by Don Drummond, William B.P. Robson and Alexandre Laurin

- Canada can no longer pride itself on its fiscal discipline. With the economy operating near capacity and growth in productive capacity weak, governments continue to run deficits and project rising debt ratios, undermining growth and living standards rather than supporting them.

Government projections understate the risks. Weak productivity, low business investment, and demographic pressures will hold back growth and revenues, while ageing, healthcare, and defence will push spending higher. Even modest changes in growth or interest rates could materially worsen the fiscal picture.

Government projections understate the risks. Weak productivity, low business investment, and demographic pressures will hold back growth and revenues, while ageing, healthcare, and defence will push spending higher. Even modest changes in growth or interest rates could materially worsen the fiscal picture.- Restoring discipline will take a real change in direction. Governments must rein in spending, set a credible path to balance, and pursue reforms that boost investment and productivity, including shifting the tax mix away from income towards less distortionary taxes. The federal government must lead the way in its upcoming Spring Economic Update.

Government projections understate the risks. Weak productivity, low business investment, and demographic pressures will hold back growth and revenues, while ageing, healthcare, and defence will push spending higher. Even modest changes in growth or interest rates could materially worsen the fiscal picture.

Government projections understate the risks. Weak productivity, low business investment, and demographic pressures will hold back growth and revenues, while ageing, healthcare, and defence will push spending higher. Even modest changes in growth or interest rates could materially worsen the fiscal picture.Introduction: Fiscal Fantasy and Fiscal Reality

Many Canadians may still have an image of Canada as a country aware that governments cannot spend and borrow without limit. They should not. The Globe and Mail columnist Gary Mason recently wrote about the “death of fiscal sanity in Canada” (Mason 2026). He pointed to the almost-doubling of the federal government’s net debt over the past decade, with the November 2025 budget projecting yet more, and budgets in British Columbia and Alberta that forecast relentless borrowing. He said we all know a crisis will hit but appear unwilling to act to prevent it.

Since Mason’s article, New Brunswick released a budget that shows a steep rise in its debt burden over the next four years. Quebec released a budget that showed a return to balance by 2029/30 – but that result, required by provincial law, depends on an unrealistically buoyant economy and major unidentified savings. Ontario released a budget that, notwithstanding its own inexplicably robust economic projections, features a higher debt ratio by the end of the decade. Prince Edward Island released a budget that prefigures a jump in its debt ratio. The federal government has also announced a fuel tax suspension – a multi-billion-dollar boondoggle that will add to its already excessive debt. All jurisdictions project deficits for 2025/26, with seven of them projecting deficits of at least 1.5 percent of GDP (Table 1).

At the same time, war in Iran and the broader Middle East is hurting prospects for world growth and raising inflation fears and debt risk premiums everywhere.

Many Canadians now seem to discount the fiscal constraints our federal and provincial governments had to confront in the 1990s. But, as science fiction novelist Philip K. Dick famously remarked, “Reality is that which, when you stop believing in it, doesn’t go away.”

Fiscal excess has already undermined economic growth and living standards. Without bold action to reduce the burden of public debt, government-fuelled consumption will continue to cut into the saving and investment needed to raise our incomes and purchasing power – and increase the risk of a borrowing crisis to boot. The federal government’s upcoming fiscal update needs to outline a change of direction – a profound and credible one.

Some Fiscal History

Canada has alternated between periods of fiscal discipline and fantasy. The immediate post-World War II period was disciplined. As military spending fell – from wartime peaks of four-fifths of all federal spending – the government ran substantial surpluses during the 1950s, and the war-swollen debt-to-GDP ratio plummeted.

The mood shifted in the late 1960s, ushering in a quarter-century of fiscal fantasy. The federal government’s budget deficits averaged 5.5 percent of GDP from 1975/76 to 1995/96, large enough to raise its net debt11 The net debt measure used in this E-Brief (unless otherwise specified) is defined as total liabilities minus financial assets. Net worth (net debt minus the value of amortized tangible capital, or accumulated deficits) is used less frequently in provincial budget projections than in federal budgets, and historical provincial data are generally reported on a net debt basis. Net debt is a key metric of indebtedness used by credit rating agencies. from less than one-fifth to two-thirds of GDP. Provinces and territories also increased borrowing, pushing their aggregate net debt to nearly one-third of GDP by the late 1990s. Combined federal and provincial net debt approached the size of the entire economy.

