prices.

3 Impose an equivalent price floor across all regions at a level higher than the Quebec-California price floor. This would likely require Quebec to end its linkage with California and align its pricing trajectory with other Canadian provinces.

None of these is a perfect option. But it’s worth noting that even in the absence of the price floor proposal, differences in compliance credit prices between Quebec and other provinces have been controversial and likely require attention.

Conclusion

Canada’s industrial carbon pricing regime aims to reduce emissions while protecting competitiveness. To reflect the country’s federal structure, it requires provinces and territories to impose a consistent carbon price across jurisdictions while preserving provincial and territorial autonomy to design systems that meet local needs.

However, rather than setting prices directly, the federal government relies on a “demand test” to determine whether provincial and territorial performance standards will result in an equilibrium price that follows the federal government’s preferred price trajectory. This report argues that there’s a better way: the federal government should require all provinces and territories (as well as the federal OBPS system) to impose a common price floor for compliance credits.

A price floor provides a more direct way to ensure consistent carbon pricing across jurisdictions. It improves objectivity, enhances fairness, and better harmonizes prices across provinces. While the approach has fiscal implications, system regulators have the freedom to choose whether their carbon pricing systems generate revenue, incur costs, or remain revenue-neutral. They also continue to set performance standards in a way that balances fiscal implications with the need to protect international competitiveness.

While this report focuses on carbon pricing, this policy alone is unlikely to achieve the dual goals of deep emissions reductions and competitiveness. Complementary investments in technology, infrastructure, and capital, as well as other policies, are likely necessary.

The author extends gratitude to Stephanie Bailey, Mawakina Bafale, Colin Busby, Emma Dizon, Kent Fellows, Kate Koplovich, Andrew Leach, Daniel Schwanen, and several anonymous referees for valuable comments and suggestions. The author retains responsibility for any errors and the views expressed.

REFERENCES

Antimiani, Alessandro, Valeria Costantini, and Elena Paglialunga. 2015. “The Sensitivity of Climate-Economy CGE Models to Energy-Related Elasticity Parameters: Implications for Climate Policy Design.” Economic Modelling 51: 38–52.

Böhringer, Christoph, Carolyn Fischer, and Nicholas Rivers. 2023. “Intensity-Based Rebating of Emission Pricing Revenues.” Journal of the Association of Environmental and Resource Economists 10(4): 1059–1089.

Calel, Raphael, et al. 2025. “Do Carbon Offsets Offset Carbon?” American Economic Journal: Applied Economics 17(1): 1–40.

Canadian Climate Institute. 2025. 2024 Independent Assessment of Carbon Pricing Systems. March. https://climateinstitute.ca/wp-content/uploads/2025/02/2024-Independent-expert-assessment-carbon-pricing.pdf#page=32.

Commission on Carbon Competitiveness. 2024. Policies to Achieve Industrial Decarbonization in Sectors Facing Competitiveness Risks. October. https://carboncompetitiveness.ca/wp-content/uploads/2024/10/C3_Industrial_Decarbonization.pdf.

Cui, Wei. 2025. “Policy Forum: Comparing Canadian Output-Based Pricing Systems.” Canadian Tax Journal 73(1).

Government of Canada. 2025. Canada’s 2035 Nationally Determined Contribution. February. https://unfccc.int/sites/default/files/2025-02/Canada%27s%202035%20Nationally%20Determined%20Contribution_ENc.pdf.

Hahn, Robert, and Robert Stavins. 2011. “The Effect of Allowance Allocations on Cap-and-Trade System Performance.” Journal of Law and Economics 54(S4): S267–S294.

Ontario Ministry of the Environment, Conservation and Parks. 2024. GHG Emissions Performance Standards and Methodology for the Determination of the Total Annual Emissions Limit. March. https://prod-environmental-registry.s3.amazonaws.com/2024-04/GHG%20EPS%20and%20Methodology%20for%20determination%20of%20TAEL_March%202024%20%28EN%29_1.pdf.