From 1961 to 1973, output per hour worked in the business sector roared ahead at an annual average pace of 3.5 percent. The rate then dropped: average growth was 1.8 percent from 1973 to 1981, 1.5 percent from 1981 to 1989, and 1.8 percent from 1989 to 2000.

In the 1970s and 1980s, fiscal policymakers did not – and arguably refused to – recognize the reality of slower productivity growth. Many attributed the economy’s disappointing performance to inadequate aggregate demand and argued that stimulative government spending financed by deficits was not a problem, since renewed growth would shrink the debt relative to the economy. Budgets in the 1980s typically projected growth in the economy and revenue that was too high and future debt burdens that were too low.

By the mid-1990s, however, reality bit. The relentless pressure of interest payments on annual budgets and evidence of dwindling appetite for Canadian sovereign debt from potential lenders forced a re-evaluation of the reality of fiscal policy. Provinces cut spending and borrowing, and so did the federal government. Budgets began to project surpluses, and the surpluses were achieved. Debt ratios and interest burdens fell, setting the stage for tax reforms into the 2000s.

The Current Need to Recognize Reality

Continuing Slow Growth of Productive Capacity

Today’s rhetoric echoes claims by finance ministers and other political leaders from the 1970s and 1980s that slow growth is cyclical rather than structural, and that a weak economy justifies spending and borrowing at levels that, if maintained, would be unsustainable. Meanwhile, rapid spending growth has become the norm. From 2018/19 to 2024/25, federal program spending rose 7.3 percent on an annual average basis.22 Excluding carbon tax proceeds and redistribution. Program spending by all provincial and territorial governments rose at an average annual rate of 6.6 percent, with British Columbia at 8.7 percent – well ahead of population growth and inflation and far exceeding earlier budget projections.

Yet growth, undermined by low business investment and stagnating productivity, remains feeble. The Bank of Canada’s latest estimate of the “output gap” (the shortfall of aggregate demand against aggregate supply) is just 0.8 percent of GDP, and the unemployment rate is close to its longer-run historical average. Prospects for a resurgence in GDP and government revenue are poor. If the economy is operating close to capacity, budgets should be close to balance, and debt-to-GDP ratios should be falling.

The Burden of High Debt

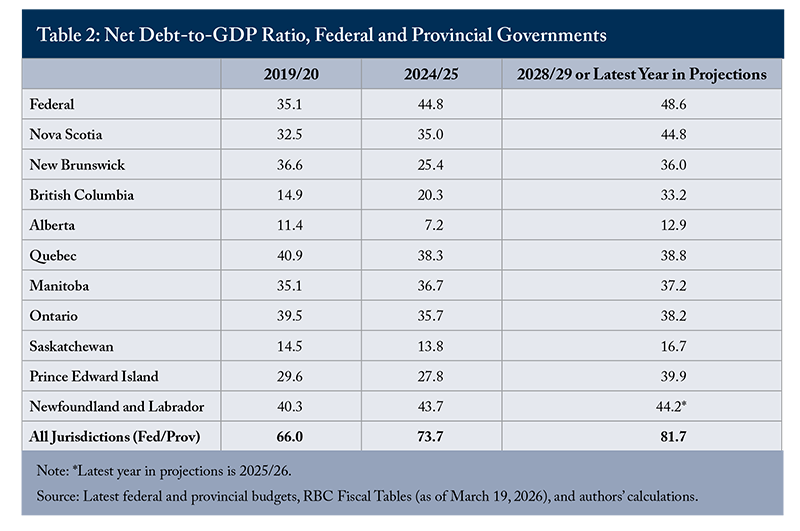

But debt ratios are not falling. They are rising (Table 2). By 2028/29, the combined federal and provincial net-debt ratio will approach 82 percent – far higher than before the COVID-19 pandemic.

The 2025 federal budget projected that the ratio of federal debt33 The federal accumulated deficits: net debt less non-financial assets. to GDP would still exceed 37.2 percent in 30 years. This projection exemplifies current lack of concern about large debts and fantasy about addressing them. Even slight changes to the growth or interest rate assumptions over that timeframe would produce a rise.44 For instance, a one-percentage-point increase in the interest rate on government debt would push the debt ratio to 48.5 percent by 2056. Similarly, a 0.25 percentage point reduction in productivity growth or in immigration would lead to debt ratios of 44.2 percent and 45.2 percent, respectively (Canada 2025, p. 263). A recent sustainability analysis of combined federal, provincial, and territorial net debt shows a rising long-term baseline, with a 50 percent probability of a sharp increase once economic shocks and interest rate risks are taken into account (Lester and Laurin 2025). With war and interest rates rising because of inflation fears and higher borrowing to finance military expenditures, these shocks and risks are now closer to reality.

Fiscal Profligacy Elsewhere is Cold Comfort

The federal government has often argued that Canada can keep borrowing because its debt burden is lower than that of many other countries. This argument has many flaws.

International comparisons of gross debt are not nearly as favourable to Canada as they appear. Assets in the Canada and Quebec Pension Plans (CPP/QPP), which largely explain the gap between gross and net debt, are not available for any other purpose than to pay future CPP/QPP liabilities – liabilities that are not measured in the international comparisons. They are not assets of the Canadian or Quebec governments.

Being in better shape than fiscal basket cases around the world is very cold comfort. Even before the outbreak of war and the resulting rise in fuel prices and downgraded projections of growth and fiscal balances, concerns over debt burdens in Japan, the United States, and many European countries were already putting upward pressure on bond yields.

Fiscal balances can deteriorate fast, as Canada’s own history shows. Borrowers and credit rating agencies are as alert to economic and political risks as they have ever been.

Perhaps most conclusively, it is unconscionable to burden future generations for current consumption that they – living with an economy suffering from decades of deficient saving and private investment – will not enjoy.

We Need More Realism in Budgeting

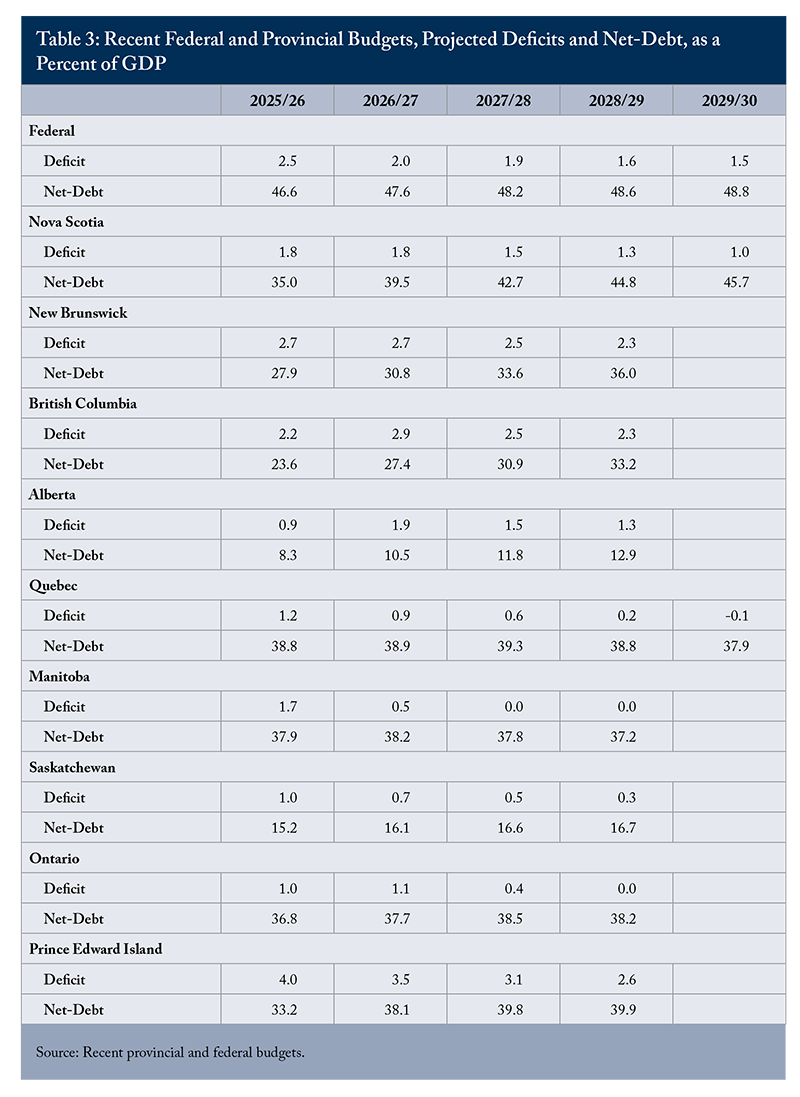

Projections in 2026 budgets released so far show chronic deficits and rising debt for years (Table 3). Nova Scotia, New Brunswick, British Columbia, Alberta, and Prince Edward Island had small deficits or even surpluses into the 2020s, but now all project sharply higher debt burdens. Quebec’s projected decline rests on shaky numbers, and Ontario projects a higher one. If the definition of insanity is doing the same thing over again while expecting a different result, Gary Mason’s comment about the death of fiscal sanity is spot on. We are repeating the excesses of the 1980s and early 1990s, and we are suffering the consequences.

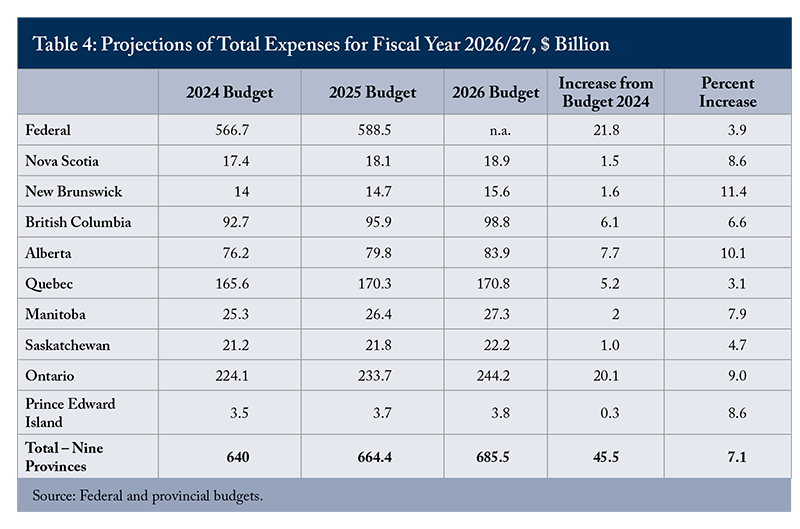

Table 4 compares projected total expenses for 2026/27 in 2026 budgets (and the federal government’s budget last fall) to projected expenses for that year in previous budgets. All show overshoots from previous projections. Quebec’s 3.1 percent overshoot is the smallest, while Alberta and New Brunswick’s overshoots exceed 10 percent. Across the nine provinces, projected 2026/27 expenses are $45.5 billion, or 7.1 percent, higher than they were in 2024. These overshoots reflect policy decisions: higher program spending and deficits that drive up interest payments.

What are the chances of lucky breaks – faster economic growth or other circumstances that would improve fiscal outcomes relative to projections?

Governments talk about their spending as “investment” that will boost growth. But the issue is whether the government or the private sector is better placed to make investments that will yield an economic return. When the economy is at capacity, higher government spending and borrowing reduce the resources available for private sector investment (Robson and Bafale 2025).

Demography will not help in the short run. Canada’s population declined in 2025, largely because of a sharp reduction in immigration. Lower immigration in the future, combined with a continuation of Canada’s slow pace of productivity growth, will hold back growth of GDP and government revenues. Population ageing will further lower revenue growth as a lower portion of the population will be of working age and paying full taxes.

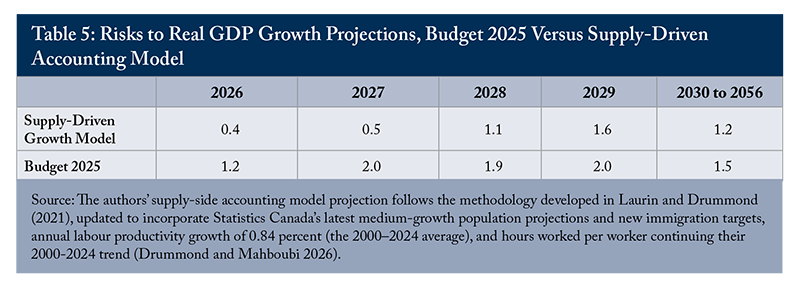

Table 5 compares real GDP growth projections in the 2025 federal budget with supply-driven estimates based on new immigration targets and post-2000 trends of labour productivity and hours worked.

From 2030 to 2056, the 2025 Budget projects average annual growth of real GDP of 1.5 percent. Our supply-driven estimate is only 1.2 percent. By 2056, output is more than 10 percent lower under our scenario than in the Budget.

Looking back, budgets missed the productivity slowdown of the 1970s. They may now be missing a break to still lower growth. Output at the lower levels shown in Table 5 would raise the net debt-to-GDP ratio substantially and understate the amount of fiscal restraint required to restore fiscal stability.

Neither will demography help in the long run. The C.D. Howe Institute has analyzed in detail how population ageing will pressure public finances in Canada (Robson and Mahboubi 2024).

In addition to the downward pressure on the tax base mentioned above, it will push spending up. Federal spending on Old Age Security and the Guaranteed Income Supplement is presently 2.6 percent of GDP. By 2030, it will be around 3 percent (Canada 2023). Ageing is also adding about 1 percentage point annually to healthcare spending growth and will continue to strain the largest area of provincial spending.55 The New Brunswick 2026 Budget clearly illustrates the pressures on healthcare, driven not only by ageing but also by challenges such as access to primary care. It increases healthcare spending by $710 million over 2025/26, for an annual growth rate of 17.4 percent. Over the next 50 years, provincial health spending could rise by 5 percentage points of GDP (Robson and Mahboubi 2024).

Last but certainly not least, satisfying Canada’s recent pledge to raise core defence spending to 3.5 percent of GDP will require increasing defence spending from around $35.4 billion in 2024/25 to $84.7 billion by 2029/30, and to $147.4 billion by 2034/35 (Busby and Dahir 2026).

Sensible Fiscal Policy

Stop Burdening Canadian Youth

Canada’s youth will struggle to cope with the high federal and provincial debt burdens being passed forward to them. They may face additional pressures from environmental stresses, geopolitical conflict, and technologically enabled crime and terrorism.

If productivity growth continues at its post-2000 pace, economic and wage growth will remain modest. Meanwhile, tax burdens are already quite high by historical standards.

Boost Economic Growth

Canada needs stronger productivity growth. A prime culprit in weak Canadian labour productivity is low business investment. Investment in machinery and equipment per worker is almost three times higher in the United States than in Canada (Robson and Bafale 2025). If firms did not invest when access to the US market was relatively open, something very enticing must be offered to encourage them to invest now that that access is in question. Fiscal policy needs to address this challenge.

Canada relies much more heavily on corporate and personal income taxes than most countries. Those taxes do much more economic harm than broad-based consumption taxes. Mintz et al. (2026) proposed a revenue-neutral “big bang” overhaul and simplification of Canada’s tax system that could raise Canada’s GDP by 2.5 percent over the long run.

The Federal Government Must Change Direction

The federal government’s upcoming Spring Economic Update must prefigure a change in direction: much lower spending in non-priority areas that ballooned over the past decade to make room for higher defence spending, while reducing borrowing and preparing the groundwork for lower income taxes. Specifically, it should:

- Present a realistic baseline for economic and fiscal prospects, most likely showing weaker growth and higher deficits and debt than in the 2025 Budget.

- Focus relentlessly on future challenges rather than self-congratulations over past actions.

- Set a clear track toward budget balance over a politically relevant period – say, four years – with credible measures to achieve it.

- Establish spending restraint targets based on mid-to-late 2010s levels, before spending growth exploded, rather than against future projections from today’s over-elevated base, supported by rigorous value-for-money reviews and independent oversight (Lester 2025).

- Prepare for major tax reform that would incentivize investment, such as those in a recent C.D. Howe Institute paper outlining lower corporate income tax rates and base broadening, and deferral of taxation until profits are distributed (Mintz et al. 2026), while shifting the tax mix from income to consumption.

Time for Bold Action

The federal government must acknowledge that Canada’s twin economic crises – stagnant investment and productivity, and US trade aggression – require bold action, including measures that will meet some political resistance. It needs to build public support for lower spending, balancing budgets, and tax reform.

All Canadian governments need to more clearly communicate the country’s economic and fiscal challenges and engage taxpayers in a productive debate on course corrections. Canadians need to emerge from their fiscal fantasy and face reality.

The authors extend gratitude to Nicholas Dahir, Brian Ernewein, Yves Giroux, Jeremy Kronick, John Lester, Peter MacKenzie, and several anonymous referees for valuable comments and suggestions. The authors retain responsibility for any errors and the views expressed.

References

Busby, Colin, and Nicholas Dahir. 2026. A Steep Climb: Financing Canada’s NATO Commitment while Maintaining Fiscal Discipline. Commentary 711. Toronto: C.D. Howe Institute.

Canada. 2023. Actuarial Report (18th) on the Old Age Security Program as at 31 December 2021. Ottawa: Office of the Superintendent of Financial Institutions, Office of the Chief Actuary.

Canada. 2025. Budget 2025. Department of Finance Canada. November.

Drummond, Don, and Parisa Mahboubi. 2026. “Canada’s Economy Is Growing Far Slower Than Ottawa Thinks.” Intelligence Memo. Toronto: C.D. Howe Institute. April 22.

Laurin, Alexandre, and Don Drummond. 2021. “Rolling the Dice on Canada’s Fiscal Future.” E-Brief 319. Toronto: C.D. Howe Institute.

Lester, John. 2025. “Federal Expenditure Review: Welcome, But Flawed.” E-Brief 377. Toronto: C.D. Howe Institute.

Lester, John, and Alexandre Laurin. 2023. “Ottawa Needs a New Approach to Fiscal Policy.” E-Brief 338. Toronto: C.D. Howe Institute.

_____________. 2025. Canada’s Debt Problem: What Can Be Done? A Report on the Institute’s 2024 Debt Conference. Commentary 675. Toronto: C.D. Howe Institute.

Mason, Gary. 2026. “The Death of Fiscal Sanity in Canada.” The Globe and Mail. March 3.

Mintz, Jack, Alexandre Laurin, and Nicholas Dahir. 2026. “Big Bang” Tax Reform: Unleashing Growth in the Canadian Economy. Commentary 707. Toronto: C.D. Howe Institute.

Robson, William B.P., and Mawakina Bafale. 2025. Canada’s Investment Crisis: Shrinking Capital Undermines Competitiveness and Wages. Commentary 699. Toronto: C.D. Howe Institute.

Robson, William B.P., and Parisa Mahboubi. 2024. Another Day Older and Deeper in Debt: The Fiscal Implications of Demographic Change for Ottawa and the Provinces. Commentary 665. Toronto: C.D. Howe Institute.

Sharpe, Andrew, and John Tsang. 2018. “The Stylized Facts about Slower Productivity Growth in Canada.” International Productivity Monitor 35 (Fall): 52–72. Centre for the Study of Living Standards